IT Sector Update : “Follow-up note explores fears driving sharp de-rating in Indian IT stocks.” by Emkay Global Financial Services Ltd

In continuation of our earlier note, Demystifying Disruption, this follow-up piece attempts to navigate the uncertainties and fears surrounding the unknowns that have driven a sharp de-rating of Indian IT stocks. As clients grapple with a rapidly evolving tech landscape and complexity of integrating AI into legacy systems, we anticipate IT Services companies to move up in the value chain from effort-based execution to consulting-led strategic partnerships as trusted advisors. This deeper engagement is also shifting commercial models from input-based pricing toward outcome-based arrangements. We attempt to i) provide our perspectives on a few common questions; ii) set historical precedents from analogous disruption cycles; and iii) arrive at a grounded view on where multiples should settle through a transition of this nature. Beyond the financial lens, we also examine the evolving dynamics from a business/tech perspective, with an aim to build a more balanced and practical understanding of the structural shifts underway. NIFTY IT is down 13%/17% vs NIFTY over 1M/3M, driven by concerns over the sustainability of the business model and fears that AI advances could disrupt Indian IT Services, leading to trimmed terminal growth assumptions. Factoring in the above, we lower our target multiples by ~20%/32% for IT Services/BPO companies under our coverage. We believe steady operating performance and relevant disclosures to gauge progress on the tech shift will drive investor confidence and recovery in valuations.

AI is reshaping the IT Services landscape… The traditional IT Services’ model is under pressure, as AI automates repetitive, highvolume tasks – once handled by junior engineers. Gen AI delivers material productivity gains in testing, documentation, and legacy migration, raising client expectations for cost savings, especially during renewals. In a low-growth environment, IT Services companies are increasingly compelled to accept aggressive pricing. The traditional staffing pyramid is also flattening as AI agents reduce billable volumes. While legacy work is being cannibalized, enterprise complexity is creating new growth opportunities. Most enterprises still lack clean, integrated data – creating a surge in demand for data engineering, governance, and modernization that act as the prerequisite for AI adoption. Moving beyond basic API calls to building, fine-tuning, and maintaining private, secure industry-specific LLMs/SLMs requires domain expertise and specialized consulting, enabling premium pricing. As AI agents gain autonomy, we believe the need for humanin-the-loop monitoring, auditing, and security could drive new services’ revenue pool that did not exist a few years ago.

…however, the biggest uncertainty is timing The pace at which new services scale relative to the decline in legacy work remains the biggest unknown, in our view. While productivity gains are quick, AI transformation projects face long sales cycles, complex security approvals, and cultural resistance. We also expect IT Services companies to face challenges in capturing new services demand due to skill mismatch (legacy skills’ availability vs AI-native skill demand). Hence, reskilling of the talent base becomes a key element to drive a smooth transition.

Estimate revisions and valuations We lower our earnings estimates for FY27/FY28 by 1%/2%, respectively, for our coverage companies, factoring in our more-conservative growth and margin assumptions. We lower target multiples for IT Services and BPO companies in our coverage by ~20% and ~32%, respectively, to capture conservative assumptions on required terminal growth. We roll forward our valuations to Mar-27E across our IT coverage universe.

We expect consistent performance delivery, along with clearer disclosures on progress over the next few quarters, to gradually restore confidence in the business model, possibly warranting a reconsideration of ratings. Based on our revised TPs, implied terminal growth for large-cap IT Services companies in our coverage is at 5-6% in rupee terms (~1–3% in USD terms), which we consider reasonable given the last 10Y growth trends.

Our pecking order is INFO, LTIM, TCS, HCLT, TECHM, and WPRO in large caps. Among our mid-size IT Services coverage stocks, we prefer COFORGE, HEXT, MPHL, and PSYS.

