Add Wipro Ltd for Target Rs. 215 by Choice Institutional Equities

2.jpg)

View and Valuation: WPRO delivered a resilient Q4FY26, exceeding expectation on growth and margins despite wage hike and integration headwinds. Strong deal momentum, led by AI transformation and vendor consolidation, supported bookings, while sustained AI investments reinforced its strategic shift towards scalable AI-enabled delivery, albeit with cautious near-term Q1FY27 guidance of -2%-0% in CC terms. Thus, we expect Revenue/EBIT/PAT to expand at a CAGR of 7.8%/8.9%/8.0% over FY26–FY29E and maintain our ‘ADD’ rating with a target price of INR 215, based on FY28E EPS of INR 15.3 at a P/E multiple of 14x.

Margin Strength Drives WPRO Q4 Beat

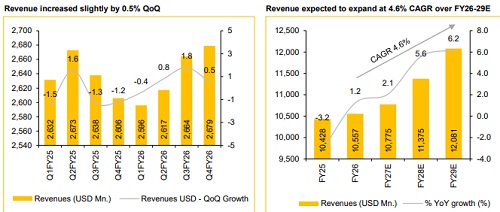

* WPRO reported Q4FY26 IT services revenues at USD 2,651.0 Mn, up 0.6% QoQ (vs CIE estimate of negative 1.7% growth), while, in CC terms, growth stood at 0.2% QoQ. Total revenue (including Products) in FY26 stood at USD 10.6 Bn, up by 1.2% YoY. IT services revenue stood at USD 10.5 Bn, up by 0.8% YoY.

* Operating (EBIT) Margin for IT Services came in at 17.3% for Q4FY26 (vs CIE estimate of 15.6%), down 30 bps QoQ. In FY26, IT services operating margin came in at 17.2%, up 10bps YoY. ? PAT for the quarter came in at INR 35 Bn, up by 12.3% QoQ. Adjusted for impact Labour Code changes, PAT stood at INR 34.9 Bn, up by 3.7% QoQ (vs CIE estimate of 4.5% growth) and EPS for Q4FY26 stood at INR 3.3 (vs CIE estimates of 3.1). For the Full year,

* PAT stood at INR 132 Bn, up 0.5% YoY. EPS for the full year was at INR 12.6. Adjusted for impact Labour Code changes, full year PAT stood at INR 134.3 Bn, up by 2.2% YoY and EPS stood at INR 12.8 per share.

Robust Deal Momentum Driven by Large Deal Wins and AI-led Transformation: Q4FY26 TCV stood at USD 3.5 Bn, up 5% QoQ, where large deal TCV stood at USD 1.4 Bn up 61% QoQ. Total TCV booking for the full year stood at USD 16.4 Bn, up by 15% YoY, while large deal TCV stood at USD 7.8 Bn, up 45.2% YoY. Deal wins were driven by vendor consolidation, AI-led transformation, and semiconductor engineering. Among verticals, Technology & Communications led growth at 5.3% QoQ, while Consumer and EMR remained modest at 1.7% and 1.1% QoQ, respectively. Healthcare declined 4.4% QoQ due to seasonality and the US policy changes, while Manufacturing faced budget pressure from tariffs and input cost volatility. Client spending remains increasingly outcome-focused, with continued prioritisation of cloud, data, and AI as core growth enablers. Management has guided for sequential growth of -2% to 0% in CC terms for Q1FY27.

WPRO to maintain Margins in a narrow band, factoring in ongoing AI-led investments

WPRO reported IT Services EBIT margin of 17.3% up 120 bps, despite fullquarter consolidation of DTS HARMAN and wage hike in March. The management plans to accelerate investments in Wipro Intelligence and its new AI-Native Business & Platform unit as part of its shift towards a “services-assoftware” model. Cost optimisation partly offset this pressure, while AI platform investments are expected to improve delivery efficiency and pricing in the medium term.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131