Buy Physicswallah Ltd For Target Rs.140 By Elara Capital

Community flywheel to cash powerhouse

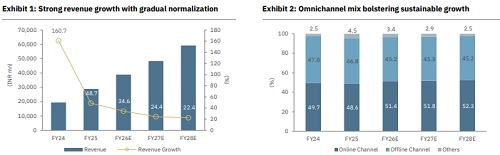

Physicswallah (PWL IN) has mastered an omnichannel education playbook: foster trust and engagement first, monetize later. Its community-led digital funnel—anchored by flagship JEE & NEET courses, expanding vernacular & category depth, and low-barrier entry—now fuels paid online cohorts and a higher-ARPU offline network. With momentum in engagement, enrolments, and center expansion, we expect a revenue CAGR of 27.0% and EBITDA CAGR of 84.7% during FY25-28E, with adjusted PAT turning positive in FY27E and rising to INR 6.7bn by FY28E. We initiate on PWL with a Buy rating and a TP of INR 140 once offline utilization improves and the cash engine funds adjacencies without balance sheet strain.

Community-powered cash engine: PWL’s low-CAC model turns trust into enrolments and engagement into revenue. Free content draws learners, who upgrade to paid courses, tests, doubt-solving, and tools, bypassing heavy marketing. The flywheel scales robustly: 134mn social followers, 83mn app downloads, ~3.4mn daily active users (DAU), and 4.37mn paid enrolments in 9MFY26. Engagement metrics guide targeted expansion by city, category, and segment, transforming community reach into scalable revenue

Offline -- Online’s high-ARPU extension: Offline centers cater to students craving classroom structure and intensive support, forming PWL’s premium monetization funnel. Within 3–4 years, it has surged into a Top 5 company with ~318 centers across 200 cities and ~413k paid offline enrolments in 9MFY26. The hybrid model bolsters scalability by minimizing star faculty reliance and standardizing delivery. Digital trust here unlocks longer-duration, higher-value revenue. We expect an offline revenue CAGR of ~25.5% during FY25-28E, with pre-IndAS EBITDA nearing break-even in FY27E and turning positive in FY28E

Cash generation fuels new engines: PWL pairs hypergrowth with robust cashflow. Upfront fee collections drive negative working capital, while centralized content and technology ensure efficient scaling. As on December 2025, treasury stands at INR 50.5bn, with 9MFY26 operating cashflow of INR 6.4bn and cumulative FCF of INR 21.8bn during FY26-28E. It self-funds expansion and adjacencies. The core business is generating cash to build the next growth engines, while capital allocation remains disciplined and follows repeatable playbooks.

Initiate with a Buy rating and SOTP-based TP of INR 140: We initiate coverage of PWL with a Buy rating and a TP of INR 140, implying 39% upside fromthe current levels. We applya SOTP valuation to PWL’s dual engines: a mature, profitable online business and a fast-scaling offline one. We assign the online business at 30x one-year forward EV/EBITDA, 3.5x one-year forward EV/Sales to offline business and 1.0x one-forward EV/Sales to other operating revenue. At CMP, the stock trades at 36.4x FY27E EV/EBITDA & 23.4x FY28E EV/EBITDA and 78.4x FY27E P/E & 43x FY28E P/E, which we view as attractive for its medium-term earnings compounding and self-funded growth. Risks include coaching regulations, slower offline utilization ramp-up, and faculty retention & execution challenges.

Investment Rationale

Masters an omnichannel education playbook: foster trust and engagement first, monetize later. Low-CAC model targets expansion by city, category, and segment, transforming community reach into scalable revenue Offline expansion monetizes digital reach, improving ARPU, revenue mix and margin. Digital trust here unlocks longer-duration, higher-value revenue. Offline revenue CAGR of ~25.5% during FY25-28E Strong cash generation and negative working capital enable self-funded, scalable growth. The core business is generating cash to build the next growth engines.

Valuation triggers

* Offline build-out, category expansion, and select M&A additional growth levers

* Under-penetrated States to provide the next leg of flagship growth in the online segment

Our assumptions

* Revenue CAGR of 27.0% and EBITDA CAGR of 84.7% during FY25–28E, driven by online scale, offline expansion, and monetization

* EBITDA margin to expand, led by low CAC acquisition, negative working capital, and operating leverage

* Asset-light, cash-rich model supports reinvestment and scalable growth.

Key risks (downside)

* PWL has India’s largest organically built student community (125mn), with a strong omnichannel presence in online and offline segments

* Lowest cost structure, industry-leading affordability, and strong brand trust drive scalable growth and create high-entry barriers.

Please refer disclaimer at Report

SEBI Registration number is INH000000933