Precedents, patterns, and perspectives

Every prior tech shift was additive… Every previous tech shift in the modern era—the PC, the internet, mobile, cloud—changed where work happened or how fast it moved, but it did not change who did it. The PC made the individual worker more productive. The internet connected systems and people at zero marginal cost. Mobiles put computers in every pocket. Cloud eliminated infra as a constraint. Each wave was additive: it gave humans better tools, faster pipes, cheaper storage, and expanded the total volume of work to be done. Thus, IT employment grew through each of those cycles rather than contracting (Exhibit 1). Outsourcing and offshoring boomed because more software had to be developed and more systems were needed to be integrated. The productivity gains created demand faster than they displaced labor. IT Services companies play important roles in tech transitions – every tech disruption that threatens them simultaneously creates a multi-year engagement opportunity. Companies that recognized this and leaned in compounded well in the past. However, AI is different in one foundational way: it is the first shift that i) acts on cognition rather than on the infra around it, and ii) is assistive/substitutive rather than being linearly/completely additive in nature.

…while the current tech shift appears to reshape the foundation Prior tech shifts required more labor to implement; this one requires less. Prior shifts attacked the periphery of IT Services delivery (ERP implementation, cloud migration); this one attacks the center (knowledge work). Prior shifts had multi-year adoption curves that gave companies time to retrain and reposition; this one is moving at a rapid pace. Prior shifts required IT Services companies to learn new tools; this one requires them to rethink their position and readjust their business operations. Prior tech was not self-improving; this can improve itself and autonomously act. As a result, this wave is expected to structurally redefine the role of humans – from primary doers to augmented operators and increasingly to checkers or reviewers. We believe companies that stay nimble and adapt quickly to changing realities – embracing outcome-driven models and building proprietary tools, solutions, and IP into their delivery – are best-positioned to emerge stronger once the initial wave of uncertainty settles.

What do previous tech disruptions suggest? All tech shifts have followed a typical pattern. First, the new tech arrives and appears to threaten the existing services model. Second, the market panics and reprices the incumbents downward. Third, the transition itself generates a large implementation wave such that the companies best positioned to execute it—those with the talent depth, client relationships, and delivery infra—have the potential to capture disproportionate value from the very disruption that was supposed to disrupt them. The disruption does not eliminate the need for services; it changes what the services are and the mode of delivery.

Is this time different or just déjà vu in disguise? There has been a familiar debate with every new incoming tech – whether the shift represents a continuation of historical patterns or a structural break from the past. Similar questions emerged during earlier waves of automation, the rise of the internet, and the spread of cloud computing. Questions often centered on whether the rate of tech innovation was accelerating beyond historical precedent, whether the speed of adoption would compress timelines relative to past such transitions, and whether the breadth of sectors affected would be wider than that during previous tech disruptions.

AI raises many of the same open questions: The pace of capability improvements could be faster than in past cycles, even if historical evidence suggests that the diffusion of new technologies across the economy tends to remain gradual. At the same time, AI may affect a broader range of cognitive and knowledge tasks than earlier automation waves, potentially expanding the share of work and jobs that could be automated or augmented. With adoption already running at elevated levels, the scale of disruption and the resulting redistribution of value across industries could prove significantly larger than in prior tech cycles. Whether these dynamics ultimately follow historical patterns or represent a structural break remains an open question.

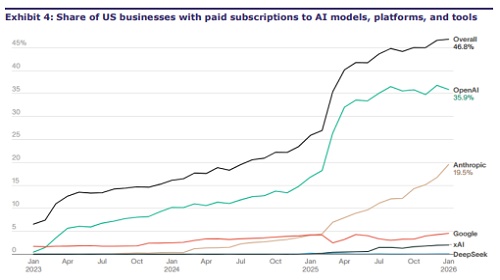

Tech adoption curves are often slower than expected Despite decades of internet adoption, e-commerce still represents only ~16% of total US retail sales (Exhibit 1). This highlights an important pattern observed with general-purpose technologies that their full economic impact typically unfolds over multiple decades, as supporting infra, business models, and user behavior gradually evolve. We believe AI is likely to follow a similar diffusion path, where meaningful transformation occurs over an extended period as enterprises integrate AI into core processes and build the necessary data and operational foundations. However, given today’s digital infra, data availability, and compute capacity, the pace of AI adoption and the scale of its economic impact are expected to be significantly faster and larger than in previous tech shifts.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354