Buy Raymond Lifestyle Ltd for the Target Rs. 1,060 by Motilal Oswal Financial Services Ltd

Profitability rebounds due to the mix & operating leverage

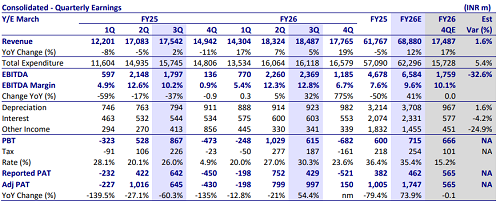

* Raymond Lifestyle (RLL) reported a weak 4QFY26 performance, with EBITDA at INR1.2b missing estimates due to lower gross margins and higher operating costs. PAT was further impacted by the one-off inventory impact of INR0.7b in the apparel business.

* FY26 pre-Ind AS EBITDA rose 56% YoY to INR4.3b, with margins expanding 180bp to 6.2%, aided by operating leverage and improved execution. Reported PAT was INR642m and remained impacted by multiple one-offs.

* Working capital discipline improved materially (up 3% vs. 12% revenue growth), supporting the CFO (after lease & interest) generation of INR1.7b. However, the elevated capex of INR1.8b resulted in marginal FCFF outflow.

* RLL’s legacy textile business continues to provide strong cash flow support, enabling investments in brands and distribution without BS stress. Growth in the garmenting business is also likely to improve posttrade deals.

* FY27 is likely to be a consolidation year for branded apparel, with the focus shifting from aggressive store expansion to sharper brand positioning, channel productivity, and profitable growth.

* Store rationalization and tighter execution should drive ~230bp EBITDA margin expansion over FY26-28E, though meaningful demand-side improvement is likely to be gradual over the next 2–3 years.

* We trim our Pre-IND AS EBITDA estimates by 7% over FY27/28E and build in revenue/EBITDA/PAT CAGR of 10%/28%/45% over FY26-28E.

* Despite near-term drag from losses in newer businesses, RLL’s strong textile franchise and attractive valuation of ~15x FY28E EPS provide favorable risk-reward.

* Reiterate BUY with a TP of INR1,060 (based on 20x FY28E EPS).

Sharp miss on profitability due to higher opex and write-offs

* RLL’s consolidated revenue rose 19% YoY to INR17.7b (vs. our estimate of 17% YoY growth).

* Revenue growth was mainly led by an acceleration in domestic demand, driving improved performance in Branded Textile (up 11% YoY).

* RLL closed net 22 stores in 4Q (35 net closures in FY26), bringing the total retail store network to 1,653.

* Gross profit grew 16% YoY to INR7.2b (in line), while gross margin contracted ~115bp YoY to 40.6% (125bp miss).

* EBITDA grew to INR1.2b (33% miss) due to lower GMs and higher opex/brand investments.

* EBITDA margin stood at 6.7% (~338bp miss).

* Depreciation and amortization jumped 8% YoY (in line), while finance costs rose 4% YoY (4% below).

* RLL posted an exceptional expense of INR700m owing to the loss allowance.

Highlights from the management commentary

* Branded apparel: Healthy same-store demand trends across apparel categories, supported by strong traction in casual wear and premium fabrics such as linen. Focus remains on premiumization, expanding casual categories, improving product mix, and increasing reach through MBOs and large-format stores.

* Emerging businesses: They currently contribute ~INR1.4b in revenue while incurring losses of ~INR0.8b. Excluding these investments, the core branded business profitability remains significantly stronger.

* The garmenting business saw a strong recovery in demand, with March recording the highest-ever monthly revenues. Improved US trade conditions, strong client retention, and healthy order visibility (1Q fully booked; 2Q progressing well) provide confidence for robust growth in FY27.

* Outlook: FY27 would be a year of consolidation, with a focus on profitable and sustainable growth over aggressive expansion. The company plans ~100 gross EBO additions with rationalization of weaker stores, resulting in a net addition of 30–40 stores while targeting double-digit revenue and earnings growth.

Valuation and view

* RLL’s legacy textile business continues to provide strong cash flow support, enabling investments in brands and distribution without BS stress. Growth in the garmenting business is also likely to improve as global sourcing normalizes and trade agreements, including the India–EU FTA, enhance export competitiveness.

* FY27 is likely to be a consolidation year for branded apparel, with the focus shifting from aggressive store expansion to sharper brand positioning, channel productivity, and profitable growth.

* Store rationalization and tighter execution should drive ~230bp EBITDA margin expansion over FY26-28E, though meaningful demand-side improvement is likely to be gradual over the next 2–3 years.

* We trim our pre-IND AS EBITDA estimates by 7% over FY27/28E and build in Revenue/EBITDA/PAT CAGR of 10%/28%/45% over FY26-28E.

* Despite near-term drag from losses in newer businesses, RLL’s strong textile franchise and attractive valuation of ~15x FY28E EPS provide favorable riskreward.

* We reiterate our BUY rating with a TP of INR1,060, based on 20x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

2.jpg)