Neutral Wipro Ltd for the Target Rs.215 by Motilal Oswal Financial Services Ltd

2.jpg)

1Q guidance underwhelming; BFSI impacted by client-specific headwinds

* Wipro (WPRO) reported 4QFY26 IT Services revenue of USD2.6b, up 0.2% QoQ CC, below our estimate of 1.0% QoQ growth. It posted an order intake of USD3.5b (up 3.5% QoQ), with a large-deal TCV of USD1.4b (down 18% YoY). Adj. EBIT margin came in at 17.2% (est. 16%). Adj. PAT stood at INR34.8b (up 3.7% QoQ) vs. our estimate of INR33b.

* In INR terms, revenue/adj. EBIT/adj. PAT grew 4.0%/1.8%/2.2% YoY in FY26. In 1QFY27, we expect revenue/adj. EBIT/adj. PAT to grow 11.9%/13.9%/2.5% YoY. Free cash flow stood at 101.4% of net profit for FY26. FY26 RoE came in at 15.7% (vs. 16.6%/14.4%/15.8% in FY25/FY24/FY23). We believe that broad-based growth across verticals and a stable conversion of deal TCV to revenue will be key to a constructive view. We reiterate our Neutral rating on WPRO with a TP of INR215, implying 14x FY28E EPS.

Our view: Margin headwinds to persist in 1Q

* Top client decline and US BFSI weakness to weigh on near-term growth: 1QFY27 guidance of -2% to 0% QoQ CC (mid-point -1%) suggests another soft quarter despite partial contribution (1.5 months’ impact in 1QFY27) from two large deals. We believe the key drag remains Americas 2, led by a client-specific issue and delayed ramp-ups.

* While management expects normalization from 2Q, we think near-term visibility remains limited due to ramp-up delays and seasonality. We believe that the timely execution of these deals will be key to improving growth visibility. The top client decline in 4Q (8% QoQ in 4QFY26) also points to volatility in large accounts. We now build in an organic revenue decline of 1.8% QoQ cc in 1QFY27.

* Margins could be under pressure in the near term owing to investments and deal ramp-ups: IT Services margins stood at ~17.3%, despite one-month wage hikes and acquisition impact. However, we believe 1QFY27 margins could see pressure, led by: 1) the remaining two months of wage hike impact, 2) lower-margin deal ramp-ups, and 3) continued investments in AI platforms. We estimate ~16.4%/ 16.9% EBIT margin for 1QFY27E/FY27E.

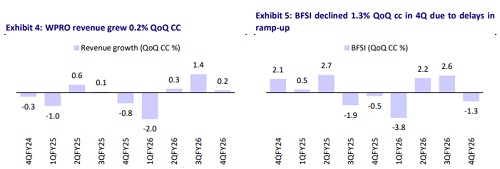

* Vertical performance mixed; recovery still uneven: BFSI was impacted by ramp-up delays and client-specific issues. Technology & Communications continues to lead, supported by AI-led deals, while Healthcare remains weak due to seasonality and policy changes. Manufacturing continues to see pressure from tariffs and demand uncertainty. Overall, we believe a broadbased recovery is still some time away, with growth likely to remain uneven across verticals.

* Deal TCV healthy, but revenue conversion remains the key monitorable: WPRO closed 14 large deals (~USD1.4bn TCV) in 4Q, with continued traction in vendor consolidation and cost takeout. While the pipeline remains healthy, we believe the conversion of deal wins into revenue remains slower than expected, driven by delayed ramp-ups and increasing deal complexity.

* The company announced a ~INR150b buyback (~5.7% of paid-up equity) at ~19% premium, with completion expected in 1QFY27. This is broadly in line with past buybacks (~4–5% of equity), implying mid-single-digit EPS accretion assuming full execution. Combined with dividends, the three-year payout ratio stands at ~88% above its stated policy.

Miss on revenues & guidance and beat on margins; 1QFY27 guidance at -2% to 0% CC

* IT Services revenue at USD2.6b was up 0.2% QoQ in CC (reported USD revenue was up 0.6% QoQ), below our estimate of 1.0% QoQ CC growth. FY26 revenue stood at USD10.4b, down 0.3% YoY.

* 1QFY27 revenue guidance was -2% to 0% in CC terms (mid-point of -1.0% vs - 0.5% expected).

* In 4QFY26, Technology and Communications/Consumer grew 5.3%/1.7% QoQ CC, while BFSI/Healthcare declined 1.3%/4.4% QoQ CC. ? Americas 1 grew 0.3% QoQ CC, while Americas 2 declined 2.6% QoQ CC; Europe stood at 2.0% QoQ CC growth.

* Overall Adj. EBIT margin was 17.2% (up 70bps QoQ) and above our estimate of 16.0%. For the full year, IT services margin stood at 17.2%, up 20bp YoY. ? Adj. PAT was up 3.7% QoQ/down 2.3% YoY at INR34.8b (against our estimate of INR33b). ? WPRO reported a deal TCV of USD3.5b in 4QFY26, up 3.5% QoQ/down 12.6% YoY, while large TCV of USD1.4b was up 65% QoQ/down 18% YoY. For FY26, deal TCV stood at USD16.5b, up 15% YoY.

* Net utilization (excl. trainees) was up 40bp at 83.5% (vs. 83.1% in 3Q). Attrition (LTM) was down 40bp QoQ at 13.8%.

* WPRO proposed a buyback of INR150b at a price of INR250/share (implying a 19% premium of CMP), equating to 600m shares (~5.7% of total paid-up equity share capital).

Key highlights from the management commentary

* Client priorities are shifting, with spending decisions increasingly tied to business outcomes. WPRO is making decisive investments in AI.

* Certain clients are witnessing supply chain disruptions due to geopolitical issues.

* Deal structures vary, with productivity benefits either passed on upfront or over time; the Olam deal follows an upfront structure.

* 1QFY27 revenue guidance is in the range of -2% to 0% QoQ in CC terms (midpoint -1.0% vs expectations of -0.5%), reflecting seasonality, a client-specific issue in Americas 2, and partial-quarter contribution from two large deal wins.

* Capco is playing a more proactive advisory role, helping clients navigate AI adoption, geopolitical trade disruptions, and technology transitions; sequentially and YoY, Capco delivered one of its highest revenue quarters in recent periods.

Valuations and view

* We model ~1.0% YoY CC revenue growth for FY27E, factoring in a weak start (1QFY27E revenue down ~1.0% QoQ CC) and continued near-term headwinds from ramp-up delays, top client decline, and vertical weakness. We also see limited room for margin expansion, given the wage hikes, lower-margin deal ramp-ups, and ongong AI investments. We keep our estimates largely unchanged.

* Further improvement in execution and a stable conversion of deal TCV to revenue will be key to a constructive view. We reiterate our Neutral rating on WPRO with a TP of INR215, implying 14x FY28E EPS.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041