Buy The Phoenix Mills Ltd For Target Rs. 1,996 By Geojit Financial Services Ltd

Project Pipeline Offers Strong Growth Visibility

Phoenix Mills Ltd is India’s leading retail mall developer and operator. It is the pioneer of retail-led, mixed-use developments, with completed development of over 20 million sq ft spanning retail, hospitality, commercial and residential asset classes.

* In Q2FY26, consolidated revenue increased 21.5% YoY to Rs. 1,115cr, driven by strong retail momentum, robust residential sales, improved office leasing and steady hotel income.

* Revenue from property and related services rose 9.7% YoY to Rs. 797cr, driven by 10% YoY rental increase and 14% YoY rise in consumption.

* Revenue from the residential business surged 263.4% YoY to Rs. 175cr, led by Rs. 139cr sales and Rs. 116cr collection at Bengaluru luxury projects, One Bangalore West and Kessaku.

* Retail sales reached Rs. 3,750cr, up 14% YoY, driven by strong growth at the Phoenix Palladium (+13% YoY), Phoenix Mall of Asia (+78% YoY) and Phoenix Mall of Millennium (+27% YoY).

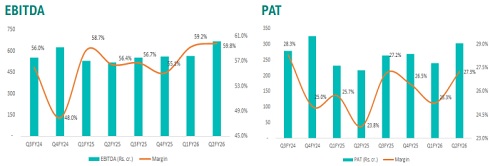

* EBITDA increased 28.8% YoY to Rs. 667cr. EBITDA margin expanded 340bps YoY to 59.8%, driven by strong growth in revenue.

Outlook & Valuation

Phoenix Mills delivered a strong performance in Q2FY26, driven by resilient retail consumption, improving occupancy across office assets and strong traction in residential sales. A strategic focus on experiential retail through concepts such as Gourmet Village, along with expansions into new geographies, is expected to further enhance footfalls and brand visibility. The office portfolio is witnessing robust leasing momentum, while hospitality assets continue to benefit from steady demand recovery. Furthermore, the company's continued emphasis on premiumisation, asset efficiency, and disciplined capital deployment are expected to support robust long-term growth and value creation. Therefore, we upgrade our rating on the stock from HOLD to BUY, with a revised target price of Rs. 1,996 based on 5.4x FY27E adjusted book value per share (BVPS).

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034