320-x-100_uti_gold.jpg" alt="Advertisement">

320-x-100_uti_gold.jpg" alt="Advertisement">

Debt Outlook for year 2021 by Pankaj Pathak, Quantum Asset Management Company

Follow us Now on Telegram ! Get daily 10 - 12 important updates on Business, Finance and Investment. Join our Telegram Channel

Below are Views On Debt Outlook for year 2021 by Pankaj Pathak , Fund Manager-Fixed Income, Quantum Asset Management Company

2020 has been an extraordinary year on many accounts. It has been a year of facing, learning and adapting to the unknown. It has changed human and societal behavior in a significant way. The manner in which various markets have responded over the course of the year would have altered investor behavior as well.

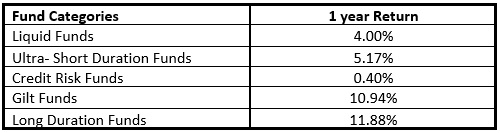

Fixed income investors witnessed another year of mixed performance across various categories. Interest rates on bank deposits and returns on liquid and money market funds continued to go down and now at levels last seen during 2008 financial crisis. Credit risk funds had yet another painful year and in some cases wiped out a significant part of investors savings. Contrary to these, investors in long duration and high credit quality bond funds enjoyed another year of great performance.

The RBI continued it’s easy monetary policy by cutting policy rates and infusing a lot of liquidity into the banking system. The policy repo rate has been reduced by cumulative 115 basis points and the reverse repo rate by 155 basis points in 2020. This was after 135 basis points reduction in the policy rates in the last calendar year. The policy repo rate currently stands at 4.0% and the reverse repo rate at 3.35%

RBI’s action on liquidity was even more aggressive. Liquidity surplus in the Banking system has been kept over Rs. 6 trillion for most of the time this year. This high liquidity surplus has kept the short term money market rates such as 3 months treasury bills or PSU CP/ CDs below the reverse repo rate. Currently the 3 month treasury bills and PSU CPs are quoting below 3.2%.

Going into 2021, the drivers of fixed income performance are likely to change. In the last two years performance of the fixed income asset class was predominantly driven by the RBI’s monetary accommodation. But now with inflation hovering above the policy repo rate, room for further rate cuts may not be available.

We see following themes playing out in the next year

Monetary policy normalization

In 2020 central banks across the globe have gone ‘all in’ to neutralize the economic pain caused by the covid-19 pandemic. Going into 2021 the impact of the crisis is subsiding and the economy is getting back on track. However, the recovery is still at a nascent stage and will require continued policy supports.

The RBI, in its October monetary policy, has committed to maintain an accommodative monetary stance in the current fiscal year and going into the next fiscal year. Given the macro backdrop of fragile growth recovery and sticky inflation trend, the RBI may maintain a status quo on policy rates in the next year. Nevertheless, if growth recovery sustains, its focus could shift towards policy normalization and a gradual withdrawal of excess monetary accommodation.

In the past, liquidity excesses has caused macro instability and resulted in crisis. Uncontrollable inflationary pressures post 2008 global financial crisis and the recent credit crisis in the bond and money markets after the IL&FS collapse all have their roots linked to excess liquidity.

We expect the RBI to begin normalization of monetary policy by the middle of 2021. They will begin by reducing the amount of excess liquidity. This could lead to the policy rate moving from Reverse Repo to the Repo Rate. In such a scenario, overnight and short term interest rates could begin to rise. This is positive for prospective returns from liquid funds.

Fiscal consolidation roadmap

Just like monetary policy, the government also stretched its fiscal position to deal with the crisis. Even before this pandemic, consolidated fiscal deficit of center and state government was at elevated levels. In the crisis it faced a double whammy of lower tax collections and an increased spending on health care and welfare.

In the current fiscal year 2020-21, center’s fiscal deficit could rise to 8% of GDP while states could add about 5% of GDP. India’s public debt could jump to about 90% of GDP this year. This is one of the highest among similar rated emerging economies.

A medium term fiscal plan will be needed to bring down the fiscal deficit and debt levels to more sustainable levels. Government’s roadmap for fiscal consolidation will have bearing on the bond markets. Market will closely watch for cues in the budget for FY 2021-22 which would be presented in February 2021. Anything higher than 6% FD/GDP would require support from RBI, else rates are likely to move higher.

Global Bond Index and Foreign flows

Globally bond yields have come down. In most of the developed economies yields are close to zero or even negative. Compared to this, the yield on Indian bonds looks attractive even after adjusting for potential INR depreciation.

Government is also keen on attracting foreign capital into Indian debt. They have made necessary changes in the rules for foreign investments to get into global bond indices. Foreign investments in India bonds are now below USD 40 bn. The potential limits available for investment is now upwards of USD 200 billion. Given the high global liquidity and low yields in developed economies, India could attract sizeable foreign inflows in the domestic bond markets. If happens this would be a major positive for the bond markets.

Outlook

In 2021 bond yields could reverse their downward trend and grind up towards the year end. Short end rates (up to 3 years maturity) are currently priced aggressively due to excess liquidity thus carry maximum risk of reversal. While the longer segment may continue to get the RBI’s support from OMO purchases and twists. Thus the yield curve will likely flatten in the next year (short term rates move up more than longer ends).

Fixed income investors should acknowledge that the best of the bond market rally is now behind us. Currently bond yields are at multi year lows and scope for capital gains look limited. Going into next year, investors should lower their return expectations from fixed income funds.

Above views are of the author and not of the website kindly read disclaimer