Buy KPIT Ltd For Target Rs. 970 by Motilal Oswal Financial Services Ltd

Near-term snags; medium-term thesis intact

Product and solution pivot now central to the KPIT story

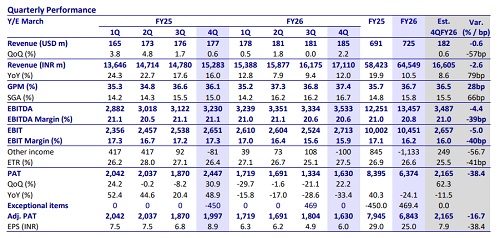

* KPIT Technologies (KPIT) reported revenue of USD185m in 4QFY26, up 1.8% QoQ in CC terms vs. our estimate of 1% growth. Growth was led by the commercial vehicles segment, up 11.6% QoQ, while the passenger car segment declined 0.2% QoQ. EBIT margin was 15.9% (up 25bp QoQ), largely in line with our estimate of 16%. Adj. PAT was down 9.6% QoQ/18.4% YoY to INR1,630m (below our est. of INR2,165m).

* For FY26, revenue/EBIT grew 10.5%/4.58% and adj. PAT declined 13.9% YoY in INR terms. We expect revenue/EBIT/adj. PAT to grow 10.9%/2%/24.3% YoY in 1QFY27. RoE came in at 19.7% in FY26 (vs. 33.1%/31.3%/26.1% in FY25/FY24/FY23). We believe KPIT remains one of the better-positioned ER&D plays within automotive software and continues to be our preferred pick in the space. We reiterate our BUY rating with a revised TP of INR970, based on 25x FY28E EPS.

Our view: KPIT’s chip-to-cloud stack strengthens long-term relevance

* Shift to products and solutions pivotal; near-term growth remains uneven: KPIT’s key strategic shift remains its transition from a services-led model to a products and solutions-led business. Solutions and products now contribute ~15% of revenue (~USD110m), and as seen in Exhibit 2, management targets this mix to scale meaningfully to ~60% over the next three years (with the services mix declining from ~85% to ~40% over the same period), while products and solutions are expected to grow ~30%+ going forward.

* However, the transition is creating near-term disruption in some legacy middleware and traditional services work. In addition, two large SDV programs are ending in 1HFY27, creating a near-term growth headwind, though management indicated the impact is being offset gradually through new client ramps and adjacencies. We believe FY27 will remain a transition year, with acceleration likely becoming more visible from 2H as delayed OEM programs move toward launch and solution-led revenues scale. We estimate FY27 revenue growth at ~4.8% YoY CC.

* KPIT’s software stack and integration capability remain a key differentiator: We believe KPIT’s positioning is materially stronger than most ER&D peers due to its end-to-end automotive software capability across the full chip-tocloud stack. Unlike peers that operate in narrower engineering areas, KPIT covers the entire automotive software V-model from architecture and middleware to feature development, integration, validation, cloud, and aftersales.

* Management highlighted that integration remains the key bottleneck in SDV development, with modern vehicles carrying ~100–120 computers and ~300+ software features that must work seamlessly across different hardware environments. We believe these capabilities differentiate KPIT from traditional engineering vendors and improve its strategic positioning within OEM programs.

* Off-highway, India and China provide medium-term diversification levers: Passenger car demand remains soft globally, particularly among legacy Western OEMs, with delays and cancellations in new platform programs. However, KPIT continues to gain wallet share across most large clients, suggesting the issue is more industry-related than company-specific. In contrast, trucks and off-highway delivered ~18% YoY growth in FY26 and continue to see healthy traction, supported by the >USD50m SDM deal win. We believe adjacencies such as off-highway, connected services, aftersales, and micro-mobility can gradually diversify the revenue base over the medium term.

* At the same time, India and China are becoming strategically important, with both contributing ~4% of revenues each. We believe geographic diversification should improve gradually over FY27–28.

* Margins likely to remain resilient despite elevated investments: KPIT maintained EBITDA margins near ~21% despite continued investments in AI, products, leadership hiring, and acquisitions. FY27 EBITDA margin guidance stands at 20.5–21.2%, reflecting ongoing investments in solutions capabilities and new markets. Management continues to invest >5% of revenue into R&D, materially higher than peers. Over the medium term, the company targets 22–24% EBITDA margins, driven by higher-margin products, AI-infused delivery, reusable solution assets, and increasing fixedprice work. We estimate FY27 EBITDA margins at ~20.8%.

