2025-09-16 01:46:33 pm | Source: Choice Broking Ltd

Reduce Motherson Sumi Wiring India Ltd for the Target Rs.48 by Choice Broking Ltd

View and Valuation:

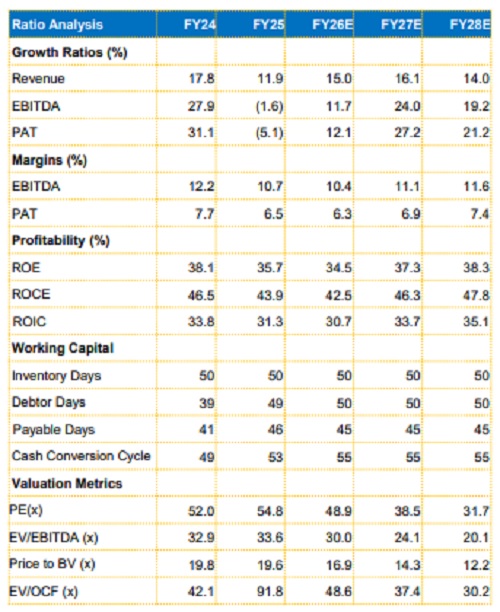

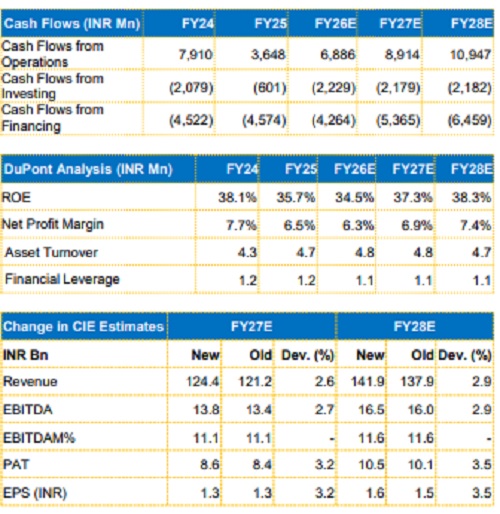

We remain positive on the long-term opportunity as the company is well-positioned to benefit from the industry’s shift towards EV and hybrid powertrains. These are expected to increase the content per vehicle, as the content value for EV programs in passenger vehicles is approximately 1.5 to 1.7 times higher than ICE vehicles. We revise our FY27/FY28 EPS estimates upwards by 3.2%/3.5% and arrive at our target price of INR 48. We value the company at 33x (previously 30x) on the average FY27/28E EPS and change our rating to REDUCE from ADD.

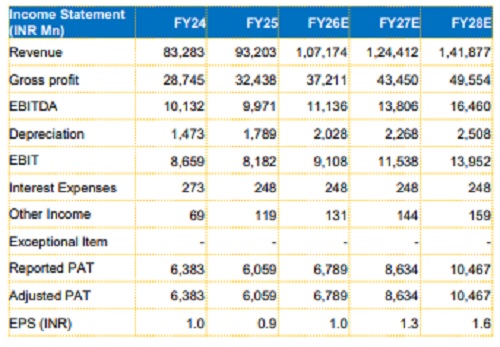

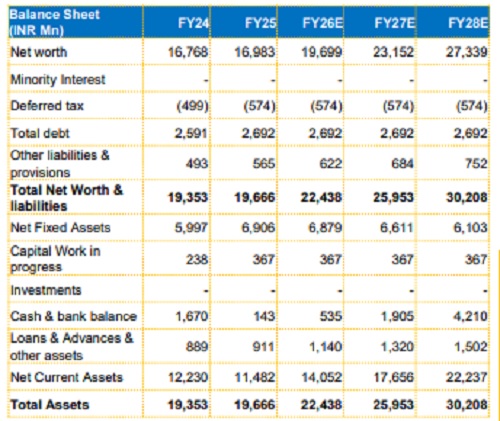

Financials:

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Buy Capri Global Capital Ltd for the Target Rs.640 b...

ITR filing deadline extended by a day to Sep 16

CM Mohan Charan Majhi sets aim to make Odisha the ma...

Centre`s e-Governance drive crosses Rs 3,000cr landm...

Add Centum Electronics Ltd for the Target Rs.3,000 b...

BJP leaders arrive for consultation meeting for upco...

Aadhaar mandatory for online ticket booking in first...

AIADMK General Secretary Edappadi K Palaniswami arri...

All may soon be well in India-US trade relations

Reduce Uno Minda Ltd for the Target Rs.1,215 by Choi...