Buy HDFC Bank Limited for Target Rs. 1,173 by Religare Broking Ltd

Healthy Profitability Driven by Lower Credit Costs: HDFC Bank delivered a steady Q4 FY26 performance with a Profit After Tax (PAT) of ?19,221 crore, representing a growth of 9.1% YoY and 3.1% QoQ. Net interest income (NII) grew 3.2% YoY to ?33,081 crore, while non-interest income saw a robust 9.7% YoY increase to ?13,200 crore, supported by a 7.4% rise in fee income. Profitability was primarily bolstered by lower-than-expected provisions, which declined 18.2% YoY and 8.1% QoQ. The bank maintained stable return metrics for the quarter, with a Return on Assets (RoA) of 1.96% and a Return on Equity (RoE) of 14.1%. Management emphasized that their primary focus remains on RoA and consistent EPS growth.

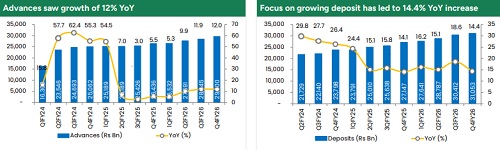

Loan Growth Gains Momentum, Led by Corporate & MSME: Gross advances rose 12.0% YoY to ?29.6 trillion, accelerating from the 5.4% growth seen in the previous year. Growth was notably strong in Business Banking (+20.0% YoY) and Small and Mid-market segments (+17.2% YoY). Corporate and wholesale loans grew by 13.0% YoY, while retail loans grew by a more moderate 6.5% YoY. Management expressed confidence in this improving trajectory, noting that retail growth—particularly in mortgages and wheels—is expected to pick up further as they leverage their expanded distribution of 9,689 branches.

Strong Deposit Accretion & Improving Granularity: The bank reported exceptional deposit growth, with total End-of-Period (EOP) deposits rising 14.4% YoY to ?31.1 trillion. Accretion was particularly strong in the final month of the quarter, driven by a surge in system liquidity. Crucially, the bank is successfully shifting toward a more sustainable and granular funding base; less than ?3 crore retail deposits accounted for 47% of net incremental accretion in FY26, up from 31% in FY25. CASA deposits grew 12.3% YoY, maintaining a 34.1% share of total deposits, while the Credit-toDeposit (LDR) ratio improved significantly to 94.6% from 98.7% in the previous quarter

Margins Stabilizing with Residual Repricing Benefits: Net Interest Margin (NIM) stood at 3.38% for the quarter. While the transmission of rate cuts has been faster on asset yields, management noted that cost of funds declined by 10 bps QoQ. With average deposit tenures between 1.2 to 1.5 years, the bank expects residual repricing benefits of time deposits to flow through in the coming quarters, providing a tailwind for NIM stability. Management remains committed to a range-bound NIM strategy, focusing on overall returns rather than margin expansion alone.

Robust Asset Quality and Provisioning Buffers: Asset quality continues to be a key strength, with the Gross NPA ratio improving to 1.15% (vs. 1.24% in Q3) and Net NPA at 0.38%. Excluding agricultural NPAs, the GNPA ratio was even lower at 0.91%. The Slippage ratio declined sharply to 0.95% from 1.37% sequentially. HDFC Bank maintains a conservative stance with a Provision Coverage Ratio (PCR) of 67% and a total capital adequacy ratio of 19.7%, well above regulatory requirements.

Valuation and Outlook: HDFC Bank’s Q4 FY26 performance demonstrates resilient earnings momentum, underpinned by accelerating loan growth, exceptional deposit mobilization, and superior asset quality. The bank’s successful pivot toward a more granular and sustainable funding base, combined with expected residual repricing benefits from its ?20.5 trillion time deposit book, provides strong visibility for margin stability and medium-term profitability. Management’s strategic focus on Return on Assets (RoA) and consistent EPS growth, supported by an expansive network of 9,689 branches and industry-leading technology investments, positions the bank to grow faster than the system from FY27 onwards. Furthermore, the ongoing realization of merger synergies—evidenced by the bank now holding liability relationships for 50% of its mortgage customers—enhances its cross-selling funnel and long-term operating leverage. We maintain a BUY rating with a target price of ?1,173, valuing the Standalone bank at 2.2x FY28E adjusted book value.

Please refer disclaimer at https://www.religareonline.com/disclaimer

SEBI Registration number is INZ00017433