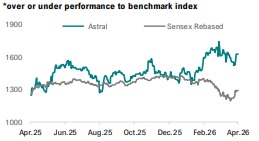

Buy Astral Ltd for the Target Rs.1,912 by Geojit Investments Ltd

High-Quality Franchise Poised for Earnings Recovery

Astral Ltd., founded in 1996 and headquartered in Ahmedabad, is India’s leading CPVC pipe manufacturer. The company pioneered CPVC pipes in India in 1999 and has since diversified into adhesives, paints, and bathware, with 19 manufacturing facilities across India, the UK, and the USA.

* The Indian plastic pipes market is estimated at USD ~7.4 bn and is projected to grow at a 14% CAGR over FY25–FY31, driven by GoI initiatives such as Jal Jeevan Mission, rising urbanisation, and a structural shift toward organised players.

* Astral is India's pioneer and market leader in CPVC pipes, commanding ~25% share in the organised CPVC segment with consistently superior EBITDA margins of 16– 17% across market cycles.

* We expect Astral's revenue to grow at a 16.5% CAGR over FY26–28E, with an earnings CAGR of ~28.1% as capex normalises and new plants ramp utilisation.

* EBITDA margins are projected to expand from 16.2% in FY25 to ~17.7% by FY28E, driven by operating leverage from improved utilisation and benefits from backward integration through Nexelon, expected to commence from Q4FY27.

* ROE is expected to recover from ~15.1% in FY25 toward ~17.5% by FY28E, as asset turns improve with utilisation recovery and margin expansion from backward integration.

Investment Rationale

* Astral’s pipes and fittings segment, which contributes ~70% of revenue, remains the key growth driver, with pipe systems capacity standing at ~410,000 MTPA; overall manufacturing capacity, including adhesives, paints and bathware, is at 549,126 MTPA.

* Firming resin prices have triggered a revival in channel restocking, driving robust plumbing volume growth of 16.8% YoY in Q3FY26, after a sharp 20.6% YoY increase in Q2FY26.

* Capex peaked in FY25 and is expected to moderate going forward, with earnings projected to grow at a CAGR of ~28.1% over FY26–FY28E, supported by rising utilisation and normalising amortisation.

* Astral is backward integrating further with an 80% stake in Nexelon Chem to manufacture CPVC resin (40,000 MTPA by Q4FY27), eliminating import dependence and supporting margin expansion from FY28.

* Astral's CPVC leadership and diversified portfolio across adhesives, paints, and bathware provide structural resilience, with non-pipes segments expected to register ~15.4% CAGR over FY26–28E.

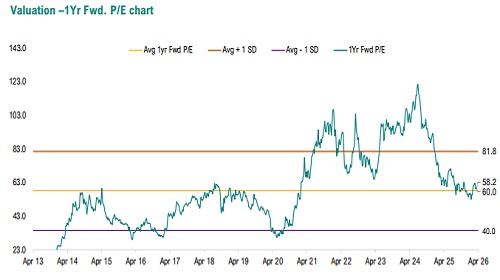

Valuations

We initiate coverage with a BUY rating and a target price of Rs. 1,912, based on 58x FY28E EPS. The valuation reflects Astral’s premium CPVC positioning, visible post-capex earnings inflection, and structurally lower earnings volatility relative to peers.

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034