Valuations and changes to our estimates

* We believe KPIT remains well-positioned to benefit from the long-term shift toward SDVs, supported by its capabilities, end-to-end automotive software stack, and increasing focus on products and solutions. While nearterm demand remains uneven due to delays in OEM platform programs and the ramp-down of two large SDV engagements in 1HFY27, we believe that automotive ER&D spending is nearing a bottom, with medium-term software demand remaining structurally intact.

* Factoring in the near-term impact of program ramp-downs and softer growth visibility in 1HFY27, we cut our estimates by 2-5%. However, we continue to expect gradual improvement in growth and margins from FY28 onward, supported by mix improvement, AI-led efficiencies, and increasing fixed-price engagements. We believe KPIT remains one of the better-positioned ER&D plays within automotive software and continues to be our preferred pick in the space. We reiterate our BUY rating with a revised TP of INR970, based on 25x FY28E EPS.

Beat on revenue and margins in line with our estimates; two major SDV programs to end in 1HFY27

* USD revenue came in at USD185m; up 1.8% QoQ in CC terms vs. our estimate of 1% growth. For FY26, revenue stood at USD725m, up 1.3% YoY CC.

* Growth was led by the commercial vehicles segment, up 11.6% QoQ, while the passenger car segment declined 0.2% QoQ.

* In terms of geographies, the US & Asia rose 0.6%/25.1% QoQ in USD terms, while Europe declined 7.1%. ]

* EBIT margin was 15.9% (up 25bp QoQ), largely in line with our estimate of 16%. For FY26, adj. EBIT margin stood at 16.2% vs. 17.1% in FY25.

* Two of the largest SDV programs are coming to an end in 1H, but revenue will be largely compensated by growth in newly acquired accounts. Continuation of these programs would have resulted in 4%-5% sequential growth.

* The company indicated FY27 EBITDA guidance of 20.5%-21.2%.

* Deal TCV stood at USD349m, up 25% YoY.

* Adj. PAT was down 9.6% QoQ/18.4% YoY to INR1,630m (below our est. of INR2,165m). For the full year, adj. PAT stood at INR6.3b, up 83% YoY.

* DSO at the end of 4QFY26 stood at 47 days. The net headcount was down 1.6% QoQ to 12,520 in 4QFY26.

* The company declared a final dividend of INR5.25/share for FY26.

Key highlights from the management commentary

* Demand environment remained uneven - passenger car programs continued to face delays and cancellations (notably Honda's new platform programmes), while commercial vehicles and off-highway witnessed stronger traction. ? ADAS is the fastest-growing spend pocket, expected to reach 3x current levels by 2030; infotainment/digital services and E-architecture are also seeing a material uptick.

* Management views near-term moderation as transitional; medium-term outlook remains robust, driven by an integration demand surge once delayed programs move to the launch phase.

* 4QFY26 is guided to be the highest-growth quarter of FY26 with positive organic growth; profitability is expected to improve sequentially despite continued investments.

* FY27 revenue growth is guided to be higher than FY26; the exact quantum is deferred to April-end commentary. Management expressed reasonable confidence in acceleration.

* Growth in FY26 was led by trucks and off-highway (+18% YoY) and cloudbased connected services; OEM revenues grew ~9% YoY, partially offset by a decline in Tier-1 revenues.

Valuation and view

* We believe KPIT remains well-positioned to benefit from the long-term shift toward SDVs, supported by its capabilities, end-to-end automotive software stack, and increasing focus on products and solutions. Factoring in the near-term impact of program ramp-downs and softer growth visibility in 1HFY27, we cut our estimates by 2-5%.

* However, we continue to expect gradual improvement in growth and margins from FY28 onward, supported by mix improvement, AI-led efficiencies, and increasing fixed-price engagements. We believe KPIT remains one of the better-positioned ER&D plays within automotive software and continues to be our preferred pick in the space. We reiterate our BUY rating with a revised TP of INR970, based on 25x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412