Buy Home First Finance Company India Ltd for the Target Rs.1,375 by PL Capital

Backing the Talos^ of affordable housing

We initiate coverage on Home First Finance Company (HOMEFIRS) with ‘BUY’ rating and TP of Rs1,375 at 2.6x FY28E P/ABV. HOMEFIRS has demonstrated robust AUM growth of 29% CAGR over FY20-25. We expect the trajectory to continue and AUM to grow by ~24% CAGR over FY25-28E aided by deeper geographic expansion in existing and new markets. Investments in technology, connector model of sourcing, and centralized control over underwriting underpin scalability of the business model and justify a premium over peers. Despite rising competition and higher BT-outs, HOMEFIRS has been able to maintain steady yields. We expect spreads to remain in the guided range of 5.0%-5.2%. While credit cost has been elevated (40bps in Q3FY26) due to challenges in the MFI/ MSME segment, we expect it to normalize in FY27/ FY28E. The stock has seen significant correction (trading below -1 SD). Our valuation at 2.6x FY28E P/ABV accounts for a 20% discount from 5-year average (3.3x). Initiate with ‘BUY’

* Diversification to drive growth: HOMEFIRS has consistently delivered robust AUM growth (29% CAGR over FY20-25). Long runway in affordable housing finance, rapid geographical expansion, and lean operating model are key growth drivers. Incremental growth will be driven by newer geographies as well as deeper presence in existing locations. Gradual portfolio diversification beyond Tier 1/2 cities and focus on Rs1mn+ ticket sizes/ co-lending and LAP are likely to augment growth, leading to AUM CAGR of ~24% over FY25-28E.

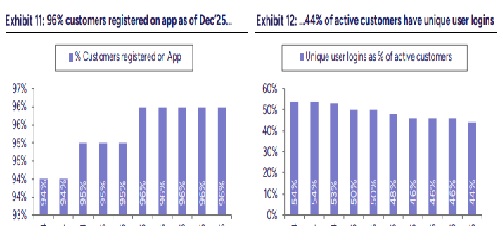

* Distribution-light model paying off: HOMEFIRS’s centralized model of underwriting, leveraging data-analytics, cheque bounce prediction models, and ML tools, has led to higher efficiency compared to peers (credit underwriting TAT of ~48 hours). Moreover, the connector-based sourcing model (~77% of leads), with opening of satellite/virtual branches first, highlights scalability in operations. These place HOMEFIRS in a better position vs. peers to tap new geographies quickly

* Higher BT-outs and credit cost are near-term challenges: While BT-outs have seen a spike (6.6%/ 7.6% in 3QFY26/ 2QFY26), HOMEFIRS has been able to maintain a healthy origination yield (13%+ over the last 2 years). Moreover, it has the potential to increase LAP share to 30% (vs. 16% currently), supporting yields. We expect spreads to remain in the guided range (5.0%- 5.2%) as cost of borrowing moderates. Asset quality metrics have been weak in 9MFY26 due to stress in the MFI/ export-oriented segments, and we have accounted for higher credit cost (average of ~34bps over FY26-28E) in our valuation.

* Valuation attractive; initiate on ‘BUY’: Affordable housing players have seen a sharp de-rating over the past year due to slower growth and asset quality challenges. However, HOMEFIRS’s unique technology-focused model, lean operations and strong execution capability grant a premium valuation vs. peers (FY28E P/ABV of 2.3x vs. 1.6x for AAVAS). While near-term RoE is suppressed due to recent capital raise (QIP of Rs12.5bn in Apr’25) and high capital adequacy (48.6% Tier 1 ratio), we expect it to expand to ~14% by FY28E with RoA of 3.5% (earnings CAGR of 24% over FY25-28E). We initiate with ‘BUY’ and TP of Rs1,375 (2.6x FY28E P/ABV).

Company Overview

HOMEFIRS: Tech-driven, connector-led affordable housing lender

Founded in 2010, Home First Finance Company (HOMEFIRS) is a non-deposit taking housing finance company (HFC) focused on lending to home buyers belonging to salaried and self-employed segments with income less than Rs50k per month. As of Dec’25, the company had an AUM of Rs149.2bn, 83% of which comprised pure housing loans, 16% LAP and 1% commercial/shop loans. It is majorly a technology-driven lender with end-to-end loan processing handled digitally.

Underwriting model - Key features

* Focused on high-velocity markets: HOMEFIRS analyzes loan origination data from Credit Information Bureau/ Experian to identify high-velocity pin codes, districts and markets in India. It also uses data on 2W/car purchases and fastfood retail outlets as proxies for income to decide where to set up a branch.

* Ground study through connectors: Once the company has identified highvelocity areas, it conducts a ground study with connectors in the areas. The main purpose is to analyze customer behavior in terms of ticket sizes, sensitivity to pricing, delinquency trends, etc. Sometimes, HOMEFIRS sets up a satellite branch with a relationship manager (RM) from a nearby branch to disburse loans along with the help of connectors in the region. Once this satellite arm reaches a threshold of Rs100mn in AUM, the company invests in a physical branch. This process usually takes 9-12 months.

* Using connectors to generate leads: Once a branch has been set up, RMs from the branch depend largely on connectors to source leads. Connectors can be of various types and include (1) builders, (2) financial connectors ( chartered accountants, lawyers, real-estate brokers, insurance agents), (3) construction connectors (masons, plumbers, cement dealers, hardware store owners) and (4) micro-connectors (kirana store owners).

* Field check by RMs: Once the lead has been sourced, the RM collects all the basic information from the customer (PAN card, Aadhaar card, e-KYC). The RM then conducts a field check by visiting the home/ workplace of the customer to cross-verify documents of identity, property/asset/vehicle ownership, etc. They also take photos/videos of the property/asset as proof along with documents such as GST, LPG and utility bills. All this data helps in creating a detailed profile of the customer to present to the central credit underwriting team

* Comprehensive credit underwriting: The centralized credit team evaluates all the documents such as KYC details, CIBIL score, bank statements, salary slips, asset ownership/insurance documents, and other bills to assess the borrower’s income generation capacity. The credit algorithm used by the team has access to 100+ data points of the customer provided by third-party vendors (including account aggregator data from banks, Hunter, Perfios, etc.). Based on this, the credit underwriting team decides whether to lend to the customer and applies a risk-based pricing mechanism (depending on the customer profile, type of loan) to arrive at interest rate, ticket size and LTV. This function of credit underwriting team typically takes ~48 hours.

* Technical valuation and legal verification: Once the credit underwriting team has given approval, the technical and legal teams assess the property while reviewing all the legal documents. HOMEFIRS has outsourced this function to an outside vendor

* Strong collections mechanism: RMs at branches are responsible for collections with ~50% of their incentives linked to collection activity.

Above views are of the author and not of the website kindly read disclaimer