Neutral NTPC Ltd for the Target Rs 393 by Motilal Oswal Financial Services Ltd

In-line 4Q; RE to drive capacity growth

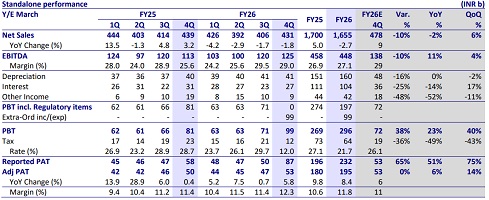

* NTPC’s standalone APAT was in line in 4QFY26, while revenue and EBITDA came in 11% below our estimates, mainly due to soft generation trends (coal PLF for 4QFY26 was 76.16% vs. 81.24% in 4QFY25). Standalone FY26 revenue/EBITDA/APAT stood at INR1,655b/INR448b/INR189b (-2.7%/- 2.1%/+4.8% YoY).

* Key things we liked about the result:

1) a spike in power demand should support strong PLFs in 1QFY27

2) NTPC Green Energy (NGEL)’s generation grew 114% YoY in FY26

3) NTPC guided group commissioning of 9.5GW in FY27 rising to 11.4GW in FY29

4) continued progress on capacity addition in PSP, with COD declared for 250MW in FY27YTD and another 3–5GW expected to be commissioned by CY32/CY33, and 5) renewable PPA tie-ups remain healthy, with FY27/FY28/FY29 capacities tied up to the extent of 79%/71%/66%, respectively.

* Key monitorables:

1) moderation in coal PLF (72% in FY26 from 77.4% in FY25)

2) reduction in thermal capacity addition targets for FY27/FY28 to 1,070MW/1,460MW vs. the earlier guidance of 1,600MW/2,120MW

3) execution-related risks as in FY27 only ~57% of projects have firm connectivity, while 38% are under temporary GNA (TGNA)

4) the pace of NGEL’s capex for FY27/FY28/FY29 (vs. target of INR358b/ INR560b/INR480b)

5) commissioning on the nuclear front with one unit of the Mahi Banswara project expected to be commissioned by 2032, followed by staggered commissioning of the remaining units at six-month intervals.

* Valuation : We reiterate our Neutral rating on NTPC with a TP of INR393. Our TP is based on the value of INR233 for the standalone, coal, and other businesses at Dec’27E P/B of 2x; the value of INR19 for other subsidiaries and INR64 for JV/associates at Dec’27E P/B of 2x, and the stake in NGEL is valued at a 25% discount to the current market price.

Highlights of the 4QFY26 performance

Operational performance

* Commercial generation in 4QFY26 was down 4% YoY, while FY26 generation declined 5% YoY to 352.5BUs. Coal PLF for 4QFY26 stood at 76.2% (vs. 81.2% in 4QFY25).

* NTPC Group’s capacity increased to 89.1GW at the end of FY26 from 79.9GW at the end of FY25.

Capacity addition & project pipeline

* NTPC Group added ~9.6GW capacity in FY26 (1,823MW under standalone NTPC and 7,795MW through JVs/subsidiaries, including the acquisition of a 1,350MW thermal asset with MAHAGENCO).

* Renewable energy additions through NGEL stood at 4.2GW during FY26, including ~2.1GW in 4QFY26.

* Trial operations for Patratu Unit-2 Stage-1 were completed in Q1FY27, while Unit-3 is expected to be commissioned during FY27.

Commissioning targets

* FY27 target: 9,557MW (Thermal: 1,070MW; Hydro: 250MW; RE: 8,237MW).

* FY28 target: 10,039MW (Thermal: 1,460MW; Hydro: 444MW; RE: 8,135MW).

* FY29 target: 11,478MW (Thermal: 3,070MW; RE: 8,408MW).

Valuation and view

Our TP of INR393 for NTPC is based on:

* Value of INR233 for the standalone, coal, and other businesses at Dec’27E P/B of 2x.

* Value of INR19 for other subsidiaries and INR64 for JV/associates at Dec’27E P/B of 2x.

* The stake in NGEL is valued at a 25% discount to the current market price

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412