Buy OSWALPUM Ltd for the Target Rs.450 by Choice Institutional Equities

Backward Integration to Boost Margin by 200 bps over FY26–FY29E

FY26 EBITDA margin contracted by 381bps YoY to 24.9% due to competitive tender pricing and input cost pressures. The planned investments towards 1.5 GW solar module expansion, aluminium extrusion and EVA manufacturing are expected to complete by FY27E-end. This will add to OSWALPUM’s backward integration competence, boosting margin in the medium term. Aluminium, steel and silver prices have moved up by 20–30% in the last one year, impacting margins. However, we expect a higher realisation in KUSUM 2.0 to offset this input cost pressure. As a result, we forecast EBITDA margin to rise from 25% in FY26 to 26.9% by FY29E.

Valuation & View

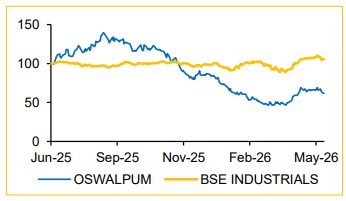

We cut our revenue estimate for FY27E / FY28E by 5.8% and 7.6%, respectively. This is primarily driven by an expected slower H1FY27E. We now anticipate Revenue / EBITDA / PAT CAGR of 17.3% / 20.4% / 17.8% over FY26–FY29E. We value OSWALPUM using the DCF approach at INR 450 (maintained) on the basis of expectation of announcement of KUSUM 2.0 in Q2FY27E-end. Our valuation implies a PE of 11.6x on FY28E EPS. Thus, we retain our 'BUY' rating, given an upside of 21.3%.

Risk to Our Valuation

Delayed KUSUM 2.0 announcement, lower allocation of solar pumps in KUSUM 2.0, higher input cost coupled with slower realisation growth

Q4FY26 Shows Margin Pressure amid RM cost Volatility

* Supplied 21,265 Solar Pumps and 19,170 Non-solar Pumps

* Overall net revenue grew by 39.8% YoY to INR 5.1 Bn

* Gross margin declined by 211 bps YoY / 91 bps QoQ to 38.4%. EBIDTA came in at INR 1,181 Mn, with a margin of 23.2%, declining by 393 bps YoY

* PAT margin rose by 57 bps YoY / declined by 12 bps QoQ to 18.2%. Reported PAT came in at INR 925 Mn, rising by 44.4% YoY

FY26 Revenue Growth a Bright Spot; Margin Weak

* Supplied 87,323 Solar Pumps, +22.7% YoY. 180,908 Pumps supplied (Solar + Non-solar,+14.8% YoY)

* Overall net revenue grew by 44.3% YoY to INR 20.64 Bn

* EBIDTA came in at INR 5.1 Bn, with a margin of 24.9% (-445 bps)

? Reported PAT came in at INR 3.8 Bn, rising by 34.1% YoY

We Expect KUSUM 2.0 announcement by end of Q2FY27

As on date, OSWALPUM has a revenue visibility of INR ~3 Bn / 19,912 pumps. We expect KUSUM 2.0 to roll out by Q2FY27E-end, with provision for intra-state subsidy utilisation and higher realisation. PM Suryaghar Yojna, rooftop solar, commercial and industrial solar projects are being undertaken on a pilot basis by the company with the aim of diversifying its revenues.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131