South Africa Economy Update 23rd June 2026 by CareEdge Ratings

GDP growth exceeds expectations in Q1 2026

The South African economy expanded by 0.5% QoQ in Q1 2026, up from 0.4% in Q4 2025. The growth exceeded expectations and was broad-based, with the majority of sectors registering positive momentum.

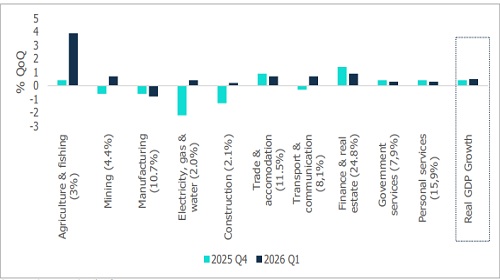

GVA growth rates (seasonally adjusted)

As depicted in the chart, the agriculture, forestry and fishing sector grew by 3.9% QoQ in Q1 2026, vs 0.4% in Q4 2025, driven by higher production of field crops and horticultural products. Meanwhile, the finance, real estate and business services sector moderated to 0.9% from 1.4% in the previous quarter, though it maintained upward momentum through financial intermediation and auxiliary financial services. The trade, catering, and accommodation sector grew by 0.7%, slightly lower than the 0.9% recorded in Q4 2025, reflecting strong wholesale trade, motor trade, food and beverage sales, and accommodation activities. Similarly, the transport, storage and communication sector grew by 0.7%, rebounding from a 0.3% contraction recorded in the previous quarter due to improved land, air and transport support services.

Mining activity improved from -0.6% in Q4 2025 to 0.7% in Q1 2026, supported by higher production levels of platinum group metals (PGMs), gold, chromium ore, and diamonds. In contrast, manufacturing contracted by 0.8%, marking a second consecutive quarterly decline, because of lower output in the petroleum and chemical products, iron and steel, and wood and paper-related manufacturing divisions.

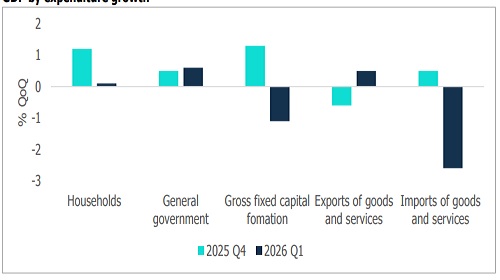

On the expenditure side, economic activity was supported by government spending and an improvement in net exports during the first quarter. Government consumption expenditure increased by 0.6% QoQ vs 0.5% in Q4 2025, while exports of goods and services returned to positive territory, increasing by 0.5% after a 0.6% contraction in the previous quarter. Simultaneously, imports declined by 2.6%, resulting in a positive contribution from the external sector. In contrast, household consumption growth slowed significantly to 0.1% from 1.2% in Q4 2025, suggesting weaker consumer spending. Gross fixed capital formation also contracted by 1.1%, indicating a decline in investment activity during the quarter. The expenditure data points to a moderation in domestic demand, with growth increasingly supported by government expenditure and net trade.

GDP by expenditure growth

Overall, South Africa entered 2026 on a stronger-than-expected footing, while recent diplomatic progress in the Middle East has reduced some of the downside risks associated with higher oil prices. Nevertheless, uncertainty remains elevated and risks to inflation, growth and financial markets have not been fully eliminated.

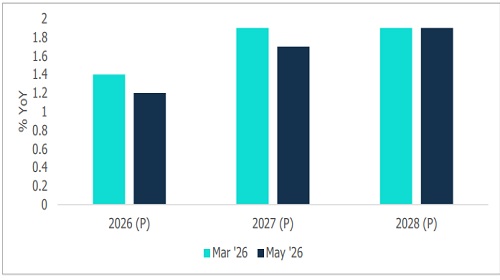

SARB cuts growth projections for 2026

While the stronger-than-expected Q1 outcome suggests that the economy entered 2026 on a firmer footing, the medium-term outlook remains constrained. At its May 2026 Monetary Policy Committee (MPC) meeting, the South African Reserve Bank (SARB) lowered its growth projections to 1.2% for 2026 and 1.7% in 2027 (from March’s projections of 1.4% and 1.9%, respectively), while holding 2028 steady at 1.9%. The downward revisions reflect a combination of heightened global uncertainty and reduced disposable incomes following escalated tensions in the Middle East. Higher oil prices, elevated inflationary pressures, and weaker global growth are expected to weigh on household consumption and investment activity, which previously drove South Africa’s recovery

The MPC also highlighted the impact of recent floods in the Western Cape, Eastern Cape and North-West provinces, which caused significant damage. In addition, the bank identified the possible emergence of El Nino conditions as a further downside risk to growth, given its potential impact on agricultural production and food prices. These risks, combined with persistent geopolitical uncertainty, have increased the likelihood of slower economic activity over the forecast period.

SARB’s growth projections

SARB revises inflation forecasts and raises the repo rate

Consumer inflation rose to 4% in April from 3.1% in March, driven by an 11.4% rise in fuel prices--one of the largest jumps in fuel inflation on record. Services inflation accelerated to 4.6%, reflecting broader price pressures in transport, insurance, and financial services.

At its May 2026 meeting, the MPC noted that the escalation of tensions in the Middle East has significantly altered the inflation outlook through higher oil prices, increased transport costs, and exchange rate pressures. As a result, the SARB revised its inflation and growth forecasts. Therefore, the MPC raised the repo rate by 25 basis points to 7.00%, effective May 29, 2026. The decision was split: four members voted in favour of the rate hike, while two preferred keeping the rates unchanged. The rate hike action reflects growing concerns over inflation risks and elevated global uncertainty.

SARB’s inflation projections

In its baseline forecast, the SARB expects headline inflation to average 4.4% in 2026, representing a 0.7 percentage point upward revision from the 3.7% projected in the March 2026 MPC meeting, before moderating to 3.7% in 2027 and reaching the SARB's preferred target of 3.0% in 2028. The upward revision is driven by risks of high global oil prices, elevated fuel inflation, and looming second-round effects. The SARB also flagged renewed pressure on food prices, with the agricultural sector facing higher diesel and fertiliser costs.

The MPC's alternative scenarios suggest that prolonged oil price spikes paired with a weaker Rand could result in significantly higher inflation and slower-than-expected economic growth. Under a hypothetical prolonged Strait closure scenario, inflation could rise above 5% and remain sticky, requiring a more restrictive monetary policy stance. In a second, worst-case scenario that includes El Nino drought risks, inflation could peak above 6% and demand three additional policy rate hikes. Consequently, the SARB indicated that future policy decisions will be highly dependent on developments in global energy markets, inflation expectations, and the broader geopolitical environment.

Looking ahead, risks to growth and inflation will be skewed by developments in global energy markets and geopolitical conditions. While stronger-than-expected GDP growth in Q1 2026 suggests that the economy entered the year on a firmer footing than anticipated, elevated oil prices, rising production costs and weaker household purchasing power are expected to weigh on economic activity in the coming quarters. Resultantly, the SARB is likely to maintain a cautious and data-dependent approach to monetary policy, with inflation developments remaining the key determinant of future interest rate decisions.