Inflation Data Insights by Abhishek K S, Fund Manager Fixed Income, Abakkus Mutual Fund

Below the Inflation Data Insights by Abhishek K S, Fund Manager Fixed Income, Abakkus Mutual Fund

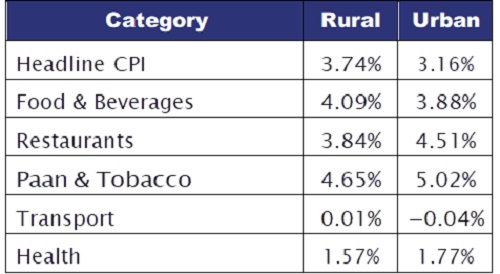

Consumer Price Index (CPI) rose to 3.48% in April 2026, slightly up from 3.40% in March 2026. However it remains comfortably under the RBI's 4% target, even as Brent crude stayed above $110/barrel through most of the month.

At a headline level, the number appears reassuring. However, a closer look suggests that part of the moderation may reflect ongoing efforts by the government and oil marketing companies to contain fuel price pass-through. While this helps cushion inflation in the near term, such measures may only defer, rather than fully offset, underlying pressures from elevated global energy prices.

That said, the current inflation trajectory still provides some comfort, particularly in the context of global uncertainties. With external risks remaining elevated, the RBI is likely to maintain a cautious stance and may refrain from altering the policy rate trajectory in the near term. Going forward, the Monetary Policy Committee (MPC) is expected to remain data-dependent, with a close watch on global developments and their implications for inflation dynamics and external balances, including the current account deficit.

In our view, the RBI is likely to keep rates unchanged in the near term while closely monitoring evolving global conditions and their potential spillover effects.

Key Inflation Drivers

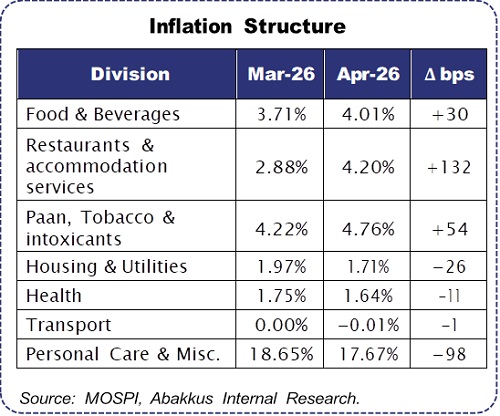

Food inflation emerged as the primary upside driver, rising to 4.20% in April’26 from 3.87% in March’26. The increase was fairly broad-based, with upward pressure from vegetables (notably tomatoes), copra, and edible oils, alongside firming prices across other food categories.

Global edible oil prices have been trending higher, marking the third consecutive monthly increase as per Food & Agriculture Organisation (FAO) data, and this momentum is now increasingly feeding into Indian retail prices.

Partially offsetting these pressures was continued sharp deflation in key vegetable items, particularly potato (−23.7% Y-o-Y) and onion (−17.7% Y-o-Y). These highly volatile components have historically provided a cushion to headline food inflation; however, their ability to consistently offset broader price pressures remains uncertain.

A notable development in the April, was the sharp rise in inflation within the Restaurants & Accommodation Services segment, which increased to 4.20% from ~2.88% in March, an uptick of approximately 130 bps.

This likely reflects the pass-through of higher commercial LPG costs into services pricing, particularly in dining, and points to emerging second-round effects that the Monetary Policy Committee (MPC) closely monitors. Meanwhile, inflation in the personal care and miscellaneous category remained elevated, supported earlier by firm gold and silver prices. However, some recent softening in these prices has led to a moderation of nearly 100 bps within the personal care segment.

While certain volatile food components continue to provide intermittent relief, underlying inflation pressures, particularly in services and non-food segments, remain elevated and need close monitoring.

Above views are of the author and not of the website kindly read disclaimer