Life Insurance Sector Update : 2H starts on a promising note with industry +19% YoY in retail business by JM Financial Services Ltd

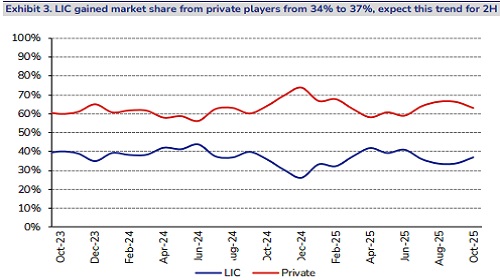

Oct’25 saw industry individual APE grow by 19% YoY to INR 93bn, contributed by 28% YoY growth in LIC’s individual APE, on strong base of 15% decline last October. Private life insurers delivered a steady 15% YoY growth in individual APE, writing INR 65bn of premiums during the month. IPRU turned to growth - with 3% YoY, for the first time in FY26. SBI Life outperformed listed peers with 19% growth while Axis Max Life largely reported its trend growth of 18%, HDFC Life disappointed with 9% YoY growth, on a strong base of 21% in Oct’24.

Group business was weak for both private players and LIC – with the industry growing 9% YoY compared to 35% growth in September. On a 2-year CAGR basis, YTD growth in group APE as of Oct’25 was 18% for the private sector and 14% for the overall industry, aligning with medium-term trends. Among unlisted players, ABSLI (Aditya Birla Sun Life Insurance) posted a weak 5% YoY growth compared to 15% YoY in September, while Bajaj Life registered 7% YoY growth in individual APE.

While SAHIs saw 38% growth on the back of GST 2.0, the life insurers have reported weaker growth as the exuberance was largely limited to lower-ticket protection plans. We project FY26 individual APE growth for the private sector at approximately 12% (vs. 15% in FY25). Against this, the industry has delivered 9% growth in 7MFY26. While questions remain on the impact of ITC on distributor commissions and the resultant growth, we expect the industry (both private sector and LIC) to maintain this 14-15% growth run rate, on a weak base of 2HFY25.

In 2Q concalls, HDFC Life called out a 300bps gross impact on margins, SBI Life 174bps while IPRU and LICI have refrained from disclosing the gross impact. We expect margins to be supported by strength in retail protection (with GST exemption), recovery in credit life (with the underlying industry growth) and wide spread between G-sec yields and deposit rates. At CMP, we prefer LICI and IPRU in the space. With the 2Q results, HDFC Life has seen its valuation premium (to SBI life and Max) narrow, we expect it to gradually increase – despite the GST 2.0 impact, and we expect the company to improve its 1H margins in 2H.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361