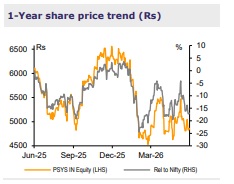

Add Persistent Systems Ltd for the Target 5,200 by Emkay Global Financial Services Ltd

Persistent Systems (PSYS) announced the acquisition of Germany-based Nagarro through a voluntary public takeover offer, valuing the company at an EV of ~€1.27bn (~1.3x/9.2x CY25 revenue/adj EBITDA), creating a ~$2.9bn AI-led digital engineering leader. Strategically, the acquisition strengthens its European footprint, enhances AI-led engineering capabilities, and creates a more balanced revenue mix across clients, verticals, geographies and offerings. With limited client overlap, Nagarro complements PSYS's existing portfolio while expanding the combined entity's TAM to over $1.4tn. The acquisition aligns with management's objective of scaling its European presence through large-scale M&A, although we view the valuation as slightly stretched and expect the near-term reported EPS dilution. Further, the recently announced large deal win (TCV: >$650mn) with a US-based tech major is expected to partially cushion near-term earnings dilution impact. We expect the stock to face a near-term overhang due to inherent execution risks in a scaled transaction (70%/65% of PSYS’s revenue/employee base), EPS dilution concerns, and an elevated risk profile from balance sheet leverage. We have not yet incorporated the transaction into our estimates pending closure. We maintain ADD and TP of Rs5,200 at 30x Mar-28E EPS

Transaction contours

PSYS has incorporated 'Galaxy Germany Holding SE' (BidCo), a wholly owned German subsidiary, to execute the transaction. BidCo has signed a binding SPA to acquire the ~21% stake (excluding treasury shares) from the largest shareholder, Lantano Beteiligungen, for €81/share, followed by a voluntary public takeover offer for the remaining shares at €81/share in cash. Nagarro’s management, holding ~13%, has also indicated its intention to tender, implying ~33% committed support. The transaction is subject to a minimum acceptance condition of 50%+1 share (including the SPA stake) and requisite approvals, with completion contingent on open offer participation.

Funding and post-acquisition plans

The acquisition will be funded through a committed €1.4bn, 18M bridge facility, (EURIBOR + 175–250bps; 4.1-4.8%), including the potential refinancing of Nagarro's existing debt. The deal is expected to close by Q4CY26/Q1CY27. Post completion, PSYS intends to delist Nagarro from the Frankfurt Stock Exchange while preserving its operating structure and separate brand under the ‘Persistent–Nagarro Group’ with a DPLTA (domination/profitand-loss transfer agreement) explicitly ruled out for at least 2Y. (Exhibit 5/6)

Our view on the transaction

We expect near-term sentiment to remain cautious despite the strategic rationale. The transaction materially increases execution risk given its size, funding structure, and integration complexity. While the BCA provides continuity by preserving Nagarro's operating structure for 2Y, it also implies a phased integration approach, potentially pushing out cost and operating synergies with a gradual extraction vs a conventional acquisition. Hence, we believe execution, rather than strategic fit alone, will remain the primary driver of the stock’s near-term performance.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

.jpg)

2.jpg)