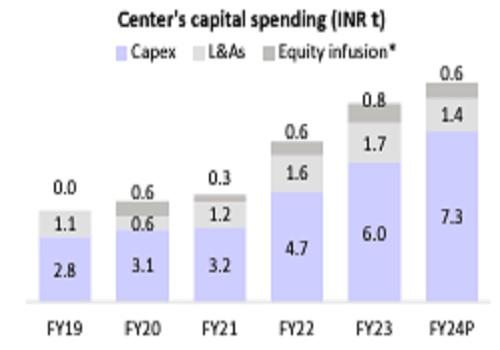

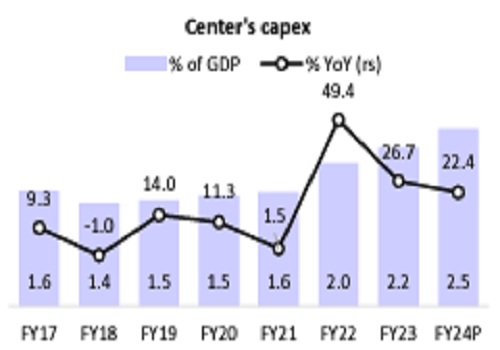

.jpg)

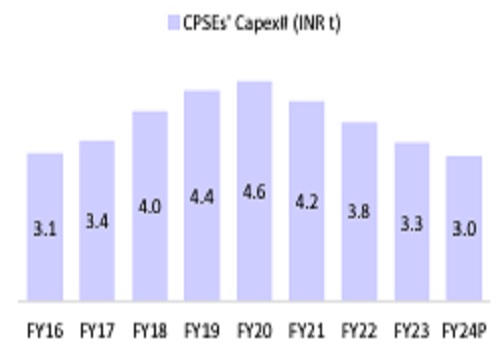

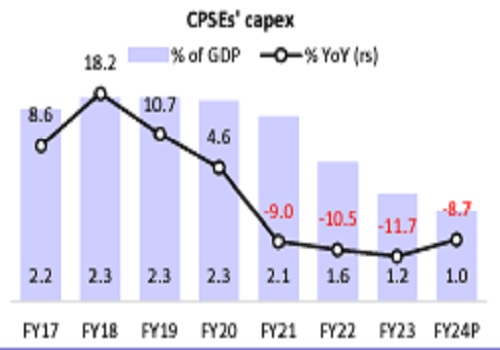

Cement Sector

Demand set to rise, yet pricing remains competitive in 2H Industry volume up 3-...

Read More

Banks Finding It Difficult to Raise Deposits Depositors Shifting to Alternative Investments

Increase in Inflation Was Driven by Food Component Which Remained Stubborn

Flexible Inflation Targeting Framework Has Worked Well

To Reduce Window of Cheque Clearing; to be Cleared Within Few Hourse Of Presentation

Transaction Limit of Tax Payment Through UPI Raised to Rs.5 lk From Rs. 1 lk

Public Repository Of Digital Lending Apps Will Help Identify Unauthorised Lending Apps

Propose is to Introduce Facility of Delegated Payment in UPI

Current Account Deficit Remains Eminently Manageable in Current FY

FDI Flows Picked Up in FY25, Gross FDI Up 20% in April-May

Alternative Investment Avenues Are Becoming More Attractive To Retail Customers

Banks Are Taking Greater Recourse To Short-Term Non-retail Deposits

Food Inflation Contributed to More Than 75% Of Headline Inflation In May & June

Many Central Banks Moving Toward Policy Pivots, Some Have Tightened Rates As Well

Market Participants Must Keep In Mind India's Robust Fundamentals

As Of Aug 7, Indian Rupee Remained Range Bound In FY25

RBI Remains Committed To Ensure Orderly Evolution Of Financial Markets

Term Premium Has Remained Steady In Recent Months

10-year India Bond Yield softened Further In July

BI Will Continue To Be Nimble, Flexible In Liquidity Management

AS Of Aug 7, Indian Rupee Remained Range Bound In FY25

Global Developments Have Implications For Emerging Market Economies

Public At Large Understands Inflation In Terms Of Food Inflation Than Other Components

MPC May Look Through High Food Inflation If It Is Transitory

Yields On Certificates Of Deposits, 3-month Treasury Bills Softened

Term Premium Has Remained Steady In Recent Months

Transmission In Credit Market Remains Ongoing

In Environment Of High Food Inflation, MPC Can't Afford To Look Through It

MPC To Remain Vigilant To Prevent Spillovers Or 2nd-round Effects From Persistent Food Inflation

Cannot And Should Not Become Complacent Because Core Infaltion Has Fallen

MPC May Look Through High Food Inflation If It Is Transitory

Public At Large Understands Inflation In Terms Of Food Inflation Than Other Components

Can't Become Complacent Merely Because Core Inflation Has Fallen

Seeing Considerable Divergence Between And Core Inflation

Real GDP Growth In Q3 FY25 Seen At 7.3%

FY25 Inflation Projection At 4.5%

Q1 FY26 Inflation Seen At 4.4%

Target Is Headline Inflation, Where Food Inflation Has Weightage Of 46%

Food Inflation Pressures Can't Be Ignored

Real GDP Growth For FY25 Projected At 7.2%

Q1 GDP Growth Seen 7.2% Vs 7.2% Earlier

Q1 FY26 Real GDP Growth Seen At 7.2%

SDF Rate Unchanged 6.25%

PMI Services Stood Strong At 60.3 In July And Remained Above 60 In 7 Consecutive Months

