Buy JSW Energy Ltd for the Target Rs.590 by Motilal Oswal Financial Services Ltd

Strong execution, lower merchant exposure key to sustaining momentum

We recently hosted a meeting with Mr. Sharad Mahendra, CEO & MD of JSW Energy (JSW), and key investors. Key takeaways from the meeting according to us are:

* Curtailment risk significantly de-risked: Management highlighted that over 80% of projects set for commissioning over the next two years are either state transmission utility (STU) connected or off-grid, significantly de-risking curtailment and execution.

* Lower merchant exposure to increase earnings visibility: Utkal (700MW thermal plant), which had 100% merchant exposure in FY26 and was impacted by weaker demand, will be largely contracted (400MW) from 1st April’26, reducing JSW’s overall merchant exposure to ~5% of operational capacity.

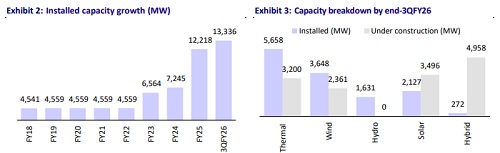

* RE capacity addition and connectivity mix: Installed capacity is expected to reach 14.5–15GW by FY26-end. The target is to add 6–7GW of RE capacity over FY27–FY28, with 3GW planned for FY27 and a higher run-rate in FY28. The planned additions include 2GW with STU connectivity in Maharashtra, ~800–900MW of group captive capacity in FY27, 800–900MW of off-grid capacity in FY28, and the remaining 2GW under CTU connectivity.

* Strong land and connectivity readiness: JSW has already secured ~80% of land and 100% of transmission connectivity for projects planned over the next two years. In addition, O2 Power has surplus transmission connectivity of ~1.7GW beyond contracted PPAs, offering meaningful optionality for future capacity tie-ups.

* Structural cost advantage vs industry: JSW enjoys a 10–15% cost advantage vs the industry, driven by lower wind turbine costs under a fixed-price partnership with SANY, lower solar plant costs aided by regulatory exemptions for PPA projects, and the use of imported modules for group captive installations.

* We have a BUY rating on JSW with a TP of INR590.

Earnings recovery amid merchant exposure reduction

* Utkal (700MW thermal plant), which had 100% merchant exposure in FY26 and was impacted by weaker demand, will be largely contracted (400MW) from 1st April’26, reducing JSW’s overall merchant exposure to ~5% of operational capacity.

* JSW expects a stronger operating and cash flow profile in 3QFY27 vs. 3QFY26, supported by Utkal (400MW) now being tied up and incremental solar capacity, offsetting the drag from ~5.8GW of hydro and wind underperformance.

* The company highlighted that Mytrah assets, given the older turbine technology, are operating at relatively lower PLFs. EBITDA expectations for Mytrah have been moderated to INR15–15.5b, compared to earlier assumptions of INR16.5b that had factored in carbon pricing.

* JSW reiterated its INR1.3t capex plan, encompassing RE, PSP, BESS, manufacturing, and thermal projects. Capex will be back-ended into FY27, with CWIP becoming a larger balance sheet component due to long-gestation projects. Funding is expected to be 75–80% debt, with equity front-loaded during CWIP stages.

Strong execution visibility: 80% land secured, 100% connectivity for next two years

* JSW reiterated its 30 GW installed capacity target by 2030, alongside a 40 GWh energy storage target, comprising 30 GWh of pumped storage projects (PSP) and 3 GWh of battery energy storage systems (BESS).

* Installed capacity is expected to reach 14.5–15 GW by FY26-end. 6–7 GW of RE capacity additions in FY27–FY28 (with ~3 GW targeted in FY27 and a higher runrate of additions in FY28), comprising ~2 GW with STU connectivity in Maharashtra, ~800–900 MW of group captive capacity in FY27, ~800–900 MW of off-grid capacity in FY28, and the balance ~2 GW under CTU connectivity.

* Under the 6.2GW MoU with JSW Steel, ~1 GW is already commissioned, with 1– 1.5 GW expected by FY27 and the balance by 2030.

* The company has already secured 80% of land and 100% of transmission connectivity for projects over the next two years. Additionally, O2 Power has surplus connectivity of ~1.7 GW over and above contracted PPAs, providing future optionality.

* Notably, the company has limited its participation in RE bids over the past few quarters, reflecting disciplined capital allocation amid changing market dynamics.

Most structure advantages across wind and solar (10–15% below industry)

* JSW highlighted meaningful cost advantages across wind, solar, and thermal manufacturing: ? The wind turbine blade manufacturing plant in Gujarat is expected to be commissioned in 1QFY27. Blade imports from China will gradually reduce, with zero imports targeted from FY28 onwards, representing a margin upside.

* Wind turbine prices for the industry are ~INR80m/MW, while JSW expects significantly lower costs, aided by the fixed-price SANY partnership, which insulates the company from currency fluctuations for the next two years.

* Local nacelle manufacturing is under development by SANY, with indigenization efforts ongoing for the past 1–1.5 years.

* Solar plant costs for JSW are ~10% lower than the industry average of INR50m/MW. For already signed PPA-based solar projects, domestic cells are not required, while group captive solar projects use imported modules due to the off-grid status.

Policy momentum and sector demand visibility

* Management cautioned that high-quality wind sites may get exhausted over the next 4–5 years, potentially leading to lower CUFs for new projects, especially in the absence of a clear repowering policy.

* On policy, management expressed confidence that the privatization of DISCOMs will gain momentum once the Draft NEP 2026 is finalized, noting strong government intent. Additionally, any changes to DSM regulations by CERC are not expected to be applied retrospectively.

Valuation and view

* Our valuation of JSW is based on SoTP:

* Thermal is valued at 9x Dec’27E EBITDA, and renewable energy at 12x FY28E EBITDA.

* Hydro is at 2x Dec’27E book value, and green hydrogen equity is at 2x.

* Additionally, the company's stake in JSW Steel is valued at a 25% discount to the current market price, acknowledging the strategic significance of this holding while incorporating a conservative valuation approach.

* By aggregating the values from these different components, the total equity value of JSW was determined, leading to a TP of INR590.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041