Buy Eternal Ltd for the Target Rs.360 by Motilal Oswal Financial Services Ltd

Bracing for a dogfight Expect high volatility in short term as competition heats up

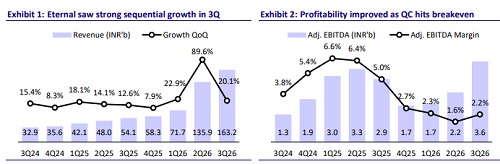

* Eternal reported 3QFY26 net revenue of INR163b, up 20.7% QoQ, above our estimate of 11.8% QoQ growth.

* Food delivery (FD) NOV came in at INR98.4b, above our est. of INR94.2b. Blinkit NOV came in at INR133b (up 120% YoY) vs. our est. of INR133.6b. For FD, adjusted EBITDA as a % of NOV margin was up 10bp QoQ at 5.4% vs. our estimate of 5.3%.

* Blinkit reported a contribution margin of 5.5% (4.6% in 2Q). Adj. EBITDA margin was at breakeven, above our expectation of -1.3%.

* Mr. Albinder Dhindsa, the current CEO of Blinkit, is set to become CEO of Eternal, effective 1st Feb’26, replacing Mr. Deepinder Goyal, who will continue to remain on the board.

* Our TP of INR360 implies a 27% upside from current levels. While FD growth is recovering, the pace of normalization remains gradual, and we expect the EBITDA respite in Blinkit to be short-lived as competitive intensity in quick commerce (QC) re-accelerates. We reiterate our BUY rating, supported by Eternal’s market leadership in both QC and FD and the long-term optionality in Blinkit as a generational opportunity in grocery and retail disruption. However, potential elevated discounting/investments in both QC and the going-out business are anticipated to constrain profitability in the short term.

Our view: EBITDA respite short-lived, more pain ahead

* EBITDA breakeven in Blinkit, but expect another period of competitive intensity: Blinkit achieved EBITDA breakeven on the back of a better assortment mix and supply chain efficiencies. However, we expect some volatility and no meaningful improvement in metrics in the near term, as competitive intensity heats up.

* Bracing for a dogfight: We note that our view (see our note dated 3rd Nov’25: Eternal & Swiggy: Deja Vu) of lower competitive intensity and cost focus in the industry has not played out. Contrary to earlier expectations, the risk is that the market leader could be drawn into a dogfight too, with lower minimum order values and higher discounts. We also note that Eternal has stopped reporting GOV and has moved to NOV reporting, which means that going forward we will not be able to ascertain the extent of discounting at Blinkit; this could point to slightly higher discounting intensity. We believe this will delay the path to profitability for Blinkit. As a result, we reduce our adjusted EBITDA assumptions by ~15% for FY27/28E, and accordingly lower our TP to INR360 (INR420 earlier)

* Other businesses: Hyperpure turns profitable; Going-out in investment phase: In our view, Hyperpure turning adj. EBITDA positive is encouraging. While still smaller within Eternal, management sees a path to ~USD1b in revenue with 4- 5% margins over the next three years, alongside ecosystem benefits across FD and Blinkit by helping restaurants run leaner and improving sourcing economics. That said, we believe Going-out business remains in an investment phase with high losses due to upfront investment in live IPs and District Pass. Management expects losses to narrow sequentially; accordingly, we have built in ~INR1,000m loss in 4Q (vs. INR1,210m loss in 3Q), with breakeven targeted in the next 4-6 quarters.

* FD growth recovering: FD growth continued its steady recovery, with NOV growing 16.6% YoY, driven by a modestly improving demand environment that led to higher-than-expected order volumes, a reduction in MOV for free delivery on Gold orders, and strong MTC additions during the quarter. Management expects growth to gradually trend toward ~20% YoY as market share gains continue. We have built in a gradual convergence, with NOV growth of 15.3%/18.0%/18.7% in FY26/27/28E.

* Leadership transition introduces some uncertainty: The CEO transition appears orderly, but the division of responsibilities between management and the board remains unclear as of now. While we believe day-to-day execution is unlikely to be disrupted, the change does introduce some uncertainty to the business.

Valuation and changes to our estimates

* Eternal’s FD business is stable, and Blinkit offers a generational opportunity to participate in the disruption of industries such as retail, grocery, and ecommerce. We reduce our FY27/FY28 estimates by ~15%, factoring in intense competition, continued dark store expansion, and branding and marketing investments in QC. Eternal should report a PAT margin of 1.6%/2.0% in FY27/28E. Our TP of INR360 implies a 27% upside from the current level. We reiterate our BUY rating on the stock.

Blinkit hits EBITDA breakeven ahead of Street estimates

* 3Q net revenue was INR163b, up 20.7% QoQ vs. our estimate of +11.8% QoQ.

* FD NOV came in at INR98.4b, above our estimate of INR94.2b. Blinkit NOV came in at INR133b (up 120% YoY) vs. our estimate of INR133.6b.

* FD adj. EBITDA as % of NOV margin was up 10bp QoQ at 5.4% (vs. est. 5.5%).

* Blinkit reported contribution margin of 5.5% (4.6% in 2Q). Adj. EBITDA margin is at breakeven, above our expectation of -1.3%.

* FD revenue grew 8% QoQ/29% YoY (est. 19% YoY) and contribution margin was flat QoQ at 10.4%.

* Consol. reported EBITDA came in at INR3,680m (2.3% reported EBITDA margin vs. 1.8% in 2Q).

* PAT stood at INR1020m, up 72% YoY (est. INR841m).

Key highlights from the management commentary

* FD: YoY growth is expected to gradually inch toward ~20% over time. Growth was driven by three key factors: 1) A modest improvement in the demand environment, particularly in the second half of the quarter, leading to higher app engagement and higher-than-expected order volume; 2) Full-quarter impact of the reduction in minimum order value for free delivery on gold orders (to INR99 from INR199), which increased ordering frequency among more budgetconscious customers; 3) Continued investments in customer activation across cohorts, reflected in 21% YoY growth in average MTC during the quarter.

* Blinkit: The business continues to grow at a robust pace, and the ceiling of the QC market in India is not yet visible. Mature cities such as Delhi NCR are still growing at ~55% YoY. The next seven metros are growing at over 100% YoY. Current guidance of 3,000 stores by Mar’27 assumes continued irrational competitive intensity. If competition moderates, the company would aim for 3,500-4,000 stores by Mar’27, supporting NOV growth of over 100% YoY.

* Competitive intensity increased during the last quarter as several competitors moved to zero minimum order values and zero delivery fees, alongside increased discounting across the market.

* 211 net new stores were added during the quarter, taking the total store count to 2,027, about 70 stores short of the guidance of 2,100.

* Capex per store is expected to increase due to warehousing infrastructure expansion, increased automation, and marginally larger store sizes. This is expected to drive higher productivity per store. Net working capital is expected to remain below 18 days, with RoCE outcomes north of 40%

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041