2025-10-16 02:32:49 pm | Source: Motilal Oswal Financial Services ltd

Buy HDFC Life Insurance Ltd for the Target Rs. 910 by Motilal Oswal Financial Services Ltd

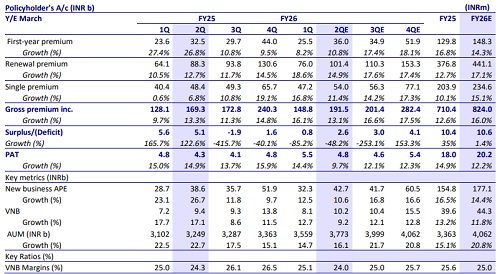

* APE growth is expected to remain in double digits YoY.

* On a YoY basis, VNB margin is expected to dip, led by a loss in GST input credit on policies.

* Product mix likely to tilt towards traditional products over ULIPs.

* The share of HDFC Bank in the distribution mix and the outlook ahead will be critical monitorables.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Buy Cyient Ltd for the Target Rs 830 by Motilal Oswa...

The Art of Slow Living: Why Slowing Down Can Improve...

Government institutes framework to strengthen cybers...

Over 77 lakh annual FASTag passes issued, register 6...

Quote on Technical Market Commentary for July 22nd, ...

Maruti Suzuki India to hike car prices by up to Rs 3...

Buy Mahindra Logistics Ltd For Target Rs. 507 by Pr...

Women's Short and Stylish Kurti: The Perfect Blend o...

Resistance : 24150 (Pivot Level) and 24300 (Key Resi...

Economic activity posted strong expansion in June 20...

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...

Financials Banking Sector Update : Are there upside risks to FY27E credit growth by Motilal Oswal Financial Services Ltd

Consumer Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd

Automobiles Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd