Daily Derivatives Report 24th February 2026 by Axis Securities Ltd

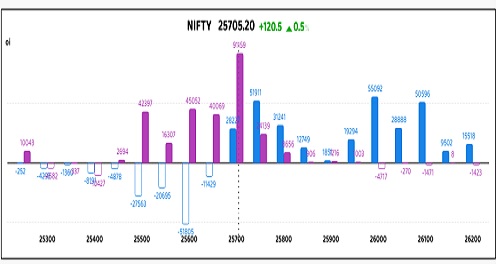

Nifty

The Day That Was:

Nifty Futures: 25,705.2 (0.5%), Bank Nifty Futures: 61,238.0 (0.1%)

Nifty Futures climbed 120.5 points as Open Interest (OI) expanded by 12.67 lakh shares to 198.05 lakh a 6.8% surge confirming a definitive Long Build-up as the index reclaimed the 25,700 psychological handle. Despite a midday dip, the benchmark maintained its upward trajectory as the US Supreme Court's decision to annul sweeping IEEPA-based levies lowered the equity risk premium for emerging market assets, even as a subsequent 15% global tariff proposal was floated. Concurrently, Bank Nifty Futures edged up 58.8 points with OI rising by 0.89 lakh shares to 19.00 lakh, an increase of 4.9% indicating similar bullish positioning; however, momentum in private lenders was checked by some profit-taking, leaving PSU banks to anchor the financial vertical. This global optimism was bolstered by cooling geopolitical tensions in Geneva, which dragged Brent crude down to $71/barrel, providing a favourable macro tailwind for Indian macros. Sectorally, Textiles and Auto components led the charge on the removal of "reciprocal" tariff threats, while the IT sector lagged under continued global guidance pressure. The India VIX retreated to 14.17, shedding 1.40% ahead of the monthly derivative expiry, signalling a contraction in short-term hedging demand as the Rupee appreciated 7 paise to settle at 90.87 against the greenback.

Global Movers:

Wall Street orchestrated a dramatic intraday reversal, as a high-velocity session defined by a paradoxical "Tariff Tantrum" saw the Dow Jones, loss -822 points (-1.7%), 48,804, the S&P 500, loss -72 points (-1.0%), 6,838, and the tech-heavy Nasdaq, loss -259 points (-1.1%), 22,627 all hammered into the red. This massive de-risking event was catalyzed by a sudden escalation in trade rhetoric as a proposed hike in global levies to 15% triggered a yield-curve steepening. Although the US 10-Year Yield was flat at 4.04%, the market has transitioned from "deregulation optimism" to "Tariff Terror," where cost-push inflation fears are paralyzing the Fed's easing narrative. In the commodities pits, a "flight to quality" saw Gold, gains +136 points (+2.7%), 5,265 and Silver, gains +3.78 points (+4.5%), 88 surge as primary volatility hedges, while industrial metals followed a reflation trade navigating a contango structure; meanwhile, Brent Crude, loss -0.08 points (-0.1%), 71 remained trapped as the demand-side drag of trade fears offset the geopolitical risk premium of potential supply disruptions.

Stock Futures:

INDIANB surged 3.6% to a 52-week peak on Long Addition, as open interest climbed 2.6% to 10,940 contracts amid PSU consolidation rumors. Despite the basis contracting 1.7 points to a 3.1-point premium, sentiment remains buoyant with 1,265 new puts eclipsing 638 new calls. This shift propelled the PCR from 0.82 to 0.92, signalling that aggressive put writing is providing a robust floor against minor retracements as institutional conviction hardens.

BHARATFORG clocked a record high after a 2.8% price jump and 1.1% OI expansion, fueled by a 9,467 Cr defense order book. Long Addition dominated the tape, even as the futures premium narrowed slightly to 6.4 points. While 785 new calls slightly outpaced 721 new puts, the PCR held steady at 0.91. This synchronized growth in defense projections and derivative participation suggests a methodical accumulation phase supported by high-conviction institutional buyers.

IDFCFIRSTB underwent a 16.1% collapse on massive Short Addition, with open interest exploding 41.3% to 43,607 contracts following a 590 Cr fraud disclosure. A staggering 20,159 new calls were added as the PCR slid to 0.71, reflecting a radioactive shift in sentiment. With the basis compressing to a 0.26-point premium and 14,000 new puts failing to stem the tide, the data confirms a violent, volume-backed liquidation and structural de-rating.

UPL plunged 14.4% as a global demerger plan sparked 17.1% Short Addition, bringing total futures OI to 27,181 contracts. Bearish concentration was evident as 9,162 new calls dominated 4,058 new puts, causing the PCR to retreat from 0.68 to 0.57. The futures premium contracted by 1.05 points to 3.4, illustrating a vertical descent where the magnitude of call writing reinforces a stiff overhead resistance.

Put-Call Ratio Snapshot:

The Nifty put-call ratio (PCR) rose to 1.06 from 0.98 points, while the Bank Nifty PCR fell from 1.09 to 1.02 points.

