Buy Greenply Industries Ltd for Target Rs. 355 by Choice Institutional Equities

Impressive Volume Growth Ahead MTLM outlined a constructive FY27 outlook, continues to see healthy volume growth across Plywood and MDF. Guiding for higher leverage in the near term to support expansion while maintaining a stable long-term balance sheet. Core plywood demand remains subdued, though supported by continued market share gains from organised players, while MDF continues to outperform with robust industry growth and stronger margin/volume guidance. New growth drivers such as PVC doors/windows and the furniture hardware JV remain in scale-up mode, with profitability expected to improve over the medium term as utilisation ramps up and domestic manufacturing expands.

We continue to have a positive stance on MTLM owing to: 1) Expected volume/realisation CAGR of 9.5/2.0%, respectively, over FY26–29E for the Plywood segment (which exceeds industry growth forecast of ~7% CAGR over the same period) driven by market share gains from unorganised players, 2) 20.0/3.0% volume/realisation, respectively, CAGR in MDF segment over FY26–29E and 3) Revenue contribution from the new JV, BV Samet, from FY27.

Valuation: We maintain our BUY rating on MTLM with a revised TP of INR 355/share (unchanged), we higher EBITDA/PAT growth by 4.1/1.2% for FY27E and 3.9/(-1.1)% for FY28E. We value MTLM on our PEG ratio-based framework – we assign a PEG ratio of 1x on FY26–29E core EPS growth of 32.1%, which we believe is a conservative multiple. This valuation framework gives us the flexibility to assign a commensurate valuation multiple based on quantifiable earnings growth.

Risks: Potential slowdown in real estate and home improvement activities and possible higher timber cost are risks to our BUY rating.

Q4FY26: Plywood & MDF segments deliver strong performance, offset by continued losses at Furniture Hardware JV (Greenply Samet)

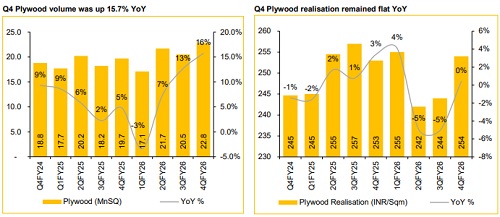

* Plywood Segment: Q4FY26 volume came in at 28.8 Mn SQM up +15.7/11.2% YoY/QoQ vs Choice Institutional Equities (CIE) estimate of 22.0 Mn SQM. Realisation at INR 254/SQM is up 0.4/4.1% YoY/QoQ vs CIE estimate of INR 244/SQM. As a result, revenue grew by 14.7/12.8% YoY/QoQ to INR 5,885 Mn (including other related products revenue of INR 103 Mn) vs CIE estimate of INR 5,368 Mn. EBITDA margin came in at 10.4% (+120/200 bps YoY/QoQ), which is higher than CIE estimate of 9.0%. Overall, Plywood segment performance was stronger than expected, owing to higher volumes and better margin in this quarter.

* MDF Segment: Q4FY26 volume came in at 62,021 CBM (+45.3/28.2% YoY/QoQ) vs CIE estimate of 52,000 CBM, which is encouraging. Realisation came in at INR 30,506/CBM, down 4.0/2.9% YoY/QoQ vs CIE estimate INR 31,500/CBM. Revenue came in at INR 1,892 Mn (+39.5/24.5% YoY/QoQ, respectively) vs CIE estimate of INR 1,638 Mn. EBITDA margin came in at 17.0%, up 200/690 bps YoY/QoQ vs CIE estimate of 12.0%.

* Overall, Q4FY26 revenue up by 19.6/15.3% YoY/QoQ to INR 7,762 Mn vs CIE estimate of INR 7,306 Mn. EBITDA grew by 37.0/58.3% YoY/QoQ, respectively, to INR 932 Mn. EBITDA margin was up 152/326 bps YoY/QoQ to 12.0% vs CIE estimate of 9.4%.

* PAT was adversely impacted by exceptional items amounting to INR 151.6 Mn, comprising INR 94.8 Mn towards provision for financial liability in GMEL, INR 27.0 Mn as provision for diminution in the value of investment relating to its 19% stake in GMEL, and INR 29.8 Mn recognised as loss allowance against advances paid

* On Annual Basis, consolidated revenue up 10.1% YoY to INR 27,390 Mn in FY26. At the same time, core EBITDA increased by 13.8% YoY to INR 2,705 MN with EBITDA margin of 9.9% (vs 9.6% in FY25)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131