Commodity Daily Insights 01 July 2026 By - HDFC Securities Ltd

GLOBAL MARKET ROUND UP

Gold prices steadied around the $4,000 mark on Wednesday but remained close to their lowest level in nearly eight months as resilient U.S. economic data reinforced expectations that the Federal Reserve will keep monetary policy restrictive. The latest JOLTS report showed job openings climbed to a two-year high, highlighting continued strength in the labor market ahead of this week's closely watched U.S. nonfarm payrolls report.

The U.S. dollar also regained momentum, with the Dollar Index rising to around 101.3 after briefly easing earlier in the week. Markets continue to price in at least one Federal Reserve rate hike this year, with September seen as the most likely timing. A stronger dollar and higher interest-rate expectations continued to weigh on demand for non-yielding assets such as gold and silver.

Meanwhile, market remained focused on the ongoing U.S.–Iran peace talks in Qatar. Although hopes for a lasting ceasefire continue to support broader market sentiment, the absence of direct negotiations between the two sides has kept geopolitical uncertainty elevated, limiting any meaningful recovery in precious metals.

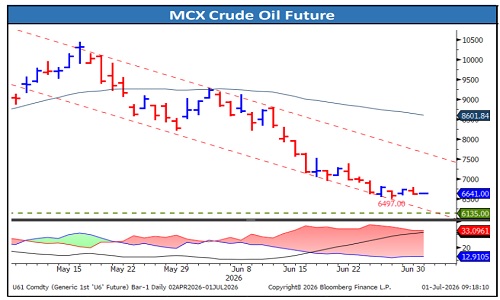

Crude oil prices traded with modest gain on Wednesday after posting their steepest quarterly decline since 2020, as investors monitored ongoing U.S.–Iran peace talks in Doha for further progress toward easing tensions in the Middle East. The recovery in tanker traffic through the Strait of Hormuz has also helped improve the global supply outlook following the recent ceasefire.

Adding to the bearish sentiment are growing concerns over a potential supply glut. Iran said it has exported more than 40 million barrels of crude since the U.S. lifted its naval blockade, while Russian exports have climbed to record levels, contributing to a build-up of oil held in floating storage. The prospect of rising global supplies continues to outweigh geopolitical risks, keeping pressure on crude oil prices.

Copper prices remained under pressure in early Asian trading as investors adopted a cautious stance ahead of the U.S. Commerce Department's report on the domestic copper market. The findings are expected to provide greater clarity on the potential imposition of tariffs on refined copper imports, a move that could significantly reshape global trade flows and pricing.

Gold

• Trading Range: 138780 to 144450

• Intraday Trading Strategy: Sell Gold Mini Aug Fut at 141775-141780 SL 142480 Target 140580/140050

Silver

• Trading Range: 219150 to 233700

• Intraday Trading Strategy: Sell Silver Mini Aug Fut at 229900-229925 SL 233700 Target 227050/224450

Crude Oil

• Trading Range: 6550 to 6780

• Intraday Trading Strategy: Sell Crude Oil Jul Fut at 6700-6705 SL 6819 Target 6600/6550

Natural Gas

• Trading Range: 297 to 324

• Intraday Trading Strategy: Buy Natural Gas Jul Fut at 305-305.5 SL 299.8 Target 312/315

Copper

• Trading Range: 1245 to 1280

• Intraday Trading Strategy: Sell Copper Jul Fut at 1264-1265 SL 1271 Target 1257/1250

Zinc

• Trading Range: 356 to 372

• Intraday Trading Strategy: Buy Zinc Jul Fut at 361.0- 361.5 SL 357.8 Target 365.50/367.8

Please refer disclaimer at https://www.hdfcsec.com/article/disclaimer-1795

SEBI Registration number is INZ00017133

.jpg)