Buy Bajaj Consumer Care Ltd For Target Rs.530 By Elara Capital

Strong Execution; Upside Moderates

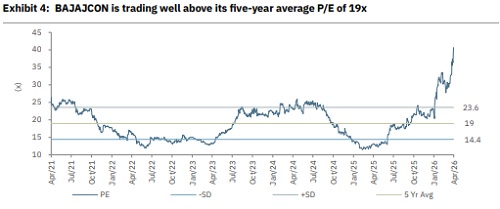

Bajaj Consumer Care (BAJAJCON IN) delivered a 30.4% YoY consolidated revenue growth (in-line with our estimate) in Q4FY26, largely led by c.5% volume growth in Almond Drop Hair Oil (ADHO) and the balance through strategic pricing and improved mix. Next growth lever would be continued distribution growth through Arohan and building the non-ADHO portfolio that stood at INR2.25bn in FY26. Management has guided INR 5bn revenue in the next three years for the non-ADHO portfolio. It has indicated EBITDA margin in low to mid-twenties in the medium term. Given the recent run-up in stock price, we downgrade BAJAJCON to Accumulate from Buy. We raise TP to INR 530 on 25x (unchanged) March 2028E P/E, to factor in overall improvement in revenue and margin.

ADHO volume in mid-single digit; price hikes aided revenue growth: BAJAJCON delivered a volume growth of 5% (adjusted for ml-age reduction – double-digit) in ADHO. Growth was driven by a combination of expansion in distribution, price increase and improved mix. Within the growth portfolio, Banjara saw teens growth along with single digit margin in FY26. The management will focus on Banjara and Coconut hair oil portfolio with new product launches in FY27. The international business (IB) remained a soft spot — marginal YoY drop in Q4 though sequential improvement was visible. Nepal and Bangladesh, the two focus markets, continued to grow. With new leadership in place, management expects sequential improvement in IB in the next two quarters.

Project Arohan scaling up well: Distribution transformation program, Aarohan has now been extended to Phase 3, covering Bihar, Gujarat, Jharkhand, Odisha, and Punjab in Q4FY26. Management indicated that Aarohan states are growing faster by 4% versus non-Aarohan states. With approximately one-third of the business yet to go through the program, it would remain the key growth lever in the next 2-3 years. Driven by the success of Project Aarohan, the general trade (GT) channel saw high-teens growth in FY26, outperforming organized trade (OT). GT channel mix is currently at 70% – While this is split evenly between urban and rural, the urban sector delivered the stronger performance in the past 12 months.

RM cost turns inflationary: Per management, the entire raw material chain has been hit by price hike in the range of 20-40%. BAJAJCON will likely hike price in Q1FY27, but if inflation persists, it may have to take further price hikes to protect margins. In Q4FY26, EBITDA grew by 139.6% and EBITDA margin came in at 23.4% (395bps/567bps ahead of Elara/Bloomberg estimates) owing to higher-than-expected gross margin. Management expects to maintain low to mid-twenties margin in the medium term.

Downgrade to Accumulate, with a higher TP of INR 530: We raise our EPS estimates by 9.6%/16.5% for FY27E/28E, to factor in overall improvement in revenue and margin. We thus raise our TP to INR 530 on 25x (unchanged) from INR 400 as we roll forward to March 2028E P/E. We downgrade BAJAJCON to Accumulate from Buy due to the recent rise in stock price.

Please refer disclaimer at Report

SEBI Registration number is INH000000933