Not Rated Brigade Hotel Ventures Ltd for the Target Rs.NA by PL Capital

Execution of expansion plan to be keenly watched

We met the management of Brigade Hotel Ventures Ltd (BRIGHOTE IN) to derive insights into the company’s expansion plan, which entails doubling of inventory by FY30E. BRIGHOTE IN is the 2nd largest owner & developer of chain affiliated hotels in South India. It has a portfolio of 9 hotels comprising 1,604 keys that are managed by global brands like Marriott International, Accor and IHG. The expansion plan entails addition of 1,700 keys by FY30E at an estimated capex of Rs36bn. The expansion is likely to be funded via internal accruals and debt. Post IPO, the balance sheet has become lean with debt/cash balance of Rs2bn/Rs3bn as of 1HFY26. However, given the plan to add 45/586 keys in FY27E/FY28E, leverage is likely to increase in future. Over FY23-25, BRIGHOTE IN’s revenue/EBITDA has registered a CAGR of 15%/27%. We believe execution of the plan to double the inventory in 5 years, will be keenly watched from here on. The stock trades at 12x/10x based on FY27E/FY28E consensus EBITDA. Not Rated.

Strong parentage: BRIGHOTE IN is a part of the Brigade Group, which has 4 decades of experience in developing large-scale real estate and commercial projects in India. The group has successfully delivered over 200 residential projects across 6 cities and completed 28mn+ sqft of commercial space across 8 cities in India.

Being a part of the Brigade Group not only lends deep understanding of the micro markets but also enables BRIGHOTE IN to locate strategic land parcels and build hotels in a cost-efficient and timely manner. Sharing services like HR, accounting and legal with the group lends operating efficiency gains, while having assets as part of mixed-use projects developed by the parent, helps boost occupancy.

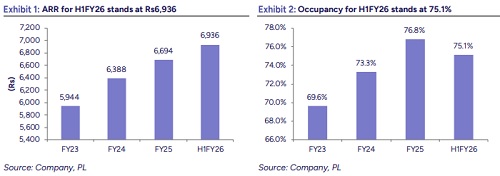

Affiliation with global hospitality brands: BRIGHOTE IN has strategic alliance with globally renowned brands like Marriott International, Accor and IHG. These partnerships provide BRIGHOTE IN access to their distribution network, marketing strategies, operational know-how and loyalty programs, thereby aiding occupancy and ARR

Plan to double portfolio by FY30E: BRIGHOTE IN has a portfolio of 9 hotels and 1,604 keys in Bengaluru, Mysuru, Chennai, Kochi and Ahmedabad (refer Exhibit 4 for geographical mix). The plan is to double the inventory by adding 1,700 keys across 9 hotels by FY30E (refer Exhibit 6 for details on inventory pipeline). Given that upcoming inventory is predominantly in South India where the parent entity has deep understanding about the micro markets, we do not foresee any material execution risk on the horizon.

Capex plan of Rs36bn by FY30E: Planned addition of 1,700 keys will entail a capex of Rs36bn over the next 5 years. BRIGHOTE IN plans to incur a capex of Rs14.9bn over FY26E-27E, followed by an additional capex of Rs21.1bn over FY28E-30E. About 49% of the keys will be in the luxury segment, indicating portfolio premiumization is on the cards.

Leverage likely to rise: BRIGHOTE IN’s debt stood at Rs6.2bn in FY25 (pre-IPO). Following the IPO, the company utilized Rs4.7bn to repay debt. Consequently, as of 1HFY26, BRIGHOTE IN’s debt declined to ~Rs2bn. Nonetheless, given the aggressive expansion plan, leverage levels are expected to rise over the next 3-4 years.

Above views are of the author and not of the website kindly read disclaimer