Finance Sector Update : Fresh loan yields witnessing a healthy rise By Motilal Oswal Financial Services Ltd

Pause in policy rates and repricing of TDs augur well for FY27E margins

* Yields on fresh loans rose 44bp for PSBs, 18bp for PVBs, and 39bp for SCBs in Jan’26. This early trend points to a favorable yield environment for banks in 4Q and thus augurs well for margins over FY27.

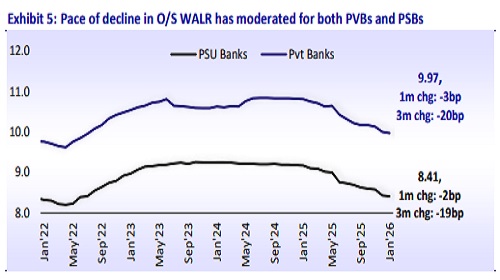

* WALR on O/S loans declined marginally by 2bp MoM, with a 2bp decline for PSBs and a 3bp decline for PVBs. With repo rates stable, the bulk of repo-linked repricing appears to be behind banks.

* PSU banks have reported a relatively lower decline in MCLR rates as deposit rates have been static though select large PVBs may face mild downward pressure due to repo repricing from 25bp cut in Dec’25 policy.

* The Weighted Average Term Deposit Rate (WATDR) for the system continued to decline at a calibrated pace by 4bp MoM in Jan’26 to 6.74%, with PSBs and PVBs reporting a 4bp and 3bp dip MoM, respectively.

* Systemic credit growth has recovered to 13.7% (11% YTD) and has remained above 13% YoY in recent fortnights, indicating a sustainable uptrend. The RBI’s comfort on elevated CD ratios further eases funding concerns. We raise our systemic loan growth estimate to ~14% CAGR over FY26-28E.

* Top picks: ICICI Bank, HDFC Bank, SBI, and AUBANK.

Fresh loan yields expand 39bp MoM; O/S loan yields stable MoM

* Yields on fresh loans rose 44bp for PSBs, 18bp for PVBs, and 39bp for SCBs in Jan’26. This early trend points to a favorable yield environment for banks in 4Q and thus augurs well for margins over FY27.

* WALR on O/S loans declined marginally by 2bp MoM to 9.04% in Jan’26 following a dip of 15bp in Dec’25. PSBs O/S yield declined by 2bp MoM, and that of PVBs declined 3bp. With repo rates stable, the bulk of repo-linked repricing appears to be behind banks.

* One-year MCLR for PVBs dipped 30-275bp over the past year. Bandhan/KMB/ HDFC reported a steeper decline of 275bp/115bp/100bp YoY, while IDFCFB/IIB witnessed a lower decline of 55bp YoY. PSBs MCLR rate has witnessed a more calibrated decline at 30-40bp YoY.

* With repo rates now being stable, O/s yields becoming steady, and incremental fresh loan yields improving over the past three months, incremental yield decline is likely to be calibrated. The continuous repricing of TDs should thus augur well for FY27E NIMs

Calibrated decline in WATDR continues; bodes well for CoF moderation

* WATDR is easing at a measured pace, declining 4bp MoM in Jan’26 following a 5bp MoM dip in Dec’25.

* With term deposit repricing progressing gradually, the WATDR spread over the repo rate remains at a four-year high of ~1.5% for both PVBs and PSBs, indicating that the impact of lower rates is likely to become evident in 4QFY26 and 1HFY27E.

* Consequently, the ongoing moderation in WATDR should translate into a reduction in the overall cost of funds, with a positive spillover to NIMs.

Growth recoups to 13.7%; estimate ~14% loan CAGR over FY26-28E

* Systemic credit growth improved to 13.7% (11% YTD growth) and remained consistently above 13% YoY over the last four fortnights.

* This appears well positioned to sustain, supported by multiple growth engines – steady retail demand (anchored by reviving unsecured growth), and pickup in SME/corporate demand as well, and revival in consumption-led momentum.

* Importantly, RBI’s indication that elevated CD ratios will not be a binding constraint alleviates funding concerns, especially as deposit repricing and liquidity measures ease system tightness.

* Further, strengthening corporate balance sheets, rising capacity utilization, and gradual rate moderation provide incremental tailwinds, suggesting the current momentum is sustainable toward mid-teens growth over the medium term.

* We expect earnings growth to lead loan CAGR over the medium term, as banks benefit from stable-to-improving NIMs, easing deposit cost pressures, and a favorable rate backdrop.

* We estimate loan growth to be healthy and expect it to sustain a healthy ~14% CAGR over FY26-28E

Our view: Prefer ICICIBC, HDFCB, SBI, and AUBANK

* The Indian banking sector has delivered resilient NIMs vs. our expectations in 3Q. Incremental data suggests that banks are generally well-positioned to sustain these NIMs, with a recovery expected over FY27E.

* With a positive growth outlook and systemic growth consistently exceeding 13% YoY over the past few fortnights, we anticipate steady growth trends led by retail, increased SME and corporate demand, and a revival in consumption. Thus, we expect credit growth to sustain at a healthy ~14% CAGR over FY26-28E.

* With asset quality remaining healthy and credit costs trending lower, incremental profitability will increasingly be driven by operating leverage, productivity gains, and tighter cost discipline across select franchises.

* We estimate a PAT growth of 15.1% and 17.8% YoY in FY27E and FY28E, respectively.

* Our top picks remain ICICI Bank, HDFC Bank, SBI, and AUBANK.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Insurance Sector Update: 2QFY26 Preview: All eyes on 2H growth by JM Financial Services Ltd