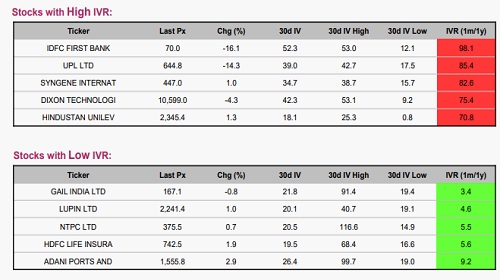

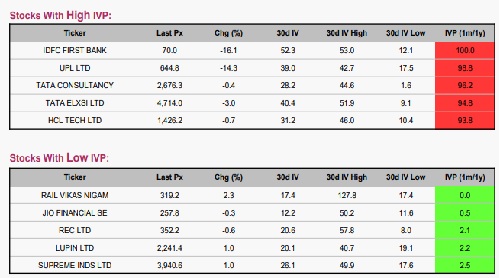

Implied Volatility (IV):

IDFC FIRST BANK and UPL LTD exhibit extreme premium expansion following double-digit price declines of 16.1% and 14.3%, respectively; with IDFC FIRST BANK hitting a 98.1 IVR and UPL LTD at 85.4, the implied volatility skew is heavily bid, creating an environment ripe for premium harvesting as wide-range sell-offs typically transition into volatility crush and price stabilization. Conversely, GAIL INDIA LTD and LUPIN LTD reside in a low-volatility vacuum with IVRs at bottommost levels in F&O segment; despite LUPIN LTD’s 1% gain, the suppressed 30d IV levels (21.8 and 20.1) indicate that the market has yet to price in significant tail risk, suggesting these stocks will remain tethered to their current consolidation zones until a catalyst triggers a volatility mean-reversion.

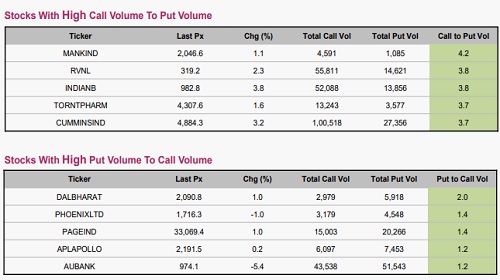

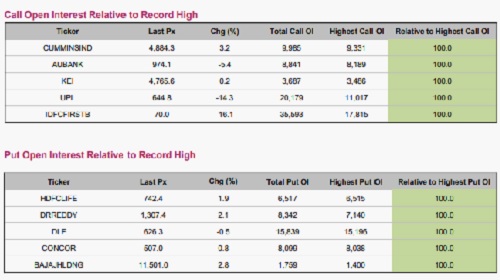

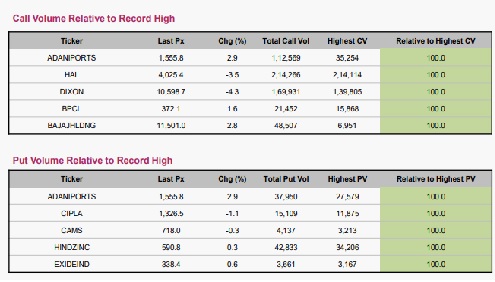

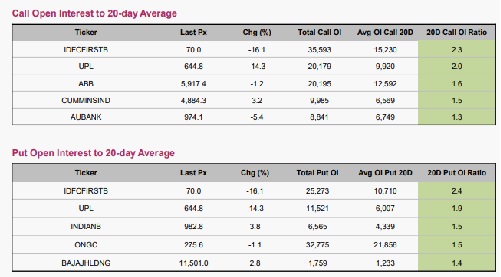

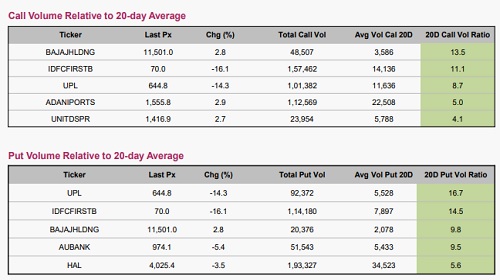

Options volume and Open Interest highlights:

Cummins India and Indian Bank currently exhibit extended bullish momentum with heavily skewed 4:1 call-to-put ratios, a crowded positioning that significantly heightens the risk of sharp profit-taking or a sudden deleveraging pullback. Conversely, while AU Bank and Page Industries have been weighed down by bearish sentiment, emerging seller exhaustion indicates that downward pressure is plateauing, setting the stage for a potential tactical mean-reversion rally. In options positioning, the broader market appears vulnerable to rising volatility as concentrated long bets in UPL and IDFC First Bank the latter recently rattled by fraud disclosures and record-high put concentrations in DLF and Container Corporation suggest a transition into a more reactive and turbulent phase of price discovery. (This data covers only stock options with at least 500 contracts traded on the day for both calls and puts).

Participant-wise Open Interest Net Activity:

Index Futures witnessed a sharp divergence in positioning as Proprietary traders and FIIs aggressively ramped up exposure, adding 6,449 and 4,579 contracts respectively. This institutional accumulation directly countered the massive liquidation from Clients, who shed 6,589 contracts, and DIIs, who pared back 4,439 positions. The shift in Stock Futures was even more pronounced; FIIs and DIIs spearheaded a bullish conviction by pouring in 41,163 and 33,941 contracts. Conversely, Proprietary desks and Clients pivoted sharply toward distribution, offloading 50,020 and 25,084 contracts. This rotation suggests a robust institutional appetite for underlying growth, even as retail participants and local desk traders retreat from broader market volatility.

BankNifty

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633

.jpg)

.jpg)