Buy LG Electronics India Ltd For Target Rs.1,750 By Elara Capital

Harnessing the ‘leadership-growth-return’ flywhee

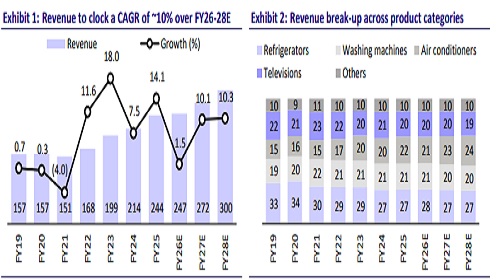

LG Electronics India (LGEIL IN) is the undisputed leader in India’s consumer durable market, with decade-long dominance in the space. We expect LGEIL to see accelerated revenue growth of 14-16% (upside case) led by the LG Essential series in the next five years, similar to the trend seen at Haier and Bluestar (led by capex and re-entry into the economy segment) in FY20-25. Expect earnings to compound at a CAGR of 18% in FY26E-28E, led by rising localization to 63%, bridging product gap via parental support and continued leadership in premium. LGEIL’s INR 50bn capex plan in the next four years should add revenue visibility of INR 200-250bn and open up scope to become an exporter. Initiate with Accumulate and a TP of INR 1,750 on 45x FY28E P/E.

Growth acceleration via LG Essential; strategy similar to competitors: LGEIL is re-entering the economy segment via its LG Essential series in tier II-III markets and in the traditional channel, initially in refrigerators and washing machines, followed by room air conditioners and microwaves. This will enable volume growth, market share gain, and operating leverage. We believe LGEIL would see accelerated revenue growth of 14-16% (upside case) in FY26E30E over a large base from the current growth of 11% if it were to mirror Haier’s blueprint of aggressive pricing, large capex and surging localization, while preserving superior return profile. Similarly, Bluestar in CY21 ventured into the mass premium space, which accelerated its revenue CAGR to 32% – It gained market share by 150bps in FY20-25

Engines of compounding – Localization and bridging product gaps: An earnings CAGR of 18% in FY26E-28E should be underpinned by: 1) rising localization with backward integration into products such as compressors and PCBs, unlike domestic peers (target of 63% from current 54% localization in the next four years), 2) strong parental support for R&D and technology, enabling bridging product gaps between the parent and India operations (data center cooling, medical displays, EV and mobility solutions, wherein the parent has a strong presence) and 3) premium portfolio with leadership in high-value categories. We expect EBITDA margin to rise to 12%+ in FY28E from 11.4% in FY26E versus industry margin at 8%. Doubling exports share to 10-12% in the next five years led by reopening of the US market, catered by the new Sri City facility, is a sunrise area.

Massive capex plan to ensure revenue visibility: LGEIL is incurring a capex of INR 50bn at Sri City, Tamil Nadu in the next four years (3.7x the cumulative capex incurred in FY22-25) to expand capacity in RACs, washing machines, refrigerators and compressors. This may translate into revenue of INR 200-250bn (asset turnover at 4-4.5x) once fully ramped up.

Initiate with Accumulate and a TP of INR 1,750, based on 45x FY28E P/E (at 12.5% premium to the average durables industry P/E of 40x), led by leadership, highest margin versus peers and strong return ratios of 32-35%. We expect an earnings CAGR of 18% with an average ROE and ROCE of 32% and 33% respectively in FY26E-28E. Key risks to our call are slowdown in demand in India’s consumer durables industry, intensifying competitive landscape, inability to pass on price rise and contingent liability related to royalty payment to the parent.

Please refer disclaimer at Report

SEBI Registration number is INH000000933