Buy Supreme Industries Ltd for the Target Rs. 4,320 by Motilal Oswal Financial Services Ltd

Margins expanded due to inventory gains and operating leverage

Strong operating performance, though below our estimates

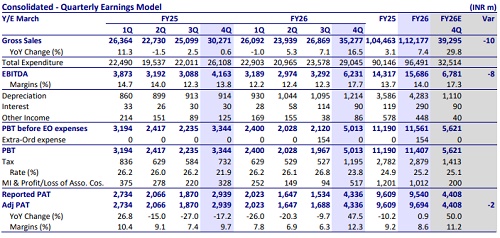

* Despite a lower-than-expected performance, Supreme Industries (SI) reported strong quarterly results, with an EBITDA growth of ~50% in 4QFY26 (vs. a dip in 9MFY26). The improvement was mainly driven by a 34% rise in EBIT/kg to INR22 (due to inventory gains of ~INR0.7-0.8b and operating leverage). Plastic pipe volume rose ~18% YoY. Management guided piping volume growth at ~15-17% for FY27.

* Following a spike in PVC prices in Mar’26 due to the West Asia crisis, management believes the current PVC prices of ~INR81/kg (down ~30% MoM in Apr) will be sustained in FY27, upon which we expect margins to stabilize around ~14% in FY27 (similar to the FY26 levels).

* Factoring in the current volatile geopolitical scenario and management guidance, we cut our FY27 earnings estimates by 6% while broadly retaining our FY28E earnings. We reiterate our BUY rating, valuing the stock at 37x FY28E EPS to arrive at our TP of INR4,320.

Healthy volume growth despite raw material price volatility

* SI’s consolidated revenue grew 17% YoY to INR35.3b (est. INR39.3b), led by growth in volume (up 16% YoY) to 232.9k MT, while realization was flat YoY (INR152/kg).

* EBITDA rose 50% YoY to INR6.2b (est. INR6.8b), with an EBITDA margin expanded by 390bp to 17.7% (est. 17.3%). EBITDA/kg for the quarter was INR26.9/kg (+29% YoY).

* SI’s Adj. PAT grew 48% YoY to INR4.3b (est. INR4.4b). ? Plastic piping products reported a volume of ~192k MT (+18% YoY). Revenue stood at INR25.6b (+23% YoY), and EBIT was INR3.8b (+77% YoY), resulting in an EBIT margin of 14.9% (+450bp YoY). Realization came in at INR133/kg (+4% YoY), while EBIT per kg stood at INR19.9/kg (+50% YoY).

* For industrial products, revenue was INR3.6b (+4% YoY), EBIT was INR416m (+18% YoY), and EBIT margin stood at 11.6% (+150bp YoY). For packaging products, revenue was INR4.6b (+7% YoY), EBIT was INR586m (+3% YoY), and EBIT margin stood at 12.8% (-60bp YoY). For consumer products, revenue came in at INR1.2b (-9% YoY), EBIT was INR315m (+39% YoY), and EBIT margin stood at 25.5% (+890bp YoY).

* For FY26, SI’s volume/revenue/EBITDA/adj. PAT grew 12%/7%/10%/1% YoY to 753.9k MT/INR128b/INR15.7b/INR9.7b, while CFO rose 22% YoY to INR12.2b. Its cash surplus for the year was INR6.6b vs. INR9.5b in FY25.

Key highlights from the management commentary

* Outlook: SI expects 12-13% overall volume growth in FY27, led by 15–17% volume growth in piping, with EBITDA margins of 14-14.5% and ROCE above 25%. Industry demand is projected to recover (~8% growth YoY) after a weak FY26. PVC prices have corrected and are likely to remain range-bound. The company targets USD50m from exports in the medium term, as against the current export level of USD5m.

* Plastic pipes: SI held ~12-13% market share in the piping system, supported by pan-India capacities, SKU expansion, and strong distribution. Further, expansion into electrofusion and olefin fittings is opening up the industrial and gas pipeline segment, which has healthy growth prospects, as there is limited competition. The company’s CPVC business grew ~38% YoY.

* Capex and expansion plans: The company has planned INR10b+ capex for FY27, fully funded through internal accruals, with a balanced focus on greenfield (Patna, Jammu, Gadegaon, and Malanpur) and brownfield expansions. Capacity is set to increase by ~110k MT to ~1.35m MT, including ~100k MT in piping and ~10k MT in material handling.

Valuation and view

* Macro headwinds affecting the PVC industry are largely behind, evidenced by the retracement of PVC prices to sustainable levels and demand recovery resulting in double-digit volume growth for SI over the last three quarters and healthy FY27 guidance. Margins are expected to stabilize, fueled by stable PVC price expectations, an improving mix of VAP, and higher growth in the highmargin CPVC segment. * We expect SI to clock a 16%/20%/23% CAGR in revenue/EBITDA/PAT over FY26- 28. We value the stock at 37x FY28 EPS to arrive at our TP of INR4,320; we reiterate our BUY rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412