Neutral Hitachi Energy Ltd for the Target Rs 32,000 by Motilal Oswal Financial Services Ltd

Another round of capex to cater to demand

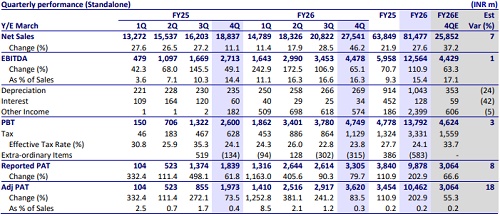

Hitachi Energy’s results came in ahead of our expectations for 4QFY26, led by a beat on both revenue and profitability. For FY26, revenue/EBITDA/PAT grew by 28%/111%/203% YoY. Order inflows for the full year stood at INR185b, up 2% YoY. Excluding exports, which accounted for nearly 25% of total inflows, domestic order inflows (base + HVDC) stood largely flat in FY26. We expect base ordering to start ramping up from domestic markets, driven by strong opportunities from transmission, renewable, data center and exports. The company is also expanding its capacities by another INR20b, potentially adding 30,000-40,000 MVA by 4QCY28. This capex is over and above the existing INR20b capex, which is being done in phases. We incorporate FY26 results and raise our EPS estimates by 8%/6% for FY27/FY28, mainly owing to changes in below-EBITDA line items. We arrive at a revised TP of INR32,000 based on 60x Jun’28E EPS. The stock is currently trading at 110x/75x/54x P/E on FY27/28/29 EPS. Reiterate Neutral rating on the stock.

Beat on revenue and PAT; EBITDA in line

4Q revenue grew 46% YoY to INR27.5b, 7% above our estimate. Gross margin contracted 30bp YoY to 36.9% (vs. est. of 41.6%). While revenue beat our estimates, absolute EBITDA was largely in line at INR4.5b (+65% YoY), mainly due to a lower-than-expected margin of 16.3% (vs. our estimate of 17.1%). Though EBITDA and PBT were broadly in line, a lower-than-expected tax rate resulted in a higher-than-estimated PAT, which jumped 84% YoY to INR3.6b. 4Q inflows increased 11% YoY to INR24b, taking the order book to INR296b (+54% YoY). For FY26, revenue/EBITDA/PAT grew 28%/111%/203% YoY to INR81.5b/ INR12.6b/INR10.5b, while margins expanded 610bp YoY to 15.4%. For FY26, order inflow rose 2% YoY to INR185b (in line) due to HVDC wins in both financial years. NWC remained comfortable at -29 days vs. -28 days in FY25.

Domestic pipeline to remain key growth driver

Overall base ordering and exports, excluding HVDC, remained muted for the company in FY26. However, going forward, the company is expected to benefit from multiple high-growth segments, supported by India’s accelerating energy transition and power infrastructure investments. These include:

1) The planned INR8t transmission investment for integration of ~900GW of non-fossil fuel capacity by 2035, along with increasing opportunities in HVDC infrastructure and grid modernization,

2) The International Finance Corporation’s plans to scale up annual investments in India’s renewable sector to INR920b,

3) The increase in government capex to INR11.2t to support industrial expansion

4) Strong momentum in the data center segment, where cumulative announced investments have crossed ~INR14t. Within data centers, the company estimates its total addressable market at ~15% of the overall capex. We expect overall inflows to increase at CAGR of 13% over FY26-28 on a high base, supported by improved base ordering and at least one HVDC order win annually.

Financial outlook and valuation

For FY27/FY28, we increase our EPS estimates by 8%/6% to factor in FY26 results, mainly on changes in below-EBITDA line items. We thus expect revenue/EBITDA/PAT CAGR of 32%/47%/43% over FY26-28E. The stock is currently trading at 110x/75x/54x P/E on FY27/28/29 earnings. We reiterate our Neutral rating with a revised TP of INR32,000 (vs. INR27,000 earlier), based on 60x Jun’28E earnings.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412