Buy Ventive Hospitality Ltd for Target Rs.790 by Choice Institutional Equities

Scaling Portfolio of Luxury Hotels, Backed by Blackstone

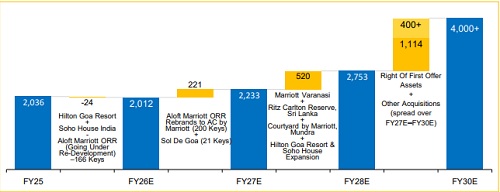

VENTIVE is scaling from a strong base in Pune and the Maldives to a wider footprint across India and Sri Lanka. Anchored by Panchshil Group’s land bank and execution capabilities, and backed by Blackstone’s joint ownership since 2017, which brings institutional capital and governance. VENTIVE is further supported by partnerships with leading hotel brands that ensure global reach and brand depth. VENTIVE’s growth is defined by an aggressive expansion pipeline, targeting a doubling of keys from 2,036 in FY25 to 4,000+ by FY30E. The company is highly acquisitive, as reflected in recent takeovers of Hilton Goa Resort and Soho Hospitality India, indicating a planned push to scale rapidly in the luxury and lifestyle segments.

Diversified Growth Stack Across Micro-markets, Non-room Revenue & Annuities

VENTIVE’s next phase is built on three growth levers: (1) Micro-market-led hotel upside across Pune, Navi Mumbai, Maldives, and Sri Lanka. Commercial absorption, connectivity upgrades, and muted luxury supply support key growth and RevPAR ramp-up at ~7.1% and ~5.2% CAGR, respectively, over FY26E–FY29E; (2) Faster non-room revenue scaling at ~26.7% CAGR over FY26E–FY29E, driven by resilient F&B, MICE, Soho House membership fees, and branded villas; and (3) Stable annuity cash flows from a ~3.4 Mn sq.ft. Grade-A leased portfolio with ~2.7-year average lease tenure and ~15% step-up on renewal

Compounding Margins and Cash Flows Through the Hospitality Cycle

VENTIVE is entering a phase of sustained margin expansion and disciplined capital deployment. EBITDA margin is projected to expand by ~290 bps to 47.5% from FY26E–FY29E, driven by operating leverage and diversifying into higher-margin business mix that improves incremental EBITDA flow through. Post its IPO-related INR 14 Bn deleveraging, lowering interest costs (INR 150–200 Mn p.a.), supporting PAT to free cash flow conversion. The INR 37 Bn pipeline and select brownfield opportunities are expected to be largely funded through internal cash generation, limiting incremental financing needs.

View & Valuation:We initiate coverage on VENTIVE with a BUY rating and a target price of INR 790, implying 36.9% upside. Our valuation is based on FY28E SOTP using 16.0x hospitality Adj. EBITDA and 14.0x annuity Adj. EBITDA. We expect Revenue and Adj. EBITDA to grow at a CAGR of 17.3% and 17.0% over FY26E–29E, driven by key additions, RevPAR growth, scaling non-room revenue, stable annuity cashflows

Key Risks: Extended geopolitical tensions, Project execution delay & geographic concentration of assets.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131