Neutral PB Fintech Ltd for the Target Rs. 1,870 by Motilal Oswal Financial Services Ltd

30%+ YoY premium growth maintained; beat across all parameters

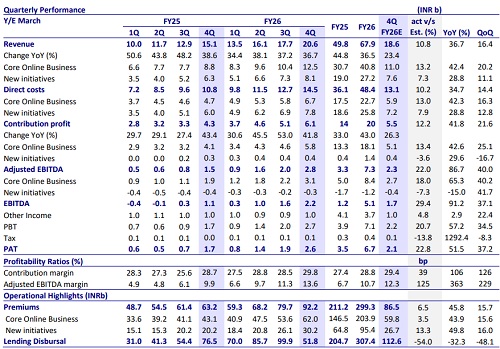

* PB Fintech (POLICYBZ) reported revenue of INR20.6b (11% beat), growing 37% YoY, driven by 42% YoY growth in online revenue to INR12.5b (13% beat) and 29% YoY growth in new initiatives revenue to INR8.1b (7% beat). For FY26, revenue grew 37% YoY to INR67.9b.

* Adj. EBITDA was at INR2.8b (22% beat; +87% YoY) and Adj. EBITDA margin at 13.6% (vs our est. of 12.3%). Core online adjusted EBITDA margin was at 25.1% (21.7% in 4QFY25), while for new initiatives, it was negative at 4.2% (-6.3% in 4QFY25). For FY26, adjusted EBITDA margin was at 10.7%.

* Strong revenue growth, along with robust operational efficiency, resulted in 23% PAT beat, which came in at INR2.6b, up 52% YoY. For FY26, PAT grew 90% YoY to INR6.7b.

* Insurance premium is expected to sustain a 30% growth trajectory. PaisaBazaar is expanding into bonds and mutual funds, along with continued recovery in lending, and has become EBITDA positive with expectations of sequential improvement through FY27.

* We have increased our revenue estimates by 2%/3% for FY27/28, considering the 4QFY26 performance. Improved cost efficiency has resulted in a 2%/5% increase in PAT estimates for FY27/28. We reiterate our Neutral stance with a revised TP of INR1,870 (based on DCF valuation), implying FY28E EV/EBITDA of 53x.

67% YoY growth in protection; lending sees sequential recovery

* Core online premium grew 44% YoY to INR62b, while new initiative premium grew 50% YoY to INR30.2b.

* Lending disbursal for the quarter was INR51.8b (-32% YoY), of which core online lending at INR26.3b continues to grow sequentially. Secured lending (PB Connect) disbursals declined to INR25.5b (INR52.8b in 4QFY24), as the company discontinued credit from wholesale agents.

* The core online insurance take rate improved to 18.2% (17.7% in 4QFY25), resulting in core insurance revenue growth of 48% YoY to INR11.3b. Core online credit revenue grew 7% YoY to INR1.2b, maintaining a sequential growth trajectory.

* New initiatives revenue grew 29% YoY to INR8.1b, backed by 50% YoY growth in new initiative insurance premium, improving insurance take rates, and offset by decline in secured lending disbursals to INR25.5b.

* Insurance renewal revenue annualized run-rate, based on 4Q performance, was INR11.3b (INR6.9b in 4QFY25), providing visibility for continued revenue growth and margin expansion.

* Contribution profit of INR6.1b (12% beat) grew 42% YoY, reflecting contribution margin of 29.8% (vs our est. of 29.4%). For FY26, contribution margin was at 28.8%.

* ESOP expenses for 4Q were INR620m. Other income was at INR1,040m.

* Policy bazaar platform’s registered customer base grew to 145.7m (104.8m in 4QFY25), with transacting customers at 26.4m (20.6m in 4QFY25). The platform has sold 67.3m policies to date. ? Paisa bazaar platform witnessed 7.5m transacting customers (6.3m in 4QFY25), with 58.5m credit scores accessed and 11.3m transactions to date. 87,000 credit cards were issued during the quarter.

Highlights from the management commentary

* PB Health acquired one operational hospital (Annual PAT of INR200-300m), with 2-3 others in the pipeline. The company is also looking at opportunities beyond Delhi NCR, with potential capital raise discussions underway.

* The protection segment grew 67% YoY, with health contributing higher than term. However, term insurance is gaining momentum and is expected to potentially rival the growth trajectory of health insurance going forward.

* Paisabazaar’s entry into savings business through bonds and mutual funds is expected to be fully built out in the next 2-3 years. While the bonds business provides a strong growth opportunity, competitive intensity is high in mutual funds, which will have to be tackled through innovative differentiations.

Valuation and view

* POLICYBZ continues to deliver strong volume growth in 4QFY26, above its guidance of 30%, driven by GST exemption-led boost in term and health insurance. Strong momentum in the protection segment, along with operational efficiency on the back of productivity improvement, resulted in robust profitability. We believe POLICYBZ holds a strong position in two of India’s most under-penetrated financial services segments, complemented by embedded optionality from new initiatives that offer further long-term convexity. Over FY26-28, we expect POLICYBZ to post a strong CAGR of 28%/73%/40% in revenue/EBITDA/PAT, factoring in a strengthening position in the underpenetrated credit and insurance industries. However, the potential risk of commission caps on take rates remains the key monitorable.

* We have increased our revenue estimates by 2%/3% for FY27/28, considering the 4QFY26 performance. Improved cost efficiency has resulted in 2%/5% increase in PAT estimates for FY27/28. We reiterate our Neutral stance with a revised TP of INR1,870 (based on DCF valuation), implying FY28E EV/EBITDA of 53x.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412