2025-09-16 02:31:14 pm | Source: Choice Broking Ltd

Reduce Uno Minda Ltd for the Target Rs.1,215 by Choice Broking Ltd

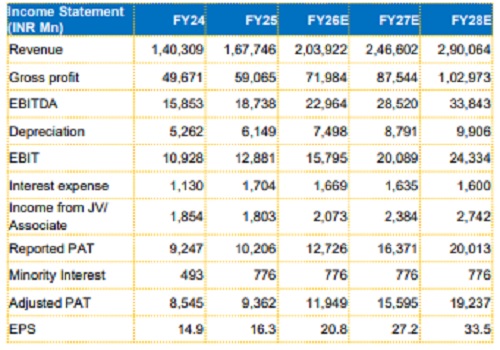

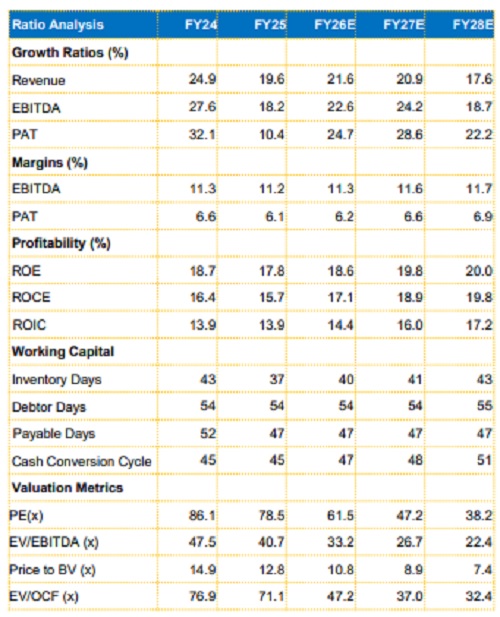

View and Valuation:

UNOMINDA is well-positioned to capitalize on structural tailwinds from premiumization and shift towards electric vehicles in the auto components sector, supported by strategic investments in high growth areas, thereby enhancing long-term growth visibility. We revise our FY27/FY28 EPS estimates upwards by 2.4%/7.3% and arrive at our target price of INR 1,215. We value the company at 40x (maintained) on the average FY27/28E EPS and change our rating to REDUCE from ADD.

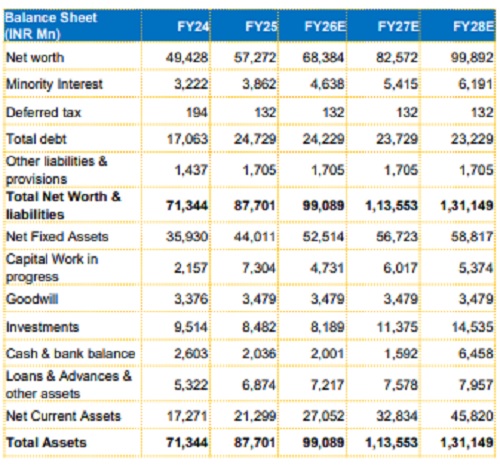

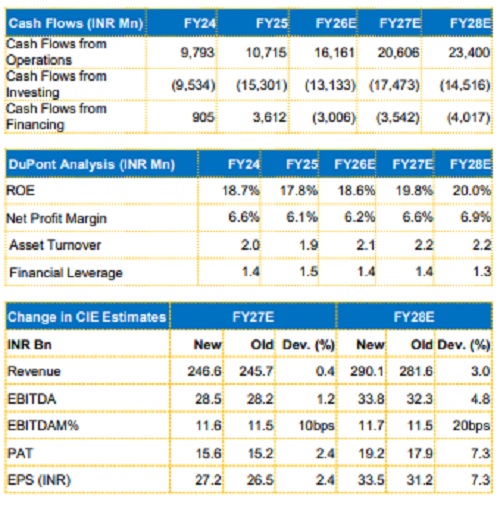

Financials:

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Pantomath Group Appoints Marketing Veteran and Forme...

ACCA Launches Virtual Skills Platform to Help Gen Z ...

Tembo Global Industries to Establish Regional Headqu...

Canara Robeco AMC gets SEBI`s approval to raise fund...

ICICI Pru MF declares IDCW under Banking and PSU Deb...

Baroda BNP Paribas Multicap Fund Celebrates 22nd Ann...

NCC surges on bagging order worth Rs 2,090.5 crore

Quote on Market Wrap 16th September 2025 by Shrikant...

Stock market soars amid India-US trade talks and Fed...

Quote on Gold Commentary 16th September 2025 by Mr. ...

.jpg)