Buy Arvind Fashions Ltd for the Target Rs.650 by Motilal Oswal Financial Services Ltd

Fundamentals intact, correction creates opportunity

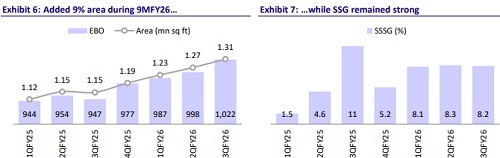

* Arvind Fashions (AFL) is demonstrating a steady operating momentum, with its 9MFY26 performance - highlighted by a robust 8% same-store sales growth (SSSG) - underscoring the strength of its execution across retail, online, and brand portfolios, despite broader demand conditions remaining soft.

* Growth continues to be fueled by direct channels, with retail increasing 14% YoY and online rising 19% YoY, contributing to a more diversified channel mix.

* This, alongside a reduction in discounting and stable inventory turns (~4x), has aided gross margin expansion (up 115bp YoY) and improved cash conversion.

* Core brands remain resilient, while adjacencies - now accounting for over 20% of revenue - are scaling profitably, providing additional growth levers.

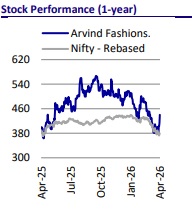

* Despite this, the stock is down ~20% on a 6M basis, with valuations now attractive at 35x FY27E earnings (vs. 37x for ABLBL). We believe this correction presents a compelling entry opportunity into a high - quality franchise featuring a strengthening direct channel, a visible adjacency growth runway, and improving earnings quality.

* We model a revenue/EBITDA CAGR of 12%/19% over FY26 - 28E. We reiterate our BUY rating with an SoTP - based TP of INR650.

USPA inflection: Profit growth becoming visible

* USPA (within Lifestyle) is witnessing a sharp improvement in profitability, with 9MFY26 PAT at ~INR996m (vs. ~INR59m YoY), implying strong earnings growth and meaningful margin expansion.

* Growth is broad-based, driven by better sell-through, ~11% retail LTL, 25% growth across adjacencies (womenswear, kids, innerwear, footwear), and a strong scale-up in online B2C.

* Reported standalone weakness (revenue of +3% YoY; PAT loss at INR474m vs. INR49m profit YoY) is structural, reflecting the transition of Arrow Retail out of Lifestyle and the cessation of intra-group sales..

* These losses are not incremental but represent a reclassification of existing losses, which were earlier absorbed within Lifestyle and are now visible in standalone financials due to the ongoing reorganization of the retail structure.

* On a combined basis (Standalone ex-dividend + Lifestyle), PAT jumped ~5x to INR522m vs. INR108m YoY, while PAT post-minority rose 75% YoY to INR1,054m. This increase clearly indicates that USPA is driving the improvement in the overall earnings trajectory.

Direct channel flywheel delivering results

* AFL’s direct channel pivot is now visible in its execution, with retail sustaining ~8% LTL across 9MFY26 and online B2C delivering 30 - 50% growth, taking the direct mix to ~57% (vs. ~54% YoY), with a clear runway toward ~75%.

* Improved mix has driven a healthy reduction in discounting and ~115bp YoY gross margin expansion, reflecting improved sell - through and tighter control over pricing and inventory.

* EBITDA margin expansion, however, remains measured (~30bp YoY in 9MFY26), as GM gains are being reinvested into higher A&P spending. This indicates a conscious strategy to strengthen brand salience while sustaining growth momentum.

* Inventory discipline remains the core enabler, with freshness at ~85%+, supporting a sharper assortment, reducing end-of-season dependency, and reinforcing a self-sustaining cycle of higher full-price sell-through and structurally better margin quality.

Adjacencies building a structurally accretive second revenue engine

* AFL’s adjacent categories (footwear, innerwear, womenswear, kids) now contribute more than ~20% of revenue and are growing at ~20–25%, materially outpacing core apparel.

* Footwear (~INR3b) has reaccelerated to high-20% growth post-BIS normalization, targeting INR5b in the next few years, while Innerwear is tracking better growth supported by improved availability and a better channel mix.

* Womenswear (~50% YoY on a small base) and kids (25%) categories are scaling well within the USPA ecosystem, with distribution expanding from digital-first to offline, supporting category deepening.

* Adjacencies are rapidly emerging as a secondary revenue driver, scaling within existing EBOs and increasing sales density while retaining healthy profitability. This approach ensures accelerated growth without compromising the margin profile.

Valuation and view

* AFL is delivering steady operating momentum, with performance demonstrating strong execution across retail, online, and brand portfolios despite a subdued demand environment.

* Growth is increasingly fueled by direct channels, improving the mix and aiding margin expansion through better sell-through and tighter inventory control.

* USPA has emerged as the key earnings driver, demonstrating broad-based traction across channels and categories. Meanwhile, the reported standalone weakness is largely structural and does not reflect the underlying performance.

* Adjacent categories continue to scale profitably, adding a second growth engine without diluting margins and enhancing overall earnings quality.

* Despite this, the stock is down ~20% on 6M basis, with valuations now attractive at 35x FY27E earnings (vs. 37x for ABLBL). We believe this correction presents a compelling entry opportunity into a high-quality franchise featuring a strengthening direct channel, a visible adjacency growth runway, and improving earnings quality.

* We model a revenue/EBITDA CAGR of 12%/19% over FY26-28E. We reiterate our BUY rating with an SoTP-based TP of INR650.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041