Health and Private Insurers Lead Non-Life Premium Growth in May 2026 by CareEdge Ratings

Overview

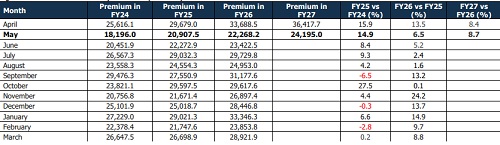

Non-life insurance premiums stood at Rs 24,195 crore in May 2026, registering a growth of 8.7% year-on-year (y-o-y) over May 2025. The industry's performance was primarily driven by strong momentum in health insurance, particularly the retail health segment, alongside sustained growth in motor insurance. The continued outperformance of standalone health insurers (SAHIs) and private sector insurers highlights the increasing importance of retail-focused business within the industry. However, growth remained uneven across segments, with significant contractions in fire and crop insurance partially offsetting gains in health and motor lines.

Figure 1: Movement in Monthly Premium (Rs crore)

Figure 2: Movement in Gross Direct Premium Underwritten (Rs crore)

• The non-life insurance industry reported gross direct premium growth of 8.7% y-o-y in May 2026, improving from 6.5% in the corresponding period last year. Industry growth was primarily driven by private insurers and SAHIs, supported by sustained momentum in retail segments such as health and motor insurance. In contrast, public general insurers witnessed a 3.8% y-o-y contraction in premiums. In comparison, private general insurers recorded healthy growth of 11.8%, reflecting a stronger retail franchise, wider distribution reach, and better customer acquisition. Consequently, the combined market share of private insurers and SAHIs increased to 70.9% in May 2026 from 66.6% a year ago.

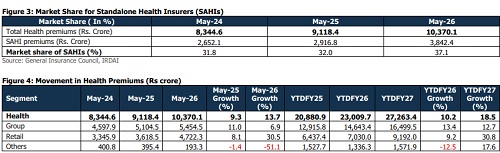

• SAHIs continued to be the fastest-growing segment within the industry, registering premium growth of 31.7% y-o-y in May 2026. The strong momentum reflects sustained demand for health insurance products amid rising healthcare costs, increasing awareness of financial protection, and a growing preference for specialised health insurers. On a YTD basis, SAHIs reported premium growth of 34.0%, significantly higher than the overall industry growth of 8.5%. Furthermore, the sharp y-o-y expansion was also accentuated by a base effect, including the implementation of the 1/n rule. SAHIs maintained their upward momentum, with their market share in health premiums rising to 37.1% in May 2026 from 32.0% y-o-y. (Refer to Figure 3)

• In contrast, specialised PSU insurers witnessed a sharp decline of 94.9% y-o-y in premiums during May 2026. The volatility in this segment is largely attributable to the lumpy nature of business and dependence on a limited number of large policies. Consequently, premiums underwritten by specialised insurers declined by 42.2% YTD.

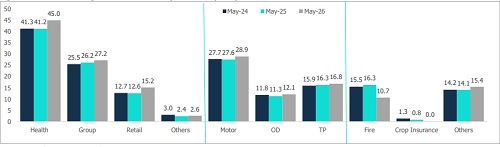

• Health insurance remained the key growth driver for the non-life insurance industry in May 2026, with premiums increasing by 13.7% y-o-y, higher than the 9.3% growth recorded in the corresponding period last year. The segment continued to benefit from sustained demand for health coverage, rising healthcare costs and increasing awareness regarding financial protection against medical contingencies.

• The group health segment registered a growth of 6.9% y-o-y in May 2026, compared with 11.0% growth in the corresponding period last year. While growth moderated, the segment continued to be supported by demand from corporates and employer-sponsored health insurance programmes. General insurers retained a dominant position in this segment owing to their established relationships with corporate clients and broader product offerings.

