Buy Godrej Consumer Products Ltd For Target Rs. 1,400 By Emkay Global Financial Services Ltd

We maintain our positive stance on GCPL, with BUY and Sep-26E TP of Rs1,400, on 50x P/E. We believe the company will continue to enhance execution with focus not only on warding off category and macro hiccups, but also expanding into high-growth segments. Near term performance is likely to have a bearing of lower-than-expected margin in 2HFY26 and macro pressures in Indonesia. We retain 10% revenue/19% earnings CAGR for FY26-28E. GCPL has announced its organic foray into the toilet-cleaner category (sized Rs30bn), and inorganic entry into the male face-wash segment(sized Rs10bn) with acquisition of the Muuchstac brand (at EV/sales of 4x/EV/EBITDA of 10x on trailing 12M sales of Rs800mn and adj EBITDA of Rs320mn). Q2 results were a mild miss on estimates, with consol revenue growing 4% and earnings declining ~2%.

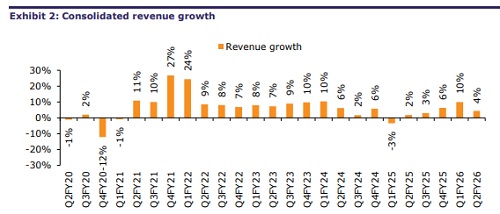

Strategy in place for accelerating topline delivery; Q2 growth soft at 4%

GCPL’s consol revenue grew 4.3%, with India revenue growth at ~4%. Its India branded portfolio grew 2%, with 3% volume growth. Home-care saw 6% revenue growth, affected by weak seasonality in household insecticides (market-share gains sustained). The personal-care segment saw 2% revenue decline, affected by the GST-related transition. Overall, the management noted a 3-4% revenue impact in Q2 due to GST-related trade destocking, which is likely to be recovered in Q3. The mgmt expects a high single-digit volume growth in Q3. Internationally, its Indonesia business saw a sales decline of 7%, of which 4% is attributed to changes in distribution arrangement (impact is likely to continue for the next 3 quarters). Pricing impact in Indonesia due to BTL activation is likely to come off in the next 1-2 quarters. GAUM clusters saw 25% growth with ~15% constant currency (CC) growth. The mgmt sees a high single-digit CC growth ahead.

Q2 earnings declined 2%; margin recovery to aid double-digit earnings ahead

Consolidated EBITDA margin stood at ~19.2%, contracting by 155bps YoY. GCPL’s India business margin stood at 21.7%, down by 260bps YoY. The management noted margin recovery from Q3, and expects 2H margins to track in the 24-26% band. We now estimate margin of 24.5% for 2HFY26E on a conservative basis. Compared to the ~7% EBITDA decline in 1HFY26, we see 17% growth in 2HFY26E (on a low base of a 15% decline in 2HFY25). International margin held firm YoY at 14.7%, aiding EBITDA growth of 7%. Indonesia margin YoY was flat at 19.4%. GAUM cluster margin was ~14% in Q2FY26, contracting by 50bps YoY; the management gave guidance for mid-teens margins ahead. The management has guided for double-digit EBITDA growth in India and GAUM for FY26, while we build in growth of 5% and 24%, respectively.

Focus on execution addressing consumer needs; maintain BUY

We continue to see relatively better execution, where the company continues to enhance its portfolio width with category additions. As the company diversifies and adds new pillars of growth, we expect macro driven volatility in performance to ease ahead. Margin recovery ahead is likely to aid in earnings acceleration. It’s one year forward P/E at 45x is now near its historical five-year average of 44.5x.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354