Near-Term Outlook Looks Positive For Global Growth

Significant Challenges To Medium-Term Global Growth Outlook

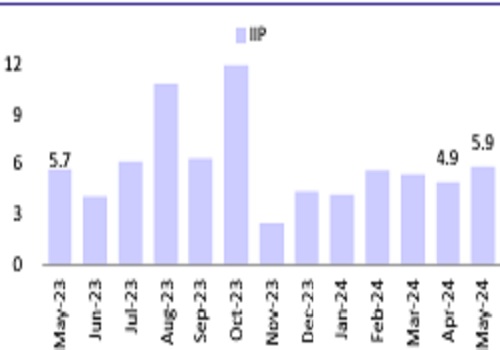

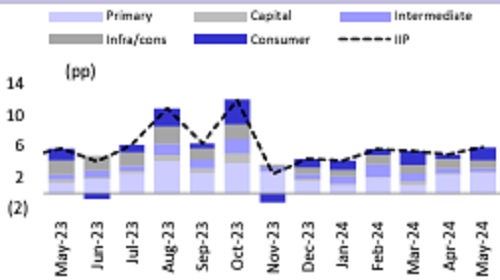

IIP Growth Accelerated In May This Year

PMI For Manufacturing At 58.1 In July Remained Elevated

Servieces Sector Retained Buoyancy

Inflation Is Receding Grudgingly Across Major Economies

Inflation Is Receding Grudgingly Across Major Economies

Start-up/Fintech Budget Quote on Union Budget 2024-25 by Yashoraj Tyagi, CEO, CASHe

Start-up/Fintech Budget Quote on union budget 2024-25 by Mr. V. Raman Kumar, Founder & Chairman, CASHe

Budget Reaction on Startup by Avinash Shekhar, CoFounder & CEO, Pi42

Budget Reaction on Startup by Sachin Agrawal, Co-Founder & CEO at Bizongo

Budget Reaction on Startup by Akshay Mehrotra, Cofounder & CEO, Fibe, India`s leading fintech and consumer lending platform

How Viksit States can help India become world's 3rd largest economy faster

Views on budget Markets - Debt & Equity & Sectors Outlook by Tata Mutual Fund

Budget 2024 sets new precedent for prioritising job creation, skilling: Jayant Chaudhary

Explainer: How full Budget 2024 compares with Interim Budget

Budget increases expenditure for National Health Mission, proposes digital public infra

Quote on Budget by Pankaj Singh, smallcase Manager and Founder & Principal Researcher at Smartwealth.ai

at S K Patodia & Associates.jpg)

Comment on Review of Income Tax Act by Mihir Tanna, Associate Director - Direct Tax at SK Patodia & Associates LLP

Quote on Budget by Suman Bannerjee, CIO, Hedonova

Union Budget 2024 Input on Annual Returns by Siddharth Tandon, Partner, Indirect Tax, BDO India

Union Budget 2024 Input on Taxation Sector by Rony Antony, Partner & Leader, Corporate Tax (South), Tax & Regulatory Services, BDO India

Broadband sector to drive telecom industry growth, create new jobs

Key PLI schemes bring significant boost to local EV manufacturing in India

India's steel production shot up by over 35 million tonnes in last 4 years: Centre

Substantial tax savings expected for majority of taxpayers due to reduction in LTCG rate in real estate: IT department

Vietnam's e-commerce boasts highest annual growth in ASEAN

Start-up/Fintech Budget Quote on Union Budget 2024-25 by Yashoraj Tyagi, CEO, CASHe

Start-up/Fintech Budget Quote on union budget 2024-25 by Mr. V. Raman Kumar, Founder & Chairman, CASHe

Budget Reaction on Startup by Avinash Shekhar, CoFounder & CEO, Pi42

Budget Reaction on Startup by Sachin Agrawal, Co-Founder & CEO at Bizongo

Budget Reaction on Startup by Akshay Mehrotra, Cofounder & CEO, Fibe, India`s leading fintech and consumer lending platform

How Viksit States can help India become world's 3rd largest economy faster

Views on budget Markets - Debt & Equity & Sectors Outlook by Tata Mutual Fund

Budget 2024 sets new precedent for prioritising job creation, skilling: Jayant Chaudhary

Explainer: How full Budget 2024 compares with Interim Budget

Budget increases expenditure for National Health Mission, proposes digital public infra

Quote on Budget by Pankaj Singh, smallcase Manager and Founder & Principal Researcher at Smartwealth.ai

Comment on Review of Income Tax Act by Mihir Tanna, Associate Director - Direct Tax at SK Patodia & Associates LLP

Quote on Budget by Suman Bannerjee, CIO, Hedonova

Union Budget 2024 Input on Annual Returns by Siddharth Tandon, Partner, Indirect Tax, BDO India

Union Budget 2024 Input on Taxation Sector by Rony Antony, Partner & Leader, Corporate Tax (South), Tax & Regulatory Services, BDO India

Broadband sector to drive telecom industry growth, create new jobs

Key PLI schemes bring significant boost to local EV manufacturing in India

India's steel production shot up by over 35 million tonnes in last 4 years: Centre

Substantial tax savings expected for majority of taxpayers due to reduction in LTCG rate in real estate: IT department

Vietnam's e-commerce boasts highest annual growth in ASEAN

| index | price | chg% |

|---|