Top Conviction Ideas - Auto & Auto Ancillaries by Axis Securities

Q1FY26 Auto OEM Review – Growth in 2W/Tractor OEMs

* Financial Performance

? Revenue/EBITDA in Q1FY26 grew by 7%/1% YoY, respectively, against our expectations of ~4%/-3% YoY for Auto OEMs under our coverage. The revenue growth was largely driven by 9%/10% volume growth in the tractor/3W industry (though Escorts was up only 2%), while PV/MHCV/LCV were flat, and 2Ws down 2% YoY. Revenue/EBITDA declined by 5%/9% QoQ against our estimates of 8%/13% QoQ, respectively. The YoY EBITDA margin decline was due to increased operational expenses and higher personnel costs due to annual wage revision, higher marketing and advertisement spends, partly offset by a richer product mix (higher exports) and price hikes taken over the past year. PAT grew by 10% YoY (our estimate of -3%), aided by other income, mainly MTM forex gains in certain OEMs, while declining 4% QoQ (our estimate: -16%).

? Maruti, Eicher Motors, and Bajaj Auto faced downward pressure on margins by 239 bps, 277 bps, and 52 bps, respectively. However, margins were largely positive for Ashok Leyland and TVS Motor, up 52 bps and 106 bps, respectively

Q1FY26 Auto Ancillaries Review – Mixed Performance

* Financial Performance

? The companies under our coverage reported 13%/14% growth in Revenue/EBITDA in Q1FY26, respectively, slightly better than our expectations of ~11% each YoY. This was driven by sales volume growth (3Ws and tractors) and the premiumization trend. Revenue/EBITDA grew by 2.5%/1.2% QoQ, largely in line with our estimates of 1.3%/1.3% QoQ, respectively. EBITDA growth was supported by cost-control initiatives and operating leverage, partially offset by a marginal impact from commodities for some auto ancillaries. PAT was up by 7% YoY (our estimate: 9%), but declined 7% QoQ (our estimate: 6%).

? Endurance Technologies, UNO Minda, SSWL, and Minda Corp delivered strong YoY EBITDA growth, while Sansera Engineering and Automotive Axles remained largely flat (+/-) 2%YoY. CIE Automotive saw a 6% YoY decline due to an unfavourable product mix in the Indian business and one-time restructuring expenses at Metalcastello, Europe.

Sector Outlook (Q1FY26 Vs Q1FY25)

Outlook – Industry Approaching Long-Term CAGR volumes

? We expect EBITDA margins to remain largely stable in the near term, supported by a richer product mix, while raw material headwinds could exert slight pressure.

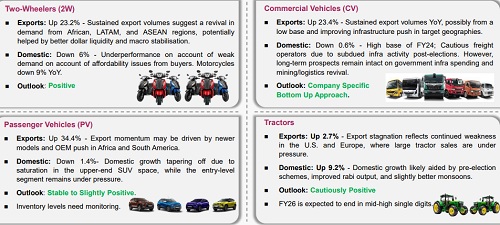

? We expect 2W sales volumes to sustain mid to high single-digit growth in FY26E, supported by new premium segment launches, an extended replacement cycle, and recovery in exports. A favourable monsoon, income tax relief, and increased rural spending are likely to further drive demand for entry-level motorcycles. The expected GST rate cut by Sep-Oct’25 to 18% (from 28% currently) in 150cc/350cc (unclear as per media reports) and lower engines will be a booster/immunity shot in the post covid era, which may result in the revival of the domestic entry-level 2W industry.

? Overall PV sales growth, which has been largely led by the UV segment, is expected to remain in the mid single digits in FY26E (earlier low single digit expectations) due to expectations on the GST rate cut, which may arrest declining entry-level PV domestic sales.

? For FY26, OEMs remain optimistic about long-term structural growth drivers, including India’s vast road network, policy measures aimed at reducing supply chain costs, the Vehicle Scrappage policy, reduced interest rate costs and continued infrastructure Capex outlined in the Union Budget.

? Tractor/CV volumes are expected to grow in the mid-high single digits in FY26, supported by a favourable monsoon, lower financing costs, GST rate cut expectations and increased government allocations towards the farming/infrastructure sector before the state election.

? We remain selective in our approach. Among OEMs under our coverage, our Top Conviction Ideas in 2Ws are Hero Motocorp, Bajaj Auto; in CVs is Ashok Leyland, and in the PV/tractor segment, we favour Mahindra & Mahindra (non-coverage), given its strong SUV product portfolio and leadership position in the domestic tractor industry. We recommend the “Buy On Dips” Strategy for TVS Motors and Maruti Suzuki Ltd. Auto Ancillaries

? In the long run, product premiumization, strong order books, growing exports, GSt rate cut and the shift toward EVs are expected to drive higher content per vehicle, boosting profitability. Considering current valuations, our top conviction picks in the ancillary space are Sansera Engineering Ltd. We also suggest a "Buy on Dips" approach for Endurance Technologies and UNO Minda for long-term gains.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...