Buy ITC Hotels Ltd for Target Rs. 190 by Choice Institutional Equities

Luxury Positioning and Accelerated Signings Drives Pipeline Visibility

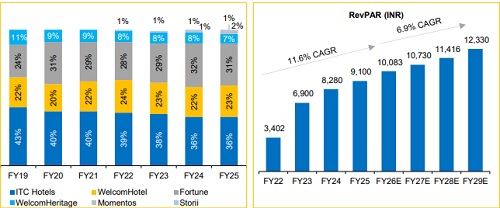

By FY30E, ITCHOTEL is set to scale up a pipeline of over 6,100 keys across luxury, upper-upscale and experiential formats. Flagship properties continue to anchor elevated RevPAR, while the chain’s increased signings in the last few years strengthens visibility of its upcoming pipeline. With owned assets maturing and strong key pipeline, 46% of which are in the upperupscale segment, the portfolio mix is structurally shifting towards higheryielding formats. Accordingly, we expect ITCHOTEL to scale up its portfolio by over 400 owned keys and more than 3,700 managed keys by FY29E.

Established Brand Equity and Prop-tech to Enable Managed Scalability

ITCHOTEL’s multi-brand architecture covers luxury, upper-upscale and midmarket formats, anchoring its presence with over 150 hotels and over 90 destinations. This diversified domestic platform is reinforced by the Marriott alliance and Club ITC, supporting higher ARRs, improved international mix and loyalty-led utilisation. Complementing these structural advantages, proprietary cloud-based Platform-as-a-Service (PaaS) enables lower-cost onboarding of managed hotels, reducing setup cost by ~50% and accelerating asset-light expansion. As a result, managed keys are expected to increase to 66.8% of ITCHOTEL’s total keys by FY29E, driving scalable network expansion and supporting revenue growth at 11.6% CAGR over FY26E–FY29E

Diversified Revenue Streams Poised for Margin Enhancement

ITCHOTEL is strengthening a capital-light growth engine, as managed keys are expected to scale up, from 60% to ~66.8% by FY29E, supporting a targeted 2.5x rise in management fees. A robust F&B platform, contributing 40% of total revenue in FY25, continues to deliver premium throughput through iconic dining brands and strong banqueting momentum. Adjacent revenue streams add further depth, to the topline, with memberships and experiential offerings set to grow 3x over the next five years, complemented by integrated developments, such as Sapphire Residences. We expect this integrated model to drive a 230 bps margin expansion over FY26E–FY29E.

View and Valuation: We initiate coverage on ITCHOTEL with a ‘BUY’ rating and a target price of INR 190, based on FY28E EV/Adj. Hospitality EBITDA of 20x, implying an upside of 28.9%. Driven by premium portfolio positioning, rising contribution from asset-light managed hotels and a visible pipeline, we expect Hospitality Revenue / Adj. hospitality EBITDA / PAT to expand at CAGRs of 11.1% / 13.7% / 16.3% respectively, over FY26E–29E. Rising managed mix and heightened operating leverage from maturing assets is likely to support margin expansion and compounding of sustained earnings.

Key Risks: Revenue concentration in hotels in metros, exposure to macro, seasonal and cyclical volatility. Heightened geopolitical tensions could discourage FTAs resulting in RevPar and occupancy declines.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)