Buy Cyient Ltd for Target Rs.1,250 by Choice Institutional Equities

Execution Intact; Recovery Dependent on Conversions

We believe Cyient’s Q4FY26 performance reflects stable execution amid nearterm demand volatility, with revenue impacted by timing-led delays while margins remained resilient. Improving order intake, pricing discipline and continued traction in AI-led engineering and semiconductor scale-up support better mediumterm visibility, despite macro headwinds persisting into Q1FY27. DLM’s strong order book & semiconductor investments further strengthen the growth narrative. We retain a constructive medium-term view, factoring in gradual recovery in growth and margin expansion towards 15% EBITM target. We maintain our target multiple at 15x for DET business and based on FY28 EPS, derive a TP of INR 1,250 using a SOTP valuation (Table below), with further re-rating contingent on execution-led growth recovery & semiconductor scaling-up. Additionally, the buyback at INR 1,125/share (~20% premium to CMP), with promoters abstaining, is EPS-accretive and strengthens the shareholder return profile, supporting sentiment; however, we have not factored this into our estimates at this stage, given limited clarity on the acceptance ratio.

Revenue & PAT Miss Estimate; EBITM In Line

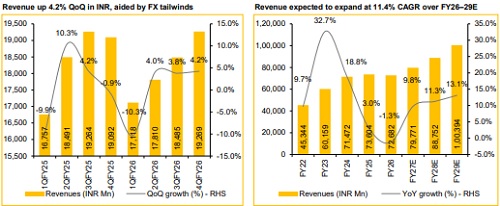

* Revenue for Q4FY26 came in at INR 14.9 Bn, up 0.8% QoQ and 7.4% YoY (vs CIE est. at INR 15.2 Bn)

* EBIT for Q4FY26 came in at INR 1.8 Bn, up 0.4% QoQ and 5.2% YoY (vs CIE est. at INR 1.8 Bn). EBIT margin was flat QoQ while down 26 bps YoY to 12.4% (vs CIE est. at 12.4%)

*- PAT for Q4FY26 came in at INR 1.3 Bn, down 7.8% QoQ and 8.8% YoY (vs CIE est. at INR 1.5 Bn) due to normalisation of other income following elevated FX and restatement gains in prior periods

Program Delays Weigh on Revenue; Mobility Offsets Weakness: DET revenue for Q4FY26 stood at USD 163.5 Mn, declining 2.4% QoQ CC (–1.5% YoY CC), impacted by budget deferrals and delayed ramp-ups across key clients, alongside project pushouts in West Asia within the Energy vertical. Performance was mixed across verticals, with Transportation & Mobility remaining resilient (+4.5% QoQ) led by Aerospace, while Network & Infrastructure declined 3.6% QoQ amid delays & a shift towards AI-led spends; Strategic Units fell 12.4% QoQ on client portfolio reset actions. H2FY26 order intake strengthened with large deal wins & pricing support, improving medium-term visibility. We expect near-term growth to remain soft, with recovery skewed towards H2FY27 driven by improving deal conversion.

Semiconductor Traction Improves; DLM Order Book Supports Outlook: Cyient Semiconductor delivered USD 7.2 Mn revenue in Q4 (+5% QoQ), marking the fourth consecutive quarter of growth, while margin remained negative (EBIT loss of USD 2.8 Mn) amid continued investments in IP, product and talent. The business is scaling up its fabless, IP-led model, supported by 74% stake in Kinetic Technologies and traction in turnkey ASIC and SCL-led opportunities, with management targeting USD 100 Mn FY27 run-rate. Cyient DLM also enters FY27E with its highest-ever order book (book-to-bill ~1.5x), indicating improved visibility

Operational Levers Support Margin; 15% EBITM Guidance Intact: Cyient DET delivered resilient Q4FY26 EBITM of 12.4%, while Consol. margin moderated to 9.5% due to continued investments in Semiconductor business (Q4 EBIT loss: USD 2.8 Mn). Management reiterated its 15% EBITM target by Q4FY27E, supported by pricing gains, AI-led productivity and structural cost optimisation, with forex tailwinds aiding offset of wage inflation. We view margin trajectory to remain intact despite near-term investment drag and macro volatility.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

600-400.jpg)