• The retail health segment remained the strongest-performing category, recording a robust growth of 30.5% y-o-y in May 2026 compared with 8.1% growth a year ago. Growth was supported by increasing adoption of individual health policies, rising medical inflation, higher demand for comprehensive coverage and continued expansion of distribution channels. The strong y-o-y growth was also aided by a favourable base effect. SAHIs continued to strengthen their presence in the retail segment, reinforcing their dominant positioning in the retail health space.

• In contrast, the ‘Others’ health segment contracted sharply by 51.1% y-o-y in May 2026, compared with a marginal decline of 1.4% in the corresponding period last year. The weakness likely reflects lower premium accruals from institutional and niche business segments, as well as the absence of sizeable policy issuances and renewals that had supported premium collections in the previous year. In addition, persistent geopolitical uncertainties in West Asia may have weighed on overseas travel demand, exerting further pressure on this segment.

• Non-life insurance premiums excluding health recorded moderate growth in May 2026, supported primarily by the motor and other segments. While the overall performance benefited from sustained growth in retail-oriented lines, gains were partly offset by a sharp contraction in fire insurance premiums and continued weakness in crop insurance. The other segment remained a key contributor, registering robust growth of 18.4% y-o-y in May 2026 compared with 3.7% growth in the corresponding period last year, likely driven by healthy traction in other liability and miscellaneous insurance products.

* Motor insurance continued to be a major growth driver, with premiums increasing by 11.9% y-o-y in May 2026, compared with 8.2% growth a year ago. Within the segment, Own Damage (OD) premiums grew by 14.6%, while Third Party (TP) premiums increased by 10.1%. The strong performance reflects healthy vehicle sales, continued replacement demand and increasing insurance penetration. Further, any future revisions to third-party motor premium rates could provide additional support for segment growth.

* The fire insurance segment reported a sharp contraction of 24.5% y-o-y in May 2026, reversing the strong growth of 17.3% recorded in the corresponding period last year. The decline may be attributable to heightened competitive intensity in commercial lines, lower premium accruals from large corporate accounts and an elevated base effect. Consequently, fire insurance remained a key drag on overall non-health premium growth during the month.

* Crop insurance premiums continued to remain under pressure, declining sharply during May 2026, reflecting the seasonal nature of premium recognition under government-supported schemes, along with premium reversals related to policy cancellations, subsidy adjustments and reconciliation of earlier underwriting periods. Consequently, the segment reported a significant decline in premiums, underscoring the inherent volatility associated with crop insurance business.

CareEdge Ratings’ View Priyesh Ruparelia, Director, CareEdge Ratings, says, “The non-life insurance industry reported gross direct premiums of Rs 24,195 crore in May 2026, registering a healthy growth of 8.7% y-o-y, supported primarily by strong momentum in health insurance and sustained growth in the motor segment. The continued outperformance of SAHIs and robust expansion in retail health premiums reflect the increasing preference for specialised and customer-centric insurance offerings. Looking ahead, structural drivers such as rising insurance awareness, increasing healthcare costs, expanding distribution networks and greater digital adoption are expected to support industry growth. While health and motor insurance are likely to remain the key growth engines, competitive intensity in commercial lines, particularly fire insurance, may continue to exert pressure on pricing and premium growth. The performance of crop and specialised insurance segments is also Health and Private Insurers Lead Non-Life Premium Growth in May 2026 6 expected to remain volatile due to their dependence on seasonal factors, policy-level adjustments and the timing of premium recognition under governmentsupported schemes. Overall, the industry is expected to maintain a steady growth trajectory in FY27, supported by favourable long-term demand fundamentals. However, growth rates may moderate from the elevated levels witnessed in certain segments during FY26 as base effects gradually normalise. Additionally, geopolitical developments, particularly in West Asia, remain an important monitorable, given their potential impact on global trade flows, freight costs and claims experience across marine, transit and related commercial insurance segments. At the same time, insurers will need to navigate the transition to Ind AS-based accounting standards while maintaining underwriting discipline and profitability amid evolving risk and competitive dynamics.”

Above views are of the author and not of the website kindly read disclaimer