Neutral Infosys Ltd For Target Rs. 1,650 by Motilal Oswal Financial Services Ltd

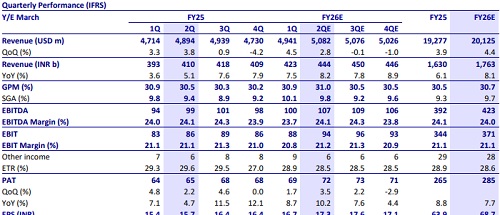

* INFO is likely to clock 2.4% QoQ CC (organic 2.1%), supported by recent deal ramp-ups and 30bp inorganic contribution from its recent acquisition. Growth remains 1H-heavy as in prior years.

* US BFSI to remain resilient, while retail continues to see softness due to tariff uncertainty. Auto is weak, but core manufacturing and industrial segments remain solid from prior wins and could offset this weakness partially

* Operating margin may improve by 40bp due to tailwinds from realization, absence of wage hike, and low thirdparty expenses, though productivity-led AI programs may lead to price compression and margin pressures.

* Expect Infosys to maintain its guidance of 1% to 3% YoY cc.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...