Capital Markets : MF regulations overhaul: Unexpected but manageable by Kotak Institutional Equities

MF regulations overhaul: Unexpected but manageable

The SEBI has published a consultation paper aimed at areas such as fee transparency and protection. There are a couple of main takeaways for the names we cover: (1) the removal of 5 bps exit load: for the MF value chain, we see ~3-4% impact from the removal of 5 bps exit load; and (2) lowering of TER slabs: this is done to separate statutory cost in TER; we need more clarity to ascertain the impact as there is a risk that some of the decline may not be passed through. Our experience from the 2023 regulatory intervention suggests some of the proposals would get debated extensively.

SEBI proposes new MF regulations

The SEBI has undertaken a comprehensive review of the MF regulations. While the broader purpose is to simplify and shorten regulations covering mutual funds, there are few pertinent items with respect to AMC financials: (1) removal of 5 bps exit load charged to the scheme as part of the overall total expense ratio (TER); and (2) lowering of expense ratio slabs with a view to exclude all the statutory levies (STT, GST, stamp duty, etc.) from expense ratio limits. Some of the other proposals include (1) greater disclosure of TER, including brokerage, exchange and regulatory fees and statutory levy; and (2) enabling differential expense ratios based on fund performance.

Removal of 5 bps exit load: Impactful based on who bears it

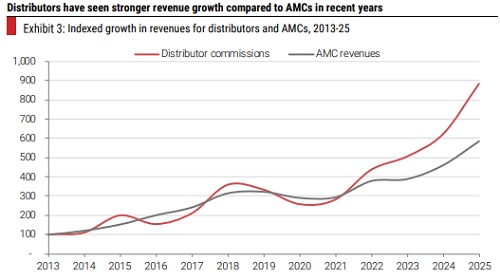

The removal of exit load, while not expected, is probably one of the constant items to undergo cuts: introduced at 1% in 2009, then reduced to 20 bps in 2012 and then to 5 bps in 2018. A 5-bps cut on equity regular TER of 1.8% implies a 3% hit to the value chain. If AMCs were to absorb all the hit, the impact on revenues would be around ~5% and on core PBT around ~10%. However, we note that the comparison of revenue growth between AMCs and distributors reveals a still unbalanced sharing of the industry revenues (Exhibit 3). RTAs could also face additional pricing pressure.

New slab rates on TER: Await more clarity on the impact

The SEBI has also proposed the creation of new expense ratio slabs, which are below current rates on a headline basis by ~15 bps. The consultation paper specifically notes that TER limits are revised downward to the extent of GST on all expenses other than management fees. This implies that GST on distribution commission could be the largest component of the 15 bps cut to TER. We need to ascertain what the actual impact of this is, especially for large players, as distribution commissions could be lower for select large funds.

Brokerage costs: Sharp reduction in allowable costs

There is a proposal to reduce the limit on brokerage cost to 2 bps (from 12 bps) for cash trades and derivatives to 2 bps (from 1 bps). The SEBI has flagged reservations with respect to double charging of research services, i.e., both through the broker and AMCs’ own stock.

Please refer disclaimer at https://www.kotaksecurities.com/disclaimer

SEBI Registration No. INZ000200137