Buy Samvardhana Motherson Ltd for the Target Rs.148 by Motilal Oswal Financial Services Ltd

Resilient performance in an adverse macro

Earnings beat led by Modules and Polymers performance

* Samvardhana Motherson’s (SAMIL) 3QFY26 adjusted PAT at INR10.6b was above our estimate of INR10b, up 21% YoY. EBITDA margin was largely stable at 9.7% YoY and ahead of our estimate of 9%. Margin beat was driven by Modules and Polymers business, which saw 200bp margin expansion QoQ to 9.4%, and Integrated Assemblies (+300bp QoQ to 15.2%).

* Given the better-than-expected performance in 3Q despite adverse global macro, we raise our earnings estimates by 6%/1% for FY26/FY27. We expect SAMIL to continue to outperform global automobile sales, fueled by rising premiumization and EV transition, a robust order backlog in autos and nonautos, and successful integration of recent acquisitions. Given the long-term growth opportunities, we reiterate our BUY rating on the stock with a revised TP of INR148, based on 24x Dec’27E EP

Margins remain stable YoY despite adverse macro

* Consolidated revenue grew 13.5% YoY to INR314.1b (in line with our estimate of INR315.3b), aided by organic growth, M&A integration and favorable forex rates.

* EBITDA margin was largely stable YoY but improved 100bp QoQ to 9.7%, above our estimate of 9%.

* Margin beat was driven by Modules and Polymers business, which saw 200bp margin expansion QoQ to 9.4% (well ahead of our estimate of 7.5%) due to benefits of transformative measures. Even Integrated Assembly division saw strong margin improvement to 15.2% (+300bp QoQ), ahead of our estimate of 12%.

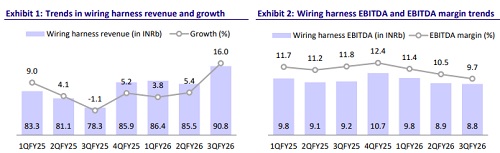

* The two segments that dragged down the overall performance were wiring harness (margin down 210bp YoY to 9.7% and below our est. of 10.3%) and emerging business (margin down 410bp to 9.3% and below our estimate of 10.5%). The wiring harness business was hit by cyclicality in the American CV market and copper price inflation, while the emerging business faced business mix issues.

* Overall, EBITDA grew 13.3% YoY to INR30.4b, ahead of estimate of INR28.2b.

* The company incurred an extraordinary expense of INR465m as provisions for changes in the labor code. Adjusted for this expense, PAT beat our estimates, growing 20.7% YoY to INR10.6b (ahead of estimate of INR10b).

* Net debt has increased to ~INR120b from INR116b QoQ due to increase in short-term debt and RCF rollover. ? Total capex during the quarter stood at INR15.9b, primarily allocated for upcoming Greenfields and maintenance.

Key highlights from the management commentary

* Consumer electronics continued to scale up rapidly (+75% QoQ), with facilities on track to reach annual run-rate of over 16m units by FY26 end. An additional plant is scheduled for 3QFY27, which will double capacity and enhance vertical integration.

* Aerospace business grew 41% YoY in 3Q with continued traction in order book. Additionally, product portfolio was further expanded to supply business jets and rotary wing aircrafts.

* SAMIL currently has 10 greenfield projects at various stages of completion spread across India, Poland, the UAE, and Morocco. Of these, eight are expected to commence production by 2QFY27.

* The acquisition of the Nexans AutoElectric wiring harness business is expected to create a scalable global platform for both PV and CV customers and is expected to close by 1HFY27.

* The earlier announced acquisition of Yutaka Giken is expected to close in the 1HFY27, with the tender offer for shareholding in Yutaka already commenced as of 9th of Feb.

* Effective net debt rose to ~INR120b (vs. INR116b QoQ) due to expanded working capital and sharp forex volatility. Leverage ratio stood at 1.1x (flat QoQ). Management expects the same to reduce further to 0.9x by end of FY26.

* Capex guidance is maintained at INR60b for FY26, with current quarter capex standing at INR15.9b, largely directed toward greenfield expansion and maintenance capex

Valuation and view

Given the better-than-expected performance in 3Q despite adverse global macro, we raise our earnings estimates by 6%/1% for FY26/FY27. Management has alluded to its next five-year revenue growth aspiration, which now stands at a staggering USD108b. We expect SAMIL to continue to outperform global automobile sales, fueled by rising premiumization and EV transition, a robust order backlog in autos and non-autos, and successful integration of recent acquisitions. While the ongoing tariff issue may lead to some near-term slowdown in some of its key geographies, we expect SAMIL to be the least impacted by these tariffs as it has all its facilities close to its customers and can effectively realign supplies as per customer needs. Further, this is likely to lead to industry consolidation, with players like SAMIL likely to emerge as key beneficiaries in the long run. Given the long-term growth opportunities, we reiterate our BUY rating with a revised TP of INR148, based on 24x Dec’27E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412