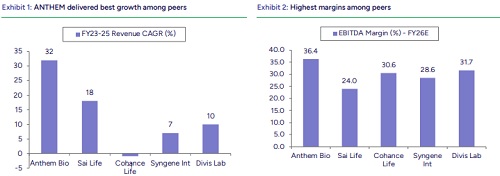

Buy Anthem Biosciences Ltd for the Target Rs. 755 By Prabhudas Lilladher Ltd

Drivers aligned for next leg of growth

Quick Pointers

* Differentiated capabilities across modalities ensures cost efficiency

* Strong portfolio of commercial molecules to drive 23% CAGR in the CDMO over FY26–28E.

* Capacity expansions provides strong growth visibility

We initiate coverage on ANTHEM with ‘BUY’ rating and TP of INR755/share, implying ~16% upside from current levels. Growth visibility remains strong given a deep pipeline spanning discovery to late-stage development, along with a commercial portfolio. Demand for commercialized molecules should remain healthy, supported by the ramp-up of recently launched molecules and potential commercialization of late - stage programs. The specialty ingredients business is expected to benefit from GLP - 1 API ramp-up from H2CY26. With INR10-12bn capex planned, largely through internal accruals, ANTHEM is expanding capacity to support future growth.

We forecast REVENUE/EBITDA/PAT CAGR of ~21%/22%/18% over FY26 - 28E led by 23% growth in CDMO services, ~11% in CRO and ~14% in specialty ingredients. ANTHEM remains one of the fastest growing Indian CRDMOs. At CMP, the stock is trading at ~30x EV/EBIDTA and ~44x P/E on FY28E. We value the company at 50x P/E on FY28E, in line with Divis. Initiate with ‘BUY’.

Comprehensive capabilities across modalities: ANTHEM has developed a broad CRDMO platform with capabilities across small molecules, highly complex modalities, and biologics. Its platform spans 5 key modalities - RNAi, ADCs, peptides, lipids and oligonucleotides - and a high-margin FFS - led CRO model (~90% of projects). These modalities ensure cost-efficiency and wider spectrum of services.

Portfolio with strong commercial exposure: ANTHEM has ~14 commercial molecules. 6 of these commercial molecules generated ~$12bn at innovator level in sales in CY24 and are expected to reach ~$22bn by CY29. In addition, 4 molecules have been commercialized in FY26 with an estimated peak sales potential of $12 - 15bn. On the development side, it has 5 - 6 molecules in Phase 2, while the Phase 3 pipeline remains stable with 6 molecules. With most commercial molecules expected to go off - patent post FY30E, we expect the CDMO segment to grow at 23% CAGR over FY26 - 28E.

Fermentation-based specialty ingredients provide stability: ANTHEM’s specialty ingredients segment focuses on fermentation-based, high - value products such as enzymes, probiotics and peptides, offering better margins and stronger entry barriers than commoditized generic APIs. With growing contribution from GLP - 1 related supplies from FY27E, the segment is expected to deliver ~14% revenue CAGR over FY26–28E vs. 3% CAGR over FY24-26E.

Scaling capacities to capture growth opportunities: ANTHEM operates custom synthesis capacity of 400kL and fermentation capacity of 142kL; these are being expanded to reach 425kL and ~182kL, respectively, by FY26E. Utilization is expected to improve with the recent ramp-up of Unit III (Neoanthem). Further, Unit IV at Harohalli near Bengaluru, a ~INR10bn capex project focused on high - value peptides and APIs, is likely to be commissioned in phases by FY28E/29E, which will meaningfully expand its manufacturing footprint.

Please refer disclaimer at Report

SEBI Registration number is INH000000933