Buy Ultratech Cement Ltd for Target Rs.15,210 by Choice Institutional Equities

Capacity expansion + Cost-efficiency = Sustained earnings growth

We maintain our BUY rating on UltraTech Cement (UTCEM) with a target price of INR 15,210, as our core investment thesis remains intact despite ongoing geopolitical uncertainty. UTCEM continues to strengthen its cost leadership through its Waste Heat Recovery System (WHRS) capacity of 414 MW and renewable energy capacity of 1,392 MW. Management remains focused on driving efficiency, targeting a cost reduction of ~INR 300/t in the next few years. We remain constructive on UTCEM, supported by: 1) Robust capacity expansion pipeline, with planned addition of 15.9 MTPA in FY27E and 29.8 MTPA in FY28E, 2) Strong cost-optimisation initiatives and 3) Favourable pricing outlook in the cement sector. Our EV/CE (Enterprise Value to Capital Employed) framework provides a disciplined approach to valuation, capturing improving fundamentals, including a projected ROCE expansion of ~364 bps over FY26–29E. We expect UTCEM to deliver an EBITDA CAGR of 14.7% over FY26– 29E, driven by: Volume growth assumptions of 8.0%/ 9.0%/10.0% for FY27E/FY28E/FY29E and Realisation growth of 1.0%/1.0%/0.5% over the same period. We derive a 1-year forward target price of INR 15,210/share, valuing UTCEM at an EV/CE multiple of 3.75x for both, FY27E and FY28E. Return ratios are expected to improve, with ROCE rising from 11.5% in FY26 to ~15.1% in FY29E, under reasonable operating assumptions

Q4FY26 result: Margin expansion continues on strong cost control

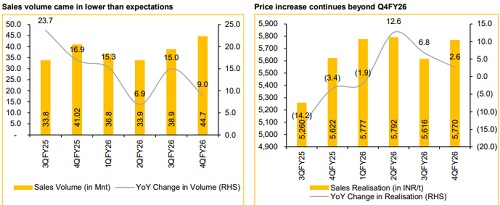

UTCEM reported Q4FY26 consolidated revenue and EBITDA of INR 257.9 Bn (+11.9% YoY, +18.2% QoQ) and INR 56.0 Bn (+21.3% YoY, +43.0% QoQ) vs CIE estimate of INR 268.7 Bn and INR 56.3 Bn, respectively. Total volume for Q4 stood at 44.7 Mnt (including Kesoram & India Cement) (vs CIE est. 47.1 Mnt), up 9.0% YoY.

Cost pressures persist, but mitigation levers in place: Geopolitical tension in West Asia is driving input cost volatility for India’s cement sector, leading to near-term margin pressure. Rising imported coal and petcoke prices remain the biggest concern, where a USD 10/t increase can impact EBITDA by INR 60–70/t. At the same time, higher packaging costs (cement bags) and diesel price are adding to the burden — each 10% increase can reduce EBITDA by INR 15–20/t and INR 25–30/t, respectively. However, management is confident to pass on this cost by hiking the price and increase green power usage. We expect UTCEM EBITDA/t of INR 1,122/t for FY27E due to West Asia conflict’s possibly slight impact.

Key Risks:

Volatile geopolitics: Possible prolonged geopolitical disruption could lead to an increase in petcoke price, resulting in higher input cost and margin pressure.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131