Buy Piramal Finance Ltd for the Target Rs. 2,220 by Motilal Oswal Financial Services Ltd

A cleaner and stronger Piramal: Retail engine in full throttle

Retail momentum strengthens, setting the stage for an RoA expansion

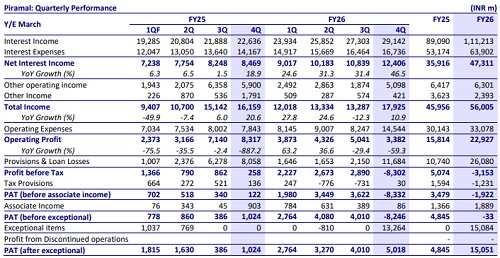

* Piramal Finance (Piramal) 4QFY26 net profit stood at ~INR5b (PQ: ~INR4b). FY26 PAT stood at INR15b (FY25: INR4.85b). NII in 4QFY26 rose 46% YoY to ~INR12.4b. Other income stood at ~INR5.5b (PY: INR7.7b and PQ: INR2.5b).

* During 4Q, Piramal agreed to the sale of its entire equity stake of ~15% in Shriram Life Insurance for a consideration of ~INR6b. The company has received the said consideration, and a net gain of ~INR2.6b was recognized in 4QFY26. Piramal also fully wrote off ~INR5.9b related to land development charges under investment property. This was because the original developer’s LOI was cancelled, and no alternate developer could be appointed within the required timeline, leading to a full impairment of the asset.

* Piramal also received ~INR13.3b as deferred consideration for the sale of its Imaging business, which was recorded under exceptional items. The company utilized the deferred consideration and gains from the Shriram stake sale to reduce the legacy book, without impacting its net worth.

* The opex-to-AUM for the company’s retail business declined to ~3.6% (PQ: 3.8%). Retail opex-to-AUM declined by ~290bp over the last 12 quarters. After a six-quarter pause in branch expansion, the company added more than 100 branches in 4QFY26, while still reporting a decline in cost ratios. It plans to open ~180 gold loan branches in FY27 and remains confident of further reduction in opex ratios, driven by productivity and efficiency gains.

* Total AUM grew 25% YoY and ~5% QoQ to INR1.01t. Wholesale 2.0 AUM grew ~38% YoY to INR125b, while Wholesale 1.0 AUM declined ~59% YoY/ 46% QoQ to INR28b. Growth to Legacy AUM mix has improved to 97%:3% in Mar’26 from 34%:66% as of Mar’22.

* Piramal indicated that retail loan growth continues to remain robust and well diversified across segments, including unsecured lending. The company guided for ~25% AUM growth in FY27 and remains on track to scale up to ~INR1.5t in AUM by FY28.

* Piramal is entering a phase where scale benefits, lower operating costs, and a stable credit framework are expected to drive RoA expansion. Key structural levers include NIM improvement (supported by better product mix and lower cost of borrowings) and enhanced operating efficiency. We estimate a total AUM CAGR of ~24% and a total PAT CAGR of 56% over FY26- FY28, with an RoA/RoE of 2.6%/12% in FY28. We reiterate our BUY rating on the stock with a TP of INR2,220 (based on Mar’27E SoTP).

Healthy retail loan growth of 33% YoY; retail mix improves to 85%

* Piramal’s retail AUM grew ~33% YoY to INR859b, with its share in the loan book rising to ~85%. Retail disbursements grew ~34% YoY to INR131b.

* Consol. NIM rose ~25bp QoQ to 6.5% (PQ: 6.3%). Management indicated that margins are expected to improve, supported by both asset-side levers (favorable product mix and expansion into higher-yielding segments) and liability-side benefits, with CoF likely to decline by ~50-80bp over the next 2-3 years, driven by credit rating upgrade and liability repricing. We expect an NIM (calc.) of 5.6%/5.9% in FY27/FY28 (vs. 5.2% in FY26E).

Asset quality improves with broad-based improvement across subsegments

* GS3 declined ~30bp QoQ to ~2.2%, while NS3 also dipped ~30bp QoQ to 1.6%. Stage 3 PCR rose ~175bp QoQ to ~30%. Total ECL/EAD was stable QoQ at ~2.1% of the AUM.

* Retail Business 90+ dpd declined ~20bp QoQ to 0.6%.

* Capital adequacy (CRAR) stood at ~19.8% as of Mar’26 (vs. ~20.3% in Dec’25).

Highlights from the management commentary

* Management indicated that even if geopolitical stress persists, portfolio impact is expected to be lagged by 2-3 months due to borrower buffers, with no impact likely in 1QFY27 and any stress potentially emerging only in 2QFY27 (Jul-Aug’26). However, management highlighted that early indicators such as bounce rates remain stable, with Apr’26 trends in line with Mar’26.

* The company remains open to M&A opportunities in MFI, MSME, and gold loans, with a focus on value-based acquisition.

Valuation and view

* Piramal reported a healthy operational performance during the quarter, led by strong growth in its retail loans and continued scaling down of the legacy wholesale book, which now accounts for <3% of total AUM. Asset quality improved across all key product segments (including unsecured segments), leading to a sequential decline in credit costs. With rising retail traction and lower incremental CoB, NIM expanded further, reinforcing the shift toward a more stable and profitable lending model.

* Our earnings estimate for FY26 and FY27 factors in gains from the AIF exposures and zero tax outgo in the foreseeable future. We estimate a total AUM CAGR of ~24%, a ~25% CAGR in Retail AUM, and a total PAT CAGR of 56% over FY26- FY28, with an RoA/RoE of 2.6%/12% in FY28. We reiterate our BUY rating on the stock with a TP of INR2,220 (based on Mar’28E SoTP).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Poonawalla Fincorp gains on raising Rs 250 crore through NCDs