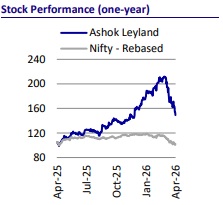

Buy Ashok Leyland Ltd for the Target Rs.185 by Motilal Oswal Financial Services Ltd

CV outlook at risk if global headwinds persist longer

We recently interacted with the management of Ashok Leyland (AL). The key takeaways are as follows: Domestic CV demand, which had revived post-GST rate cut, has sustained even in Mar’26. Demand revival has been positive across all CV segments. Further, to gain share, AL plans a major expansion in Western India with 30 new touchpoints to be added to its current strength of 150 in the region. However, the ongoing geopolitical headwinds pose risks to our estimates given: 1) a sustained rise in crude could derail economic growth and is likely to be detrimental for CV demand, 2) exports, which are likely to see near-term headwinds as the Middle East market contributes 35 - 40% of the exports, and 3) uncertainty over sustained gas availability as well as a rise in input costs. To factor in the risks due to the ongoing WestAsia conflict, we have now lowered our estimates by 13% each for FY27E/FY28E. Assuming this conflict does not continue beyond Q1FY27, we reiterate our BUY rating on the stock with a TP of INR185 (based on 13x Dec’27E EV/EBITDA + ~INR10/sh for the NBFC).

CV demand momentum continues

GST rate cuts have helped revive CV demand since Sep’25, and the momentum has sustained even in March. Even small fleet operators, whose contribution to freight movement had significantly declined post-pandemic, are now buying new fleets, given the pickup in freight demand. Further, the good part of this demand revival is that the momentum is strong across all segments, whether it is light commercial vehicles (LCVs), intermediate, or heavy - duty CVs. Further, in order to gain share, AL is planning a major expansion in Western India with 30 new touch points to be added to its current 150 touch points in the region.

Global conflict may derail current sentiments

The key cause of concern from the ongoing geopolitical macro is the mounting crude prices, which, if sustained for longer, will likely limit the country’s economic growth. This, along with rising inflation, is likely to be detrimental for CV growth in the future. Even AL’s exports will face near - term headwinds as the Middle East market contributes almost 35 - 40% of the exports. On the availability of gas, while there are no immediate hiccups, there is also no clarity as yet on how long uninterrupted production will continue. Further, input costs are also mounting, the impact of which is likely to be visible in the financials from 1QFY27. To offset this impact, AL announced a price hike of up to 2% in CVs w.e.f. 1 st Apr’26.

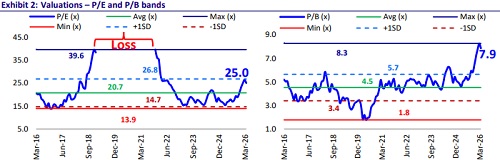

Valuation and view

To factor in the risks due to the ongoing WestAsia conflict, we have now lowered our estimates by 13% each for FY27E/FY28E. After the recent correction, the stock is now attractively valued at 21.0x FY27 and at 17.6x FY28E. Assuming this conflict does not continue beyond Q1FY27, we reiterate our BUY rating on the stock with a TP of INR185 (based on 13x Dec’27E EV/EBITDA + ~INR10/sh for the NBFC).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041