Neutral Can Fin Homes Ltd for the Target Rs. 1,000 by Motilal Oswal Financial Services Ltd

Stable performance supported by steady margins and asset quality

Execution of 15% loan growth and NIM trajectory remain the key monitorables

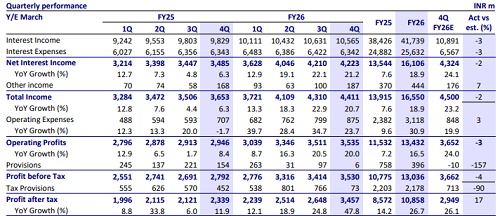

* Can Fin Homes (CANF)’s 4Q PAT grew ~48% YoY to ~INR3.5b (~17% beat). PAT for FY26 grew ~27% to ~INR10.9b. NII in 4QFY26 grew 21% YoY to ~INR4.2b (in line). Fee and other income stood at ~INR187m (PY: INR168m).

* Opex rose ~24% YoY to INR875m (inline). The cost-to-income ratio stood at ~19.8%. (PQ: ~18.5%, PY: ~19.4%). PPoP grew ~20% YoY to INR3.5b (inline). PPoP for FY26 grew ~17% YoY to INR13.4b.

* Provisions stood at INR6m (vs. MOFSLe of INR10m write-back), resulting in annualized credit costs of ~1bp [PQ: ~10bp and PY: ~16bp]. CANF posted an income-tax refund of INR135m in 4QFY26 and a one-time INR460m impact of DTA. This led to a lower effective tax rate of ~2% (PQ: 22.4% and PY: 16.2%).

* CANF is positioned for steady performance, with management guiding ~14% AUM growth in FY27. There is a potential for additional upside if prepayments moderate further. Disbursement momentum remains healthy across key markets, with Karnataka improving to ~INR2.75-2.9b monthly run rate, Tamil Nadu sustaining ~INR1.8-2.0b per month, and Telangana recovering to ~INR1.1–1.2b per month.

* Broadening this trend, growth is also supported by stable contributions from the North and East, reflecting healthy regional diversification and resilient demand conditions, as indicated by strong inquiry pipelines and the absence of any visible slowdown.

* CANF is also focusing on distribution expansion through ~28 new branches planned in 1HFY27, along with the ramp-up of ~54 recently opened branches that are still maturing. Additionally, a meaningful scale-up in the sales force from ~80-90 members to ~150 is expected to enhance sourcing capabilities, while the gradual shift towards higher in-house sourcing is improving overall productivity.

* Asset quality remains strong, with no discernible impact from geopolitical developments on delinquencies or bounce rates, indicating stable repayment behavior at the portfolio level. Karnataka continues to be the best-performing region, with the lowest delinquency levels and a YoY decline in absolute NPAs.

* CANF remains a resilient franchise, supported by strong margin performance even in a declining interest rate environment and consistently superior asset quality. However, we await clearer evidence of the execution of its FY27 loan growth guidance of 15%. We estimate an advances/PAT CAGR of ~14%/7% for CANF over FY26-28, with RoA/RoE of ~2.3%/~17% in FY28. We reiterate our Neutral rating with a TP of INR1,000 (premised on 1.7x FY28E P/BV).

Pricing discipline and the benefit of CoB drive NIM improvement

* NIM (reported) for 4QFY26 rose ~4bp QoQ to ~3.9%. NIM (calc.) declined ~10bp QoQ. Reported yields for 4QFY26 fell ~2bp QoQ to 10.06% while CoB dipped ~6bp QoQ to 7.2%, leading to reported spreads expanding ~4bp QoQ at 2.86%. Bank borrowings for the quarter rose to 63% of the total borrowings (PQ: 62%).

* CANF guided for spreads of ~2.75-2.8%+ and NIM of ~3.75% in FY27. We expect CANF to deliver an NIM (calc.) of ~3.9% for FY27/FY28E.

Strong disbursement momentum drives growth visibility ahead

* CANF’s 4QFY26 disbursements grew ~32% YoY and 19% QoQ to INR32.5b. Advances grew ~10% YoY and ~3.7% QoQ to ~INR422b. Annualized run-off in advances stood at ~17% (PQ: 17.1% and PY: ~15%).

* CANF guided for loan growth of ~14% in FY27 on the back of disbursements of ~INR130b.

* Average ticket size (ATS) of incremental housing loans stood at INR2.7m (PQ: INR2.6m). The DSA channel in the sourcing mix was stable at ~80%.

GS3 and NS3 decline while credit costs remain contained

* Asset quality improved, with GS3 declining ~7bp to 0.85% and NS3 declining ~12bp to ~0.37%.

* Within Karnataka, exposure to IT-linked salaried borrowers (~6%) has not resulted in any negative impact on overall asset quality trends. The company expects asset quality to remain strong, and we model credit costs of 18bp/16bp for FY27/FY28.

Highlights from the management commentary

* CANF has undertaken a major IT transformation with an outlay of ~INR3b, of which INR1b was capex, and ~INR2b was opex spread over five years, aimed at improving scalability and operational efficiency.

* The Karnataka e-Khata issue is gradually being resolved, leading to improved business momentum in the state. Both Karnataka and Telangana are witnessing improving business sentiment, which is expected to support growth acceleration going forward.

Valuation and view

* CANF’s advances grew moderately, while elevated repayments weighed on AUM growth. Margins expanded ~4bp QoQ, supported by a favorable liability mix, and asset quality remained resilient with low GS3 levels. Importantly, disbursement growth was healthy in this quarter, indicating improving underlying momentum. The company guided ~14% loan growth in FY27, with NIM at ~3.75% and credit costs expected to remain benign. Going forward, execution on the loan growth target and the planned technology transformation will be the key monitorables.

* The stock trades at 1.8x FY27E P/B. We model an advances/PAT CAGR of ~14%/7% over FY26-28E, with an RoA/RoE of ~2.3%/~17% in FY28E. We reiterate our Neutral rating with a TP of INR1,000 (based on 1.7x FY28E P/BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412