Buy ICICI Lombard Ltd for the Target Rs.2,260 by Motilal Oswal Financial Services Ltd

NEP miss and one-off drive combined ratio and PAT miss

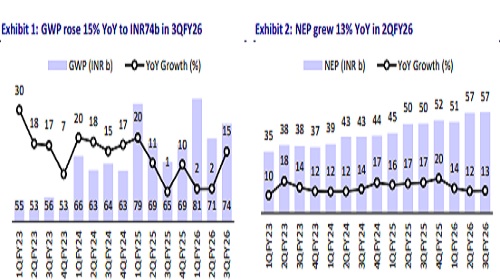

* ICICI Lombard’s (ICICIGI) gross written premium grew 15% YoY in 3QFY26 to INR74.3b (in-line). NEP grew 13% YoY to INR56.9b, (5% miss). For 9MFY26, it grew 13% YoY to INR165b.

* Claims ratio stood at 68.7% (vs our est. of 67.4%) vs 65.8% in 3QFY25. Commission ratio came in at 22.5% vs 22.9% in 3QFY25 (vs. our expectation of 21%) and opex ratio came in at 13.3% vs. 14% in 3QFY25 (vs. our expectation of 13.2%).

* Combined ratio came in at 104.5% (vs our expectation of 101.6%), compared to 102.7% in 3QFY25. Excluding 1/n and new wage code impact of INR0.55b, combined ratio was at 102.2% in 3QFY26.

* PAT at INR6.6b declined 9% YoY (23% miss). For 9MFY26, PAT grew 11% YoY to INR15.7b. Excluding the impact of Wage Code and 1/n, PAT for 3QFY26 was INR7.2b, registering a growth of 6.3% YoY.

* Management highlighted strong underlying demand across both motor and health post GST changes and reiterated its medium-term intent to grow 100–200bp faster than the industry in FY27, while sustaining 18– 20% RoE.

* We have kept our premium estimates intact. However, we have raised the claims ratio for the motor segment considering the competitive intensity, leading to a 4% decline in our FY26/27/28 EPS. Reiterate BUY with a TP of INR2,260 (based on 28x FY28E EPS).

Strong fresh business growth in motor and health post GST cuts

* NEP growth of 13% YoY was driven by 10%/22% YoY growth in the motor/health (including PA) segments. The marine segment reported a YoY decline of 4%, while the fire segment witnessed a 5% YoY growth. The strong fresh business growth in motor and health post GST reductions resulted in higher URR creation and a 5% NEP miss. Hence, claims ratio came in 130bp above our estimates, while absolute claims were largely in line with our estimates.

* Underwriting loss was at INR3.5b compared to a loss of INR1.5b in 3QFY25 vs MOFSLe of INR1b. This was largely owing to 7% higher commission expenses compared to our estimates, while opex was in line.

* Total investment income in policyholders’ account was in line with our estimates at INR9.2b; for shareholders’ account, it was 7% below our estimates at INR3.1b.

* Claims ratio at 68.7% rose 130bp YoY, with motor OD loss ratio rising 820bp YoY and motor TP rising 970bp YoY, while the health segment’s loss ratio improved 660bp YoY.

* Investment book grew 13% YoY to INR583b, reflecting a strong investment leverage of 3.6x. Absolute investment yield for 3QFY26 was at 2.1%, which was slightly lower YoY (2.15% in 3QFY25). The investment portfolio mix for 9MFY26 stood at 42.5%/ 34.3%/17.8% for corporate bonds/G-Sec/Equity (incl. Equity ETF).

* The impact on profitability due to higher URR creation and one-off wage code impact resulted in an RoE of 16.5% in 3QFY26 (21.5% in 3QFY25). Excluding the wage code impact, RoE was 17.5% for 3QFY26.

* Solvency ratio was at 2.69x (2.36x in 3QFY25).

Highlights from the management commentary

* The auto industry recorded a 19.5% YoY volume growth, the highest in the last 12 quarters, supported by festive demand and GST rationalization, which resulted in growth recovery for motor insurance. In health insurance, GST exemption improved affordability, driving strong uptake, particularly from firsttime buyers in Tier-2 and smaller cities.

* In 3QFY26, new business contributed 35% to motor premium, with new business growth at 12.4% YoY and renewals growing 7.4% YoY. After lagging renewals earlier in the year, new business momentum strengthened meaningfully in 3Q, supported by momentum in fresh vehicle sales.

* Retail health premium grew 86% YoY in 3QFY26, raising the retail health market share to 4.5%, supported by GST exemption, higher awareness, and strengthened distribution, including the opening up of the agency channel.

Valuation and view

* 3QFY26 witnessed the favorable impact of the recent GST exemption, making health insurance more affordable, while rate cuts in automobile boosted vehicle sales, leading to a recovery in motor insurance.

* The company's retail health segment continues its strong momentum, gaining market share through effective new customer acquisition, strong distribution capabilities, and significant traction of its "Elevate" product. Competitive intensity remains high in the motor OD segment, but the company maintains the top position.

* We have kept our premium estimates intact. However, we have raised the claims ratio for the motor segment considering the competitive intensity, leading to 4% decline in our FY26/27/28 EPS. Reiterate BUY with a TP of INR2,260 (based on 28x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412