Buy Indian Bank Ltd for the Target Rs.750 by Motilal Oswal Financial Services Ltd

Steady quarter; lower provisions aid earnings

Asset quality ratio improves

* Indian Bank (INBK) reported 1QFY26 PAT of INR29.7b (up 23.7% YoY/flat QoQ, 5% beat), driven by lower provisions.

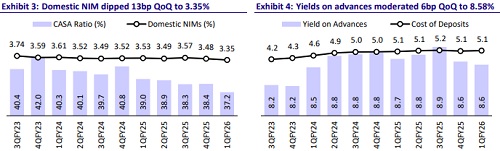

* NII was up 2.9% YoY/flat QoQ at INR63.6b (inline). NIM dipped 14bp QoQ to 3.23%.

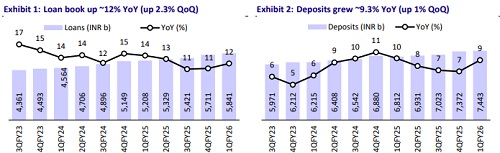

* Net advances grew 12% YoY/2.3% QoQ, while deposits grew 9.3% YoY/1.0% QoQ. Consequently, the C/D ratio increased 100bp QoQ to 78.5%. CASA ratio moderated to 37.2%, with domestic CASA ratio at 39%.

* Fresh slippages improved to INR13.7b vs. INR14.3b in 4QFY25. GNPA/NNPA ratios continued to improve by 8bp/1bp QoQ to 3.01%/0.18%. PCR stood at 94.3%.

* We increase our earnings estimates by 6%/4% for FY26/FY27 and anticipate the bank to deliver FY27E RoA/RoE of 1.29%/16.9%. Reiterate BUY with a TP of INR750 (premised on 1.2x FY27E BV).

Credit growth guidance maintained at 10-12% ; NIM moderated 14bp QoQ

* INBK’s reported 1QFY26 PAT of INR29.7b (23.7% YoY/ flat QoQ, 5% beat), driven by lower provisions.

* NII was up 2.9% YoY/flat QoQ at INR63.6b (in line). NIM dipped 14bp QoQ to 3.23% during the quarter. The bank continues to guide for FY26 NIMs in the range of ~3.15%-3.30%.

* Other income grew 28% YoY (down 11% QoQ) to INR24.4b (in line), resulting in 9% YoY growth (3.7% QoQ drop) in total revenue (in line). Treasury income stood at INR3.8b vs. INR1.9b in 4QFY25.

* Opex grew 12.4% YoY (down 2.1% QoQ, 4% above est.). As a result, C/I ratio slightly increased to 45.8% from 45% in 4QFY25. PPoP grew ~6% YoY (down 4.9% QoQ) to INR47.7b (6% miss).

* Advances grew 12.1% YoY/2.3% QoQ to ~INR5.8t, led by retail and agri. Retail loans grew 16.6% YoY/3.8% QoQ. Within retail, housing grew 2.3% QoQ and VF rose 7.3% QoQ. Agri advances grew 4.7% QoQ.

* Deposits grew 9.3% YoY (1% QoQ), with CASA ratio moderating 114bp QoQ to 37.2% and domestic CASA ratio standing at 39%. C/D ratio increased by 100bp QoQ to 78.5%.

* Fresh slippages improved to INR13.7b vs. INR14.3b in 4QFY25. GNPA/NNPA ratios continued to improve by 8bp/1bp QoQ to 3.01%/0.18%. PCR stood at 94.3%.

* SMA-2 book rose to INR45.9b due to two large PSU accounts, which the bank did not expect to slip. The restructured portfolio fell to INR45.6b or 0.78% of loans (vs. 0.85% in 4QFY25).

Highlights from the management commentary

* FY26 guidance: Deposit growth guidance is maintained at ~8-10%. GNPA ratio is expected to be below 3% (likely 2.5%). The bank plans to open 119 branches in FY26.

* The quantum of margin decline will reduce from 2Q onward as bulk deposits will also start repricing and retail term deposits and SA deposits will also reprice.

* MCLR book is 52%, out of which one year linked is 41%. On 40% of book which is EBLR linked, rate cut impact has already been passed on.

Valuation and view

INBK reported healthy earnings, as provisions were significantly lower than expected. However, margins contracted 14bp QoQ and are expected to moderate further due to rate cuts. Advances growth was higher than deposit growth; hence, the CD ratio inched up. Management expects margins to be in the range of 3.15- 3.3%, while the growth outlook remains healthy. The bank guides for a healthy asset quality outlook. The asset quality ratio improved, with INBK maintaining the best-inclass coverage ratio and lower slippages, which provides comfort on incremental credit costs. SMA-2 has seen an increase; however, the bank does not anticipate any slippages from these accounts. We increase our earnings estimates by 6%/4% for FY26/FY27 and anticipate the bank to deliver FY27E RoA/RoE of 1.29%/16.9%. Reiterate BUY with a TP of INR750 (premised on 1.2x FY